21 Instrumental Variables Regression

21.1 Introduction

In this chapter, we will discuss instrumental variables (IV) regression. IV regression is a method that provides a way to obtain a consistent estimate of the coefficient of the variable of interest when it is correlated with the error term. In this method, we use instrumental variables or simply instruments for isolating the part of the variable of interest that is correlated with the error term. The method addresses omitted variable bias, simultaneous causality bias, and errors-in-variables bias.

21.2 The IV estimator with a single regressor and a single instrument

We consider the following simple linear regression model: \[ Y_i=\beta_0+\beta_1X_i+u_i. \]

To introduce the IV approach, we first determine when there is endogeneity in the model.

Definition 21.1 (Endogeneity and exogeneity) We call a variable that is correlated with the error term an endogenous variable and a variable that is uncorrelated with the error term an exogenous variable.

Recall that \(\text{Cov}(X_i,u_i)\neq 0\) implies \(\E(u_i|X_i)\neq 0\). Thus, if \(X_i\) is endogenous, then the OLS estimator is biased and inconsistent.

Definition 21.2 (Instrumental variable) We call a variable that is correlated with the endogenous variable but uncorrelated with the error term an instrumental variable or simply an instrument.

Let \(Z_i\) be an instrumental variable for \(X_i\). Then, \(Z\) satisfies the following two conditions:

- Instrument relevance: The instrumental variable is correlated with the endogenous variable, i.e., \(\text{Cov}(Z_i,X_i)\neq 0\).

- Instrument exogeneity: The instrumental variable is uncorrelated with the error term, i.e., \(\text{Cov}(Z_i,u_i)=0\).

Example 21.1 (Philip Wright and Sewall Wright) The IV method was developed by Philip Wright and his son Sewall Wright in the 1920s. The key idea first appeared in an appendix to a book written by Philip Wright in 1928 (Stock and Trebbi (2003)). The author was interested in estimating the elasticities of demand and supply for products such as vegetable oils, butter, and soy oil. Consider the following demand equation for butter: \[ \begin{align} \ln(Q^{demand}_i)=\beta_0+\beta_1P_i+u_i, \end{align} \]

where \(Q^{demand}_i\) is the butter consumption in the \(i\)th period, \(P_i\) is the price of butter, and \(u_i\) includes all other factors that affect butter consumption, such as income and consumer preferences. In this equation, \(\beta_1\) represents the demand elasticity for butter. Philip Wright collected data on annual butter consumption and the average annual butter price in the U.S. over the period 1912–1922. He realized that these data could not be used to estimate the demand elasticity because the price is determined by the intersection of supply and demand.

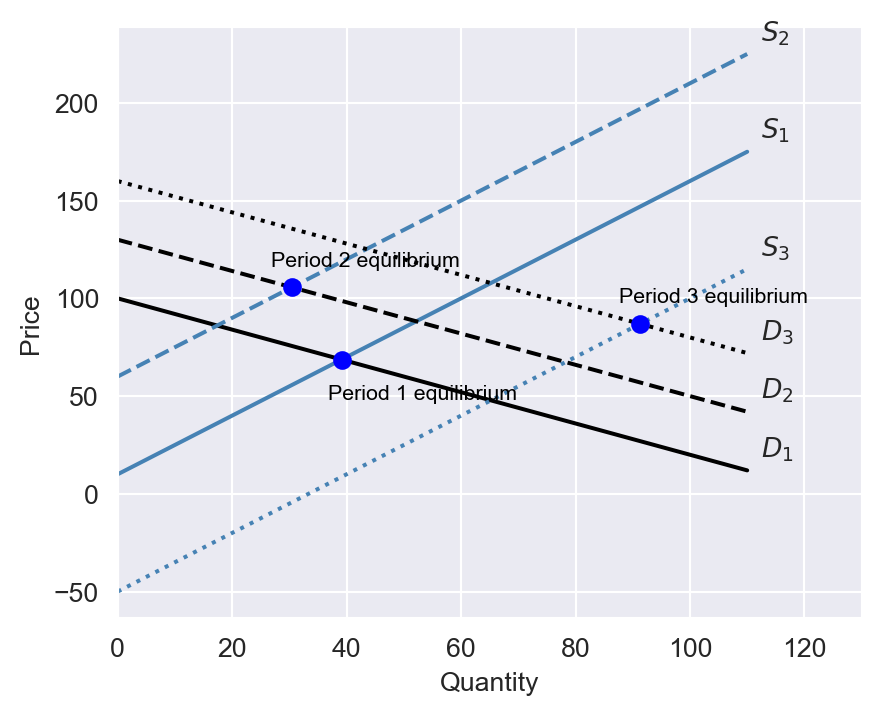

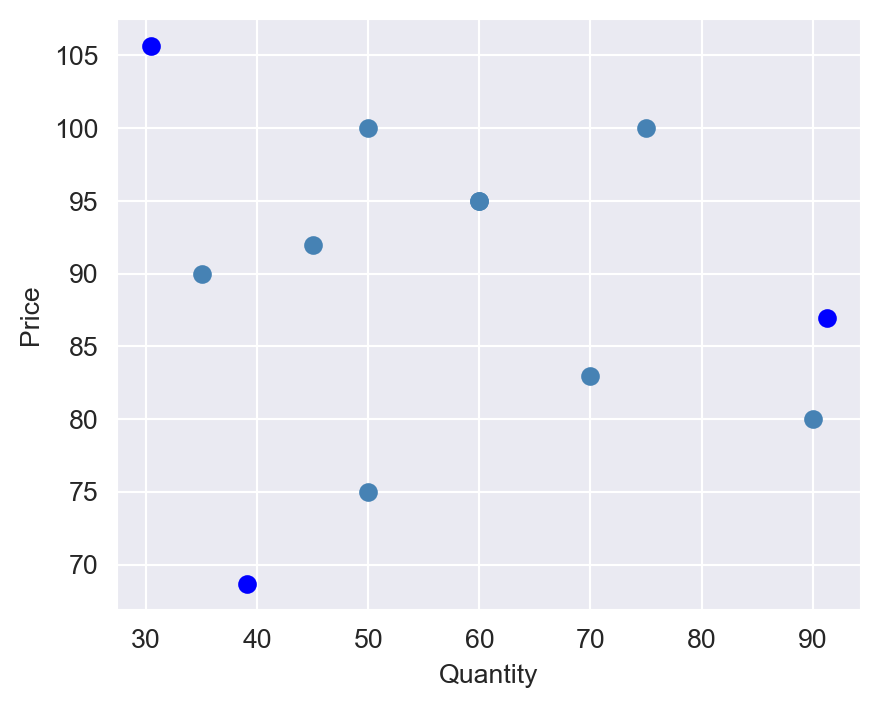

In Figure 21.1, we plot the supply and demand curves for three periods. At each period, the equilibrium price and quantity are determined by the intersection of the supply and demand curves. In Figure 21.2, we plot the equilibrium price and quantity for 11 periods, where the supply and demand curves are hidden. Philip Wright recognized that fitting a linear regression model to the data would yield neither the demand curve nor the supply curve. The reason is that the price is endogenous; it is determined by the intersection of the supply and demand curves.

Formally, this can be shown by solving the market equilibrium equations for price and quantity. Assume that the supply of butter is given by \(Q^{supply}_i = \gamma_0 + \gamma_1P_i + v_i\), where \(v_i\) is an error term independent of \(u_i\). The equilibrium price and quantity are determined by the intersection of the supply and demand curves, i.e., \(Q^{demand}_i = Q^{supply}_i\). The equilibrium condition gives \[ \begin{align} P_i=\frac{\beta_0-\gamma_0}{\gamma_1-\beta_1}+ \frac{u_i-v_i}{\gamma_1-\beta_1}. \end{align} \]

Thus, \(\text{Cov}(P_i, u_i)=\sigma^2_u/(\gamma_1-\beta_1)\), where \(\sigma^2_u\) is the variance of \(u_i\). This implies that the price is correlated with the error term, i.e., the price is endogenous.

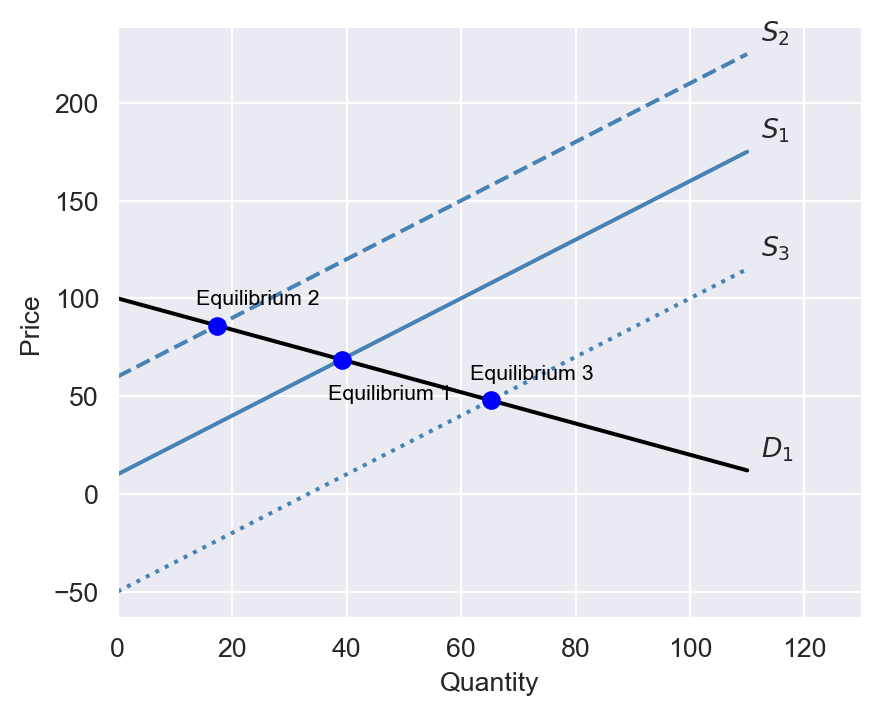

Philip Wright suggested identifying another variable that shifts the supply curve but does not affect the demand curve. In Figure 21.3, we illustrate the equilibrium price and quantity when this variable shifts the supply curve over three periods. Using this approach, the demand curve can be identified, allowing us to determine the demand elasticity for butter (the slope of the demand curve).

The variable that shifts the supply curve is referred to as an instrumental variable. Since the instrumental variable shifts the supply curve, it is correlated with the price. However, it is uncorrelated with the error term because it does not influence the demand curve. Philip Wright proposed several potential instrumental variables. One such variable he suggested was below-average rainfall in a dairy region, which could affect the supply of butter but is unlikely to influence the demand for butter.

In Example 21.1, the price of butter is endogenous because it is determined by the intersection of the supply and demand curves. In general, if the dependent variable and the regressor of interest are determined simultaneously, then the regressor of interest is endogenous.

Example 21.2 (Wage and education) Assume that \(Y_i\) is the wage of individual \(i\) and \(X_i\) is the years of education of individual \(i\). In this classical wage equation, the error term \(u_i\) captures unobserved factors that affect wages, such as ability or family background. Since ability and family background are likely to be correlated with education, the education level becomes endogenous.

In Example 21.2, the education level is endogenous because it is correlated with the error term. In general, if the dependent variable and the regressor of interest are choice variables of the same individual, then the regressor of interest is endogenous (Hansen (2022)).

21.2.1 The two stage least squares estimator

Using the instrumental variable \(Z_i\), we can use the two-stage least squares (TSLS) estimator to consistently estimate \(\beta_1\). The TSLS method involves two stages:

First stage: To isolate the part of \(X\) that is uncorrelated with \(u\), we regress \(X\) on \(Z\) using the OLS estimator: \[ \begin{align} X_i=\pi_0+\pi_1Z_i+v_i, \end{align} \] where \(\pi_0\) and \(\pi_1\) are the unknown parameters and \(v_i\) is an error term. Then, we compute the predicted values \(\hat{X}_i=\hat{\pi}_0+\hat{\pi}_1Z_i\), where \(\hat{\pi}_0\) and \(\hat{\pi}_1\) are the OLS estimators of \(\pi_0\) and \(\pi_1\), respectively.

Second stage: We replace \(X_i\) by \(\hat{X}_i\) in \(Y_i=\beta_0+\beta_1X_i+u_i\), and use the OLS estimator to estimate \(\beta_1\) in the following regression: \[ \begin{align} Y_i=\beta_0+\beta_1\hat{X}_i+u_i. \end{align} \]

Definition 21.3 (Two-stage least squares (TSLS) estimator) The OLS estimators \(\hat{\beta}^{TSLS}_0\) and \(\hat{\beta}^{TSLS}_1\) obtained from the second stage are called the TSLS estimators.

Recall that the OLS estimator of \(\beta_1\) in the model \(Y_i=\beta_0+\beta_1X_i+u_i\) is given by \(\hat{\beta}_1=\frac{s_{XY}}{s^2_X}\), where \(s_{XY}\) is the sample covariance between \(Y\) and \(X\) and \(s^2_X\) is the sample variance of \(X\). Applying this formula to the second stage, we obtain

\[

\begin{align}

\hat{\beta}^{TSLS}_1=\frac{s_{\hat{X}Y}}{s^2_{\hat{X}}}.

\end{align}

\tag{21.1}\]

To determine \(s_{\hat{X}Y}\) and \(s^2_{\hat{X}}\), we use the predicted equation \(\hat{X}=\hat{\pi}_0+\hat{\pi}_1Z\) from the first stage: \[ \begin{align*} &s_{\hat{X}Y}=\text{Cov}(\hat{X},Y)=\text{Cov}(\hat{\pi}_0+\hat{\pi}_1Z,Y)=\hat{\pi}_1\text{Cov}(Z,Y)=\hat{\pi}_1s_{ZY},\\ &s^2_{\hat{X}}=\text{Var}(\hat{X})=\text{Var}(\hat{\pi}_0+\hat{\pi}_1Z)=\hat{\pi}^2_1s^2_{Z}. \end{align*} \]

Also, from the first stage, we have \(\hat{\pi}_1=\frac{s_{ZX}}{s^2_Z}\implies s^2_Z=s_{ZX}/\hat{\pi}_1\). Then, using \(s_{\hat{X}Y}=\hat{\pi}_1s_{ZY}\) and \(s^2_{\hat{X}}=\hat{\pi}^2_1s_{ZX}/\hat{\pi}_1=\hat{\pi}_1s_{ZX}\) in Equation 21.1, we derive \(\hat{\beta}^{TSLS}_1\) as \[ \begin{align}\label{eq4} \hat{\beta}^{TSLS}_1=\frac{s_{ZY}}{s_{ZX}}. \end{align} \tag{21.2}\]

That is, \(\hat{\beta}^{TSLS}_1\) is given by the ratio of the sample covariance between \(Z\) and \(Y\) and the sample covariance between \(Z\) and \(X\).

21.2.2 The sampling distribution of the TSLS estimator

We first establish the consistency of the TSLS estimator and then show the asymptotic distribution of the TSLS estimator. The population covariance between \(Z\) and \(X\) is given by \[ \begin{align*} \text{Cov}(Z,Y)&=\text{Cov}(Z,\beta_0+\beta_1X+u)\\ &=\beta_1\text{Cov}(Z,X)+\text{Cov}(Z,u)=\beta_1\text{Cov}(Z,X)\\ &\implies\beta_1=\frac{\text{Cov}(Z,Y)}{\text{Cov}(Z,X)}=\frac{\sigma_{ZY}}{\sigma_{ZX}}, \end{align*} \]

where \(\sigma_{ZY}\) and \(\sigma_{ZX}\) are the population covariance between \(Z\) and \(Y\) and between \(Z\) and \(X\), respectively. Then, using Equation 21.2, we have \[ \begin{align} \hat{\beta}^{TSLS}_1=\frac{s_{ZY}}{s_{ZX}}\xrightarrow{p}\frac{\sigma_{ZY}}{\sigma_{ZX}}=\beta_1, \end{align} \tag{21.3}\]

because \(s_{ZY}\xrightarrow{p}\sigma_{ZY}\) and \(s_{ZX}\xrightarrow{p}\sigma_{ZX}\) as \(n\to\infty\) by the law of large numbers. Thus, the TSLS estimator is a consistent estimator of \(\beta_1\).

Next, using \(Y_i-\bar{Y}=\beta_1(X_i-\bar{X})+(u_i-\bar{u})\), we can show that \[ \begin{align} s_{ZY}&=\frac{1}{n-1}\sum^n_{i=1}(Z_i-\bar{Z})(Y_i-\bar{Y})\\ &=\beta_1\frac{1}{n-1}\sum^n_{i=1}(Z_i-\bar{Z})(X_i-\bar{X})+\frac{1}{n-1}\sum^n_{i=1}(Z_i-\bar{Z})(u_i-\bar{u})\\ &= \beta_1s_{ZX}+\frac{1}{n-1}\sum^n_{i=1}(Z_i-\bar{Z})u_i. \end{align} \]

Then, the TSLS estimator can be written as (for large \(n\)) \[ \begin{align} &\hat{\beta}^{TSLS}_1=\frac{\beta_1s_{ZX}+\frac{1}{n}\sum^n_{i=1}(Z_i-\bar{Z})u_i}{s_{ZX}}=\beta_1+\frac{1}{n}\frac{\sum^n_{i=1}(Z_i-\bar{Z})u_i}{s_{ZX}}\\ &\implies\sqrt{n}(\hat{\beta}^{TSLS}_1-\beta_1)=\frac{\frac{1}{\sqrt{n}}\sum^n_{i=1}(Z_i-\bar{Z})u_i}{s_{ZX}}\approx \frac{\frac{1}{\sqrt{n}}\sum^n_{i=1}q_i}{\sigma_{ZX}}, \end{align} \] where \(q_i=(Z_i-\mu_Z)u_i\). Then, we can extend the argument for the distribution of the OLS estimator to show that the sampling distribution of \(\hat{\beta}^{TSLS}_1\) is approximated by \(N(\beta_1, \sigma^2_{\hat{\beta}^{TSLS}_1})\), where \[ \sigma^2_{\hat{\beta}^{TSLS}_1}=\frac{1}{n}\frac{\text{Var}\left((Z_i-\mu_Z)u_i\right)}{\left(\text{Cov}(Z_i,X_i)\right)^2}. \]

This variance can be consistently estimated by using the sample counterparts: \[ \begin{align} \hat{\sigma}^2_{\hat{\beta}^{TSLS}_1}=\frac{1}{n}\frac{\frac{1}{n-1}\sum^n_{i=1}(\hat{q}_i-\bar{\hat{q}})^2}{s^2_{ZX}}, \end{align} \]

where \(\hat{q}_i=(Z_i-\bar{Z})\hat{u}_i\) and \(\hat{u}_i=Y_i-\hat{\beta}^{TSLS}_0-\hat{\beta}^{TSLS}_1X_i\) is the residual from the TSLS regression. We can use this variance to construct confidence intervals and perform hypothesis tests, similar to the procedure used in multiple linear regression models.

21.2.3 Application to the demand for cigarettes

We estimate the price elasticity of demand for cigarettes using the instrumental variable method. The data set consists of annual data for the 48 continental U.S. states from 1985 to 1995. Cigarette consumption is measured by annual per capita cigarette sales in packs per year. The price is the average retail cigarette price per pack during the fiscal year, including taxes. The data set is included in the cig_ch12.xlsx file. The variables are as follows:

| Variable | Description |

|---|---|

state |

State |

year |

Year |

cpi |

Consumer price index |

pop |

State population |

packpc |

Number of packs per capita |

income |

State personal income (total, nominal) |

tax |

Average state, federal, and average local excise taxes for fiscal year |

avgprs |

Average price during fiscal year, including sales taxes |

taxs |

Average excise taxes for fiscal year, including sales taxes |

We use real variables by deflating the nominal variables by the consumer price index. We consider the following demand equation for cigarette consumption: \[ \begin{align} \ln(Q^{cigarettes}_i)=\beta_0+\beta_1\ln(P^{cigarettes}_i)+u_i, \end{align} \tag{21.4}\]

where \(Q^{cigarettes}_i\) is the number of packs of cigarettes sold per capita in the \(i\)th state and \(P^{cigarettes}_i\) is the average real price per pack of cigarettes including all taxes. The price is endogenous because it is determined by the intersection of the supply and demand curves, as we illustrated in Example 21.1. We can use the general sales tax as an instrumental variable for the price. The general sales tax is a tax applied to all consumption goods, including cigarettes. We need to ensure that the general sales tax is correlated with the price but uncorrelated with the error term.

Instrument relevance: An increase in general sales tax should increase the price of cigarettes, suggesting that \(\text{Cov}(\text{SalesTax}_i, P^{cigarettes}_i)\neq 0\). Thus, the general sales tax is a relevant instrument.

Instrument exogeneity: We need to show that the general sales tax affects the demand for cigarettes only through its effect on the price. This assumption is plausible because general sales tax rates vary across states and are usually set based on the state’s fiscal policies. Therefore, the general sales tax is likely to be uncorrelated with the factors that affect cigarette consumption.

We use the following code chunk to import data and generate (i) the real cigarettes prices, (ii) the real sales taxes, and (iii) the real per-capita income.The summary statistics of variables are shown in Table 21.2.

# Import data

mydata <- read_excel("data/cig_ch12.xlsx")

# Column names

colnames(mydata)[1] "state" "year" "cpi" "pop" "packpc" "income" "tax" "avgprs"

[9] "taxs" # Generate real cigarette prices

mydata$rprice <- mydata$avgprs / mydata$cpi

# Generate real sales tax

mydata$salestax <- (mydata$taxs - mydata$tax) / mydata$cpi

# Generate real cigarette tax

mydata$cigtax <- mydata$tax / mydata$cpi

# Generate real per capita income

mydata$rincome <- (mydata$income / mydata$pop) / mydata$cpi# Variables of interest

variables <- c("rprice", "salestax", "cigtax", "rincome", "packpc")

# Summary statistics

datasummary_skim(

mydata[, variables],

stats = c("n", "mean", "sd", "min", "max"),

fmt = 2

)| Unique | Missing Pct. | Mean | SD | Min | Median | Max | |

|---|---|---|---|---|---|---|---|

| rprice | 96 | 0 | 108.28 | 17.36 | 78.97 | 103.54 | 158.04 |

| salestax | 78 | 0 | 4.13 | 2.93 | 0.00 | 4.79 | 10.26 |

| cigtax | 64 | 0 | 32.33 | 8.66 | 16.73 | 31.17 | 64.96 |

| rincome | 96 | 0 | 13.81 | 2.14 | 9.22 | 13.67 | 20.96 |

| packpc | 96 | 0 | 109.18 | 25.87 | 49.27 | 110.16 | 197.99 |

To estimate Equation 21.4, we only use data from the year 1995. We use the ivreg function from the AER package to perform the IV regression.

According to estimation results in Table 21.3, the estimated model is \[ \begin{align} \widehat{\ln(Q^{cigarettes}_i)}=9.720-1.084\ln(P^{cigarettes}_i). \end{align} \]

The TSLS estimate \(\hat{\beta}^{TSLS}_1=-1.084\) suggests that a one percent increase in cigarette prices reduces cigarette consumption by approximately 1.08 percent, indicating that demand is fairly elastic.

# Display results

modelsummary(

models = list("Model" = iv_model),

vcov = "HC1",

stars = TRUE,

fmt = 3,

gof_omit = "AIC|BIC|Log.Lik"

)| Model | |

|---|---|

| (Intercept) | 9.720*** |

| (1.528) | |

| log(rprice) | -1.084** |

| (0.319) | |

| Num.Obs. | 48 |

| R2 | 0.401 |

| R2 Adj. | 0.388 |

| RMSE | 0.19 |

| Std.Errors | HC1 |

| + p < 0.1, * p < 0.05, ** p < 0.01, *** p < 0.001 | |

21.3 The general IV regression model

In this section, we extend the IV regression model to include multiple endogenous variables and multiple instruments. Consider the following multiple linear regression model: \[ \begin{align} Y_i = \beta_0 + \beta_1X_{1i}+\ldots+\beta_kX_{ki}+\beta_{k+1}W_{1i} +\ldots + \beta_{k+r}W_{ri} + u_i, \end{align} \tag{21.5}\]

where \(Y_i\) is the dependent variable, \(X_{1i},\ldots,X_{ki}\) are the endogenous variables, and \(W_{1i},\ldots,W_{ri}\) are either exogenous variables or the control variables. The endogenous variables are correlated with the error term, i.e., \(\text{Cov}(X_{ji},u_i)\neq 0\) for \(j=1,\ldots,k\). We use the instrumental variables \(Z_{1i},\ldots,Z_{mi}\) for the endogenous variables. In this model, the coefficients \(\beta_1,\ldots,\beta_k\) are said to be:

- exactly identified if \(m = k\). There are just enough instruments to estimate \(\beta_1,\ldots,\beta_k\).

- overidentified if \(m > k\). There are more than enough instruments to estimate \(\beta_1,\ldots,\beta_k\). In this case, we can also test whether the instruments are valid (a test of the overidentifying restrictions), which we will discuss later.

- underidentified if \(m < k\). There are too few instruments to estimate \(\beta_1,\ldots,\beta_k\).

In order to use the IV method to estimate the coefficients in Equation 21.5, the coefficients must either be exactly identified or overidentified. The IV method is not applicable when the coefficients are underidentified.

21.3.1 TSLS in the general IV model

There are two stages to compute the TSLS estimator for the general IV regression model:

- First-stage regression(s): For the \(j\)-th endogenous regressor, estimate the following regression by the OLS estimator: \[ \begin{align} X_{ji}=\pi_{0j}+\pi_{1j}Z_{1i}+\ldots+\pi_{mj}Z_{mi}+\gamma_{1j}W_{1i}+\ldots+\gamma_{rj}W_{ri}+v_{ji}, \end{align} \] where \(\pi_{0j},\ldots,\pi_{mj}\) and \(\gamma_{1j},\ldots,\gamma_{rj}\) are the unknown parameters, and \(v_{ji}\) is the error term. This model is sometimes called the reduced form equation. Then, compute the predicted values \[ \hat{X}_{ji}=\hat{\pi}_{0j}+\hat{\pi}_{1j}Z_{1i}+\ldots+\hat{\pi}_{mj}Z_{mi}+ \hat{\gamma}_{1j}W_{1i}+\ldots+\hat{\gamma}_{rj}W_{ri}. \]

Repeat this for all the endogenous regressors \(X_{2i},\ldots,X_{ki}\), thereby computing the predicted values \(\hat{X}_{1i},\ldots,\hat{X}_{ki}\).

- Second-stage regression: Estimate the following regression by the OLS estimator: \[ \begin{align} Y_i=\beta_0+\beta_1\hat{X}_{1i}+\ldots+\beta_k\hat{X}_{ki}+\beta_{k+1}W_{1i}+\ldots+\beta_{k+r}W_{ri}+u_i. \end{align} \]

Definition 21.4 (The TSLS estimator in the general IV model) The TSLS estimators \(\hat{\beta}^{TSLS}_0,\hat{\beta}^{TSLS}_1,\ldots,\hat{\beta}^{TSLS}_{k+r}\) in the general IV regression model are the OLS estimators obtained from the second-stage regression.

21.3.2 Instrument relevance and exogeneity in the general IV model

Valid instruments should be relevant and exogenous. In the general IV regression model with instruments \(Z_1,\ldots,Z_m\), these conditions take the following form:

- Instrument relevance: Consider the following \(n\times (k+r+1)\) matrix: \[ \begin{align} \begin{pmatrix} 1 & \hat{X}_{11} & \ldots & \hat{X}_{k1} & W_{11} & \ldots & W_{r1}\\ \vdots & \ddots & \vdots & \vdots & \ddots & \vdots \\ 1 & \hat{X}_{1n} & \ldots & \hat{X}_{kn} & W_{1n} & \ldots & W_{rn} \end{pmatrix}. \end{align} \tag{21.6}\]

This matrix should have full column rank, i.e., the columns of the matrix are linearly independent. This condition corresponds to the no-perfect multicollinearity assumption and ensures that we can use the OLS estimator to estimate the second stage regression. If there is only one endogenous regressor, then at least one of the instrumental variables must be relevant for the endogenous regressor in the reduced form equation.

- Instrument exogeneity: The instrumental variables must be uncorrelated with the error term: \(\text{Cov}(Z_{l},u)=0\) for \(l=1,\ldots,m\).

21.3.3 The sampling distribution of the TSLS estimator in the general IV model

The IV regression assumptions are the extension of those for the multiple linear regression model and ensure that the TSLS estimator is consistent and has an asymptotic normal distribution. In the following callout block, we state the IV regression assumptions for the general IV model.

Under these four assumptions, the TSLS estimator is consistent and has an asymptotic normal distribution. In Chapter 28, we will use the IV regression assumptions to derive the asymptotic distribution of the TSLS estimator in the general IV model.

In Assumption 1, we assume that \(W_1,\ldots,W_r\) are exogenous variables that are uncorrelated with the error term. We can adjust this assumption if these variables are control variables that are included into the model to ensure that the instrumental variables become uncorrelated with the error term. In that case, the first assumption is replaced by the following conditional mean independence assumption: \[ \begin{align} \E\left(u_i|W_{1i},\ldots,W_{ri},Z_{1i},\ldots,Z_{mi}\right)=\E(u_i|W_{1i},\ldots,W_{ri}). \end{align} \]

Because the control variables can be correlated with the error term, the coefficients on these variables do not have a causal interpretation.

Let us assume that there is only one endogenous and one control variable such that \[ \begin{align} Y_i = \beta_0 + \beta_1X_i + \beta_2W_i + u_i. \end{align} \tag{21.7}\]

In this case, we can replace Assumption 1 with the following conditional mean independence assumption: \[ \begin{align} \E\left(u_i|W_i,Z_i\right)=\E(u_i|W_i). \end{align} \tag{21.8}\]

Under the assumption that \(\E(u_i|W_i)=\gamma_0+\gamma_1W_i\), we can rewrite Equation 21.7 as \[ \begin{align} Y_i &= \beta_0 + \beta_1X_i + \beta_2W_i +u_i-\E(u_i|W_i,Z_i)+\E(u_i|W_i,Z_i)\\ &= \beta_0 + \beta_1X_i + \beta_2W_i + \gamma_0 + \gamma_1W_i + \varepsilon_i\\ &= \delta_0 + \beta_1X_i + \delta_1W_i + \varepsilon_i, \end{align} \tag{21.9}\]

where \(\delta_0=(\beta_0+\gamma_0)\), \(\delta_1=(\beta_2+\gamma_1)\), and \(\varepsilon_i=u_i-\E(u_i|W_i,Z_i)\) is the error term in the model. Note that \[ \begin{align} \E(\varepsilon_i|W_i,Z_i)&=\E(u_i-\E(u_i|W_i,Z_i)|W_i,Z_i)\\ &=\E(u_i|W_i,Z_i)-\E(u_i|W_i,Z_i)=0, \end{align} \]

which implies that \(\text{Cov}(\varepsilon_i,Z_i)=0\). Thus, if we replace Assumption 1 with the conditional mean independence assumption in Equation 21.8, the IV regression assumptions are satisfied and we can use the TSLS estimator to estimate the coefficients in Equation 21.9. Note that the TSLS estimator only consistently estimates \(\delta_0\), \(\beta_1\), and \(\delta_1=(\beta_2+\gamma_1)\) in Equation 21.9. In particular, we do not have a consistent estimator for \(\beta_2\).

21.3.4 Application to the demand for cigarettes

We extend the cigarette demand model to include real per capita income as an additional regressor. Recall that we use the sales tax as an instrument for the average real price in the demand equation stated in Equation 21.4. However, if real income is correlated with the sales tax, then the sales tax is not a valid instrument for real prices in Equation 21.4. Therefore, we need to extend the demand equation to include real per capita income as an additional regressor: \[ \begin{align} \ln(Q^{cigarettes}_i)=\beta_0+\beta_1\ln(P^{cigarettes}_i)+\beta_2\ln(\text{Income}_i)+u_i. \end{align} \tag{21.10}\]

where \(\text{Income}_i\) is the real per capita income in state \(i\). We use the ivreg function to estimate the extended demand equation, where we use the sales tax as an instrument for the real price and include real per capita income as a control variable. Note that in the formula for the ivreg function, we specify the control variable log(rincome) in both the first stage and the second stage.

The estimation results are shown in Table 21.4. The estimated model is \[ \begin{align} \widehat{\ln(Q^{cigarettes}_i)}=9.43-1.143\ln(P^{cigarettes}_i)+0.215\ln(\text{Income}_i). \end{align} \]

The TSLS estimate \(\hat{\beta}^{TSLS}_1=-1.143\) suggests that a one percent increase in cigarette prices reduces cigarette consumption by approximately \(1.14\) percent, holding real income constant.

# Display results

modelsummary(

models = list("Model" = iv_model2),

vcov = "HC1",

stars = TRUE,

fmt = 3,

gof_omit = "AIC|BIC|Log.Lik"

)| Model | |

|---|---|

| (Intercept) | 9.431*** |

| (1.259) | |

| log(rincome) | 0.215 |

| (0.312) | |

| log(rprice) | -1.143** |

| (0.372) | |

| Num.Obs. | 48 |

| R2 | 0.419 |

| R2 Adj. | 0.393 |

| RMSE | 0.18 |

| Std.Errors | HC1 |

| + p < 0.1, * p < 0.05, ** p < 0.01, *** p < 0.001 | |

The model in Equation 21.4 is exatcly identified because there is only one endogenous variable and one instrument. In addition to this instrument, we can use the cigarette-specific tax as an additional instrument. We use the following code chunk to estimate the model using both the sales tax and the cigarette-specific tax as instruments.

The estimation results are shown in Table 21.5. The estimated model is \[ \begin{align} \widehat{\ln(Q^{cigarettes}_i)}=9.89-1.277\ln(P^{cigarettes}_i)+0.280\ln(\text{Income}_i). \end{align} \]

The TSLS estimate \(\hat{\beta}^{TSLS}_1=-1.277\) suggests that a one percent increase in cigarette prices reduces cigarette consumption by approximately 1.28 percent, holding real income constant.

# Display results

modelsummary(

models = list("Model" = iv_model3),

vcov = "HC1",

stars = TRUE,

fmt = 3,

gof_omit = "AIC|BIC|Log.Lik"

)| Model | |

|---|---|

| (Intercept) | 9.895*** |

| (0.959) | |

| log(rincome) | 0.280 |

| (0.254) | |

| log(rprice) | -1.277*** |

| (0.250) | |

| Num.Obs. | 48 |

| R2 | 0.429 |

| R2 Adj. | 0.404 |

| RMSE | 0.18 |

| Std.Errors | HC1 |

| + p < 0.1, * p < 0.05, ** p < 0.01, *** p < 0.001 | |

The validity of the estimation results presented in Table 21.4 and Table 21.5 depends on the validity of the instruments. In the next section, we discuss how to check the validity of the instruments.

21.4 Checking instrument validity

Recall that we need two conditions for the instrumental variables to be valid: (i) instrument relevance and (ii) instrument exogeneity. Assume that there is only one endogenous variable and multiple instruments. In this case, the first stage regression (the reduced form equation) is \[ \begin{align} X_i=\pi_0+\pi_1Z_i+\ldots+\pi_mZ_i+\gamma_1W_i+\ldots+\gamma_rW_i+v_i, \end{align} \tag{21.11}\]

where \(\pi_0,\ldots,\pi_m\) and \(\gamma_1,\ldots,\gamma_r\) are the unknown parameters, and \(v_i\) is the error term. Then, the instruments are relevant if at least one of \(\pi_1,\ldots,\pi_m\) is not zero. The instruments are said to be weak if all of \(\pi_1,\ldots,\pi_m\) are zero or close to zero. That is, in the weak instrument case, the instruments can only explain a small portion of the variation in the endogenous variable.

In practice, we can use the F-statistic from the first stage regression to test the instrument relevance condition. Consider the following null and alternative hypotheses: \[ \begin{align} H_0&: \pi_1=\ldots=\pi_m=0,\\ H_1&: \text{At least one of the coefficients is not zero}. \end{align} \]

A large F-statistic indicates that the instruments are relevant. A common rule of thumb is that the F-statistic should be greater than 10. An F-statistic smaller than 10 suggests that the instruments are weak. In such cases, the TSLS estimator is biased and does not have an asymptotic normal distribution, even when the sample size is large.

To study the large sample distribution of the TSLS estimator under the weak instrument, we consider the case where there is only one endogenous variable and one instrument. In this case, we start with the following expression for the TSLS estimator: \[ \begin{align} &\hat{\beta}^{TSLS}_1=\beta_1+\frac{\frac{1}{n}\sum^n_{i=1}(Z_i-\bar{Z})u_i}{\frac{1}{n}\sum^n_{i=1}(Z_i-\bar{Z})(X_i-\bar{X})}\approx \beta_1+\frac{\frac{1}{n}\sum^n_{i=1}q_i}{\frac{1}{n}\sum^n_{i=1}r_i}, \end{align} \tag{21.12}\]

where \(q_i=(Z_i-\mu_Z)u_i\) and \(r_i=(Z_i-\mu_Z)(X_i-\mu_X)\). Let \(\sigma^2_q=\var(q_i)\), \(\sigma^2_r=\var(r_i)\), \(\bar{q}=\frac{1}{n}\sum^n_{i=1}q_i\), and \(\bar{r}=\frac{1}{n}\sum^n_{i=1}r_i\). Then, under Assumption 2, we have \(\var(\bar{q})=\sigma^2_q/n\) and \(\var(\bar{r})=\sigma^2_r/n\). Thus, we express Equation 21.12 as \[ \begin{align} \hat{\beta}^{TSLS}_1=\beta_1+\frac{\bar{q}}{\bar{r}}=\beta_1+\frac{\sigma_q}{\sigma_r}\frac{\bar{q}/\sigma_q}{\bar{r}/\sigma_r}. \end{align} \tag{21.13}\]

If the instrument is irrelevant, then \(\E(r_i) = \E((Z_i - \mu_Z)(X_i - \mu_X)) = 0\). Additionally, by the exogeneity condition, we have \(\E(q_i) = 0\). Thus, under Assumptions 2 and 3, we can apply the CLT to show that \(\bar{r}/\sigma_r \xrightarrow{d} N(0,1)\) and \(\bar{q}/\sigma_q \xrightarrow{d} N(0,1)\). Therefore, in large samples, the distribution of \(\hat{\beta}^{TSLS}_1 - \beta_1\) is approximately that of \((\sigma_q / \sigma_r) S\), where \(S\) is the ratio of two random variables, each following a standard normal distribution. This extreme case also sheds light on the large sample distribution of the TSLS estimator when the instruments are weak. Specifically, when the instruments are weak but not irrelevant, the large-sample distribution of the TSLS estimator is non-normal.

Also, in the extreme case where the instrument is strong but endogenous, the TSLS estimator is inconsistent. This can be see from the following expression: \[ \begin{align} \hat{\beta}^{TSLS}_1&=\beta_1+\frac{\frac{1}{n}\sum^n_{i=1}(Z_i-\mu_Z)u_i}{\frac{1}{n}\sum^n_{i=1}(Z_i-\mu_Z)(X_i-\mu_X)}\xrightarrow {p} \beta_1+\frac{\E((Z_i-\mu_Z)u_i)}{\E((Z_i-\mu_Z)(X_i-\mu_X))}\\ &=\beta_1+\frac{\cov(Z_i,u_i)}{\cov(Z_i,X_i)}\neq \beta_1. \end{align} \]

In the exactly identified case, we cannot use any statistical test to verify whether the instruments are exogenous. Instead, we must rely on economic theory and expert judgment to justify the exogeneity of the instruments. In the overidentified case, however, we can employ the test of overidentifying restrictions (also known as the J test) to assess the instrument exogeneity condition. The test can be computed in the following way:

- Compute the TSLS estimators \(\hat{\beta}^{TSLS}_0,\ldots,\hat{\beta}^{TSLS}_{k+r}\).

- Compute \(\hat{u}^{TSLS}_i=Y_i-(\hat{\beta}^{TSLS}_0+\hat{\beta}^{TSLS}_0X_{1i}+\ldots+\hat{\beta}^{TSLS}_{k+r}W_{ri})\).

- Run the following regression \[ \begin{align} \hat{u}^{TSLS}_i= \delta_0 + \delta_1Z_{1i}+\ldots+ \delta_mZ_{mi} + \delta_{m+1}W_{1i} +\ldots+ \delta_{m+r}W_{ri} + e_i, \end{align} \tag{21.14}\] where \(\delta_0,\ldots,\delta_{m+r}\) are the unknown coefficients and \(e_i\) is the error term.

- Compute the homoskedasticity-only F-statistic for the following hypothesis: \[ \begin{align*} H_0:\delta_1=0,\ldots,\delta_m=0\quad\text{versus}\quad H_1: \text{At least one coefficient is non-zero}. \end{align*} \]

- The J-statistic is computed as \(J=m\times F\), where \(m\) is the number of instruments.

Under the null hypothesis that all instruments are exogeneous, the J statistic has a chi-squared distribution with m-k degrees of freedom, i.e., \(J\sim \chi^2_{m-k}\).

21.5 Application to the demand for cigarettes

In this section, we revisit the demand for cigarettes using the instrumental variable method. We will consider both the sales tax and the cigarette-specific tax as instruments for the average real price. The relevance of these instruments was discussed in previous examples.

The first step in checking instrument exogeneity is to consider the factors that are likely to affect cigarette consumption, i.e., the factors included in the error term \(u_i\). If these factors are correlated with the instruments, then the instruments are not exogenous. For instance, real state income is likely to influence cigarette consumption and may also be correlated with the sales tax and the cigarette-specific tax. Consequently, it is essential to account for real state income in the demand equation; otherwise, the instruments will not satisfy the exogeneity condition. We also use the state fixed effects to control for unobserved omitted factors that vary across states but not over time. Finally, we will consider the J-test to test the instrument exogeneity condition.

21.5.1 Model

We consider the following fixed effects panel data model: \[ \begin{align} \ln(Q^{cigarettes}_{it})=\beta_1\ln(P^{cigarettes}_{it})+\beta_2\ln({\tt Income}_{it})+\alpha_i+u_{it}, \end{align} \]

where

- \(\ln({\tt Income}_{it})\) is the logarithm of real per capita income in state \(i\) at time \(t\),

- \(\alpha_i\) is the \(i\)th state fixed effect, which reflects unobserved omitted factors that vary across states but not over time, e.g. attitude towards smoking.

We are interested in estimating the long-run price elasticity of demand for cigarettes, \(\beta_1\). One way to model long-term effects is to consider 10-year changes, between 1985 and 1995. Thus, in the ``changes’’ form, the demand equation can be written as \[ \begin{align} &\ln(Q^{cigarettes}_{i1995})-\ln(Q^{cigarettes}_{i1985})=\beta_1(\ln(P^{cigarettes}_{i1995})-\ln(P^{cigarettes}_{i1985}))\\ &+\beta_2\left(\ln({\tt Income}_{i1995})-\ln({\tt Income}_{i1985})\right)+(u_{i1995}-u_{i1985}). \end{align} \tag{21.15}\]

We first create the 10-year change variables and then estimate the demand elasticity using the TSLS estimator with the 10-year changes in the instrumental variables.

# Subset data for years 1995 and 1985

mydata1995 <- mydata[mydata$year == 1995, ]

mydata1985 <- mydata[mydata$year == 1985, ]

# Compute 10-year change variables

packdiff <- log(mydata1995$packpc) - log(mydata1985$packpc)

pricediff <- log(mydata1995$rprice) - log(mydata1985$rprice)

incomediff <- log(mydata1995$rincome) - log(mydata1985$rincome)

salestaxdiff <- mydata1995$salestax - mydata1985$salestax

cigtaxdiff <- mydata1995$cigtax - mydata1985$cigtax

# Create a data frame with the differences

diffData <- data.frame(

packdiff = packdiff,

pricediff = pricediff,

incomediff = incomediff,

salestaxdiff = salestaxdiff,

cigtaxdiff = cigtaxdiff

)21.5.2 Estimation

We estimate three models: (i) using only sales taxes as the instrument, (ii) using only the cigarette-specific tax as the instrument, and (iii) using both sales tax and cigarette tax as the instruments.

# Model 1: Instrument = salestaxdiff

model1 <- ivreg(

packdiff ~ incomediff + pricediff | incomediff + salestaxdiff,

data = diffData

)

# Model 2: Instrument = cigtaxdiff

model2 <- ivreg(

packdiff ~ incomediff + pricediff | incomediff + cigtaxdiff,

data = diffData

)

# Model 3: Instruments = salestaxdiff + cigtaxdiff

model3 <- ivreg(

packdiff ~ incomediff + pricediff | incomediff + salestaxdiff + cigtaxdiff,

data = diffData

)The estimation results are shown in Table 21.6. The TSLS estimates for \(\beta_1\) are -0.938, -1.343, and -1.202 for models 1, 2, and 3, respectively. All estimates are statistically significant at the 5% level. The reliability of these coefficient estimates depends on the validity of the instruments. In the next section, we examine the validity of the instruments.

# Display results

modelsummary(

models = list("Model 1" = model1, "Model 2" = model2, "Model 3" = model3),

vcov = "HC1",

stars = TRUE,

fmt = 3,

gof_omit = "AIC|BIC|Log.Lik"

)| Model 1 | Model 2 | Model 3 | |

|---|---|---|---|

| (Intercept) | -0.118+ | -0.017 | -0.052 |

| (0.068) | (0.067) | (0.062) | |

| incomediff | 0.526 | 0.428 | 0.462 |

| (0.339) | (0.299) | (0.309) | |

| pricediff | -0.938*** | -1.343*** | -1.202*** |

| (0.208) | (0.229) | (0.197) | |

| Num.Obs. | 48 | 48 | 48 |

| R2 | 0.550 | 0.520 | 0.547 |

| R2 Adj. | 0.530 | 0.498 | 0.526 |

| RMSE | 0.09 | 0.09 | 0.09 |

| Std.Errors | HC1 | HC1 | HC1 |

| + p < 0.1, * p < 0.05, ** p < 0.01, *** p < 0.001 | |||

21.5.3 Checking instrument validity

The relevance of the instruments can be checked using the F-statistic from the first stage regressions. The code chunk below shows how to compute the F-statistics for the first stage regressions.

# First-stage regressions

f1 <- lm(pricediff ~ salestaxdiff + incomediff, data = diffData)

f2 <- lm(pricediff ~ cigtaxdiff + incomediff, data = diffData)

f3 <- lm(pricediff ~ salestaxdiff + cigtaxdiff + incomediff, data = diffData)

# F-tests

# F-tests

f1_fstat <- linearHypothesis(f1, "salestaxdiff = 0",

vcov = vcovHC,

type = "HC1"

)

f2_fstat <- linearHypothesis(f2, "cigtaxdiff = 0",

vcov = vcovHC,

type = "HC1"

)

f3_fstat <- linearHypothesis(f3, c("salestaxdiff = 0", "cigtaxdiff = 0"),

vcov = vcovHC,

type = "HC1"

)

# Extract F-statistics and p-values

fstats_df <- data.frame(

Model = c(

"Model 1",

"Model 2",

"Model 3"

),

F_statistic = c(

f1_fstat$F[2],

f2_fstat$F[2],

f3_fstat$F[2]

),

df1 = c(

f1_fstat$Df[2],

f2_fstat$Df[2],

f3_fstat$Df[2]

),

df2 = c(

f1_fstat$Res.Df[2],

f2_fstat$Res.Df[2],

f3_fstat$Res.Df[2]

),

p_value = c(

f1_fstat$`Pr(>F)`[2],

f2_fstat$`Pr(>F)`[2],

f3_fstat$`Pr(>F)`[2]

)

)The F-statistics for the first stage regressions are presented in Table 21.7. The first stage F-statistics are 33.7, 107.2, and 86.7 for models 1, 2, and 3, respectively. These F-statistics are greater than 10, indicating that the instruments are relevant.

| Model | F-statistic | df1 | df2 | p-value |

|---|---|---|---|---|

| Model 1 | 28.45 | 1 | 45 | 0 |

| Model 2 | 98.03 | 1 | 45 | 0 |

| Model 3 | 76.92 | 2 | 44 | 0 |

Since the first two models are exactly identified, we cannot use the J-statistic to test instrument exogeneity. However, the regression in column (3) is overidentified because there are two instruments and a single included endogenous regressor, resulting in one (m - k = 2 - 1 = 1) overidentifying restriction. Below, we compute the J-statistic for the overidentifying restriction in model 3.

# J-test for overidentifying restrictions

# Get residuals from Model 3

diffData$residuals <- resid(model3)

# Auxiliary regression

mj <- lm(

residuals ~ salestaxdiff + cigtaxdiff + incomediff,

data = diffData

)

# Joint test of excluded instruments

ftest <- linearHypothesis(mj, c("salestaxdiff = 0", "cigtaxdiff = 0"))

# Extract F-statistic

F_value <- ftest$F[2]

# Number of instruments

m <- 2

# Compute J-statistic

jtest <- m * F_value

# Compute p-value

p_value <- 1 - pchisq(jtest, df = m - 1)# J-test results

jtest_df <- data.frame(

J_statistic = round(jtest, 2),

p_value = round(p_value, 5)

)

kable(jtest_df, align = "cc", col.names = c("J-statistic", "p-value"))| J-statistic | p-value |

|---|---|

| 4.93 | 0.02636 |

The J-test results are presented in Table 21.8. The \(p\)-value indicates that the null hypothesis of both instruments being exogenous is rejected at the 5% significance level. The rejection of the J-statistic suggests that at least one of the instruments is endogenous. This leads to three logical possibilities:

- The sales tax is exogenous, but the cigarette-specific tax is not, making the column (1) regression reliable.

- The cigarette-specific tax is exogenous, but the sales tax is not, making the column (2) regression reliable.

- Neither tax is exogenous, rendering both regressions unreliable.

Stock and Watson (2020) conclude that “We think that the case for the exogeneity of the general sales tax is stronger than that for the cigarette-specific tax because the political process can link changes in the cigarette-specific tax to changes in the cigarette market and smoking policy.”

Finally, both F-statistic from the first stage regression and the J-test for overidentifying restrictions are also returned by the summary function for the ivreg object: summary(model3, diagnostics = TRUE).

21.6 Application to the effect of institutions on economic performance

Acemoglu et al. (2001) investigate the effect of institutions on economic outcomes across countries. They use log GDP per capita in 1995 as a measure of economic outcomes and the average index of protection against expropriation over 1985–95 as a proxy for institutional differences.

In our ensuing analysis, we use three data files: maketable1.dta, maketable2.dta, and maketable4.dta. In Table 21.9, we describe some of the key variables in these datasets.

| Variable | Description |

|---|---|

shortnam |

A three-letter country name. |

euro1900 |

The fraction of the population of European descent in 1900, measuring European settlement in the colonies. |

excolony |

A dummy variable equal to 1 if the country was a colony (FLOPS definition). |

avexpr |

Average protection against expropriation risk over 1985–95 (higher values indicate greater protection). |

logpgp95 |

Log of per capita GDP in 1995 (PPP adjusted). |

extmort4 |

Corrected mortality. |

logem4 |

Log European settler mortality. |

baseco |

Dummy variable for the base sample of countries that were ex-colonies. |

africa |

Dummy variable equal to 1 if the country is in Africa. |

asia |

Dummy variable equal to 1 if the country is in Asia. |

other |

Dummy variable equal to 1 if the country is in neither Asia, Africa, nor the Americas. |

lat_abst |

Absolute latitude (distance from the equator), scaled between 0 and 1, where 0 represents the equator. |

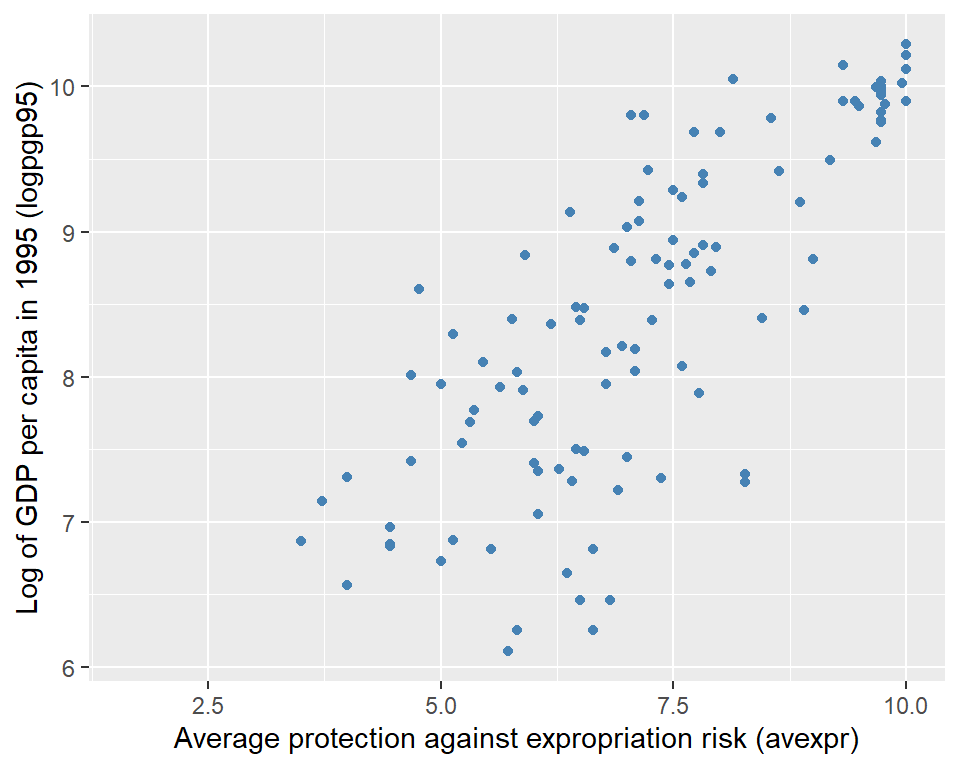

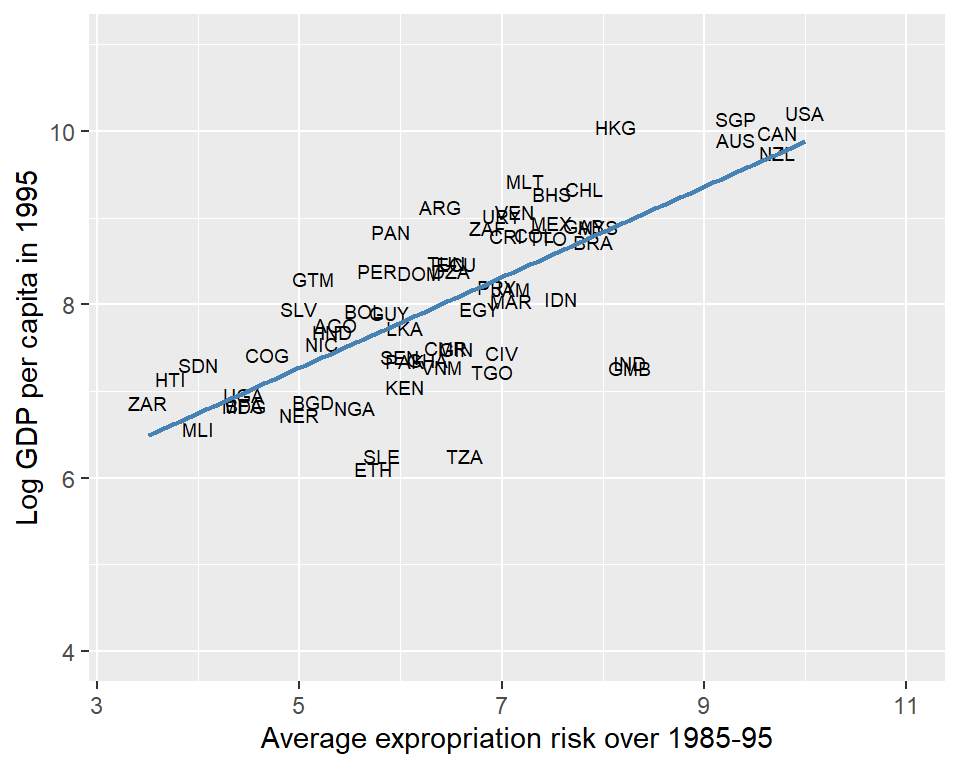

We use the data from maketable1.dta to create a scatter plot of log GDP per capita in 1995 (logpgp95) against the average protection against expropriation risk over 1985-95 (avexpr). The scatter plot is shown in Figure 21.4. The plot reveals a strong positive relationship between protection against expropriation and log GDP per capita. If protection against expropriation is an indicator of institutional quality, then the scatter plot suggests that income per capita is postively associated with institutional quality.

[1] "shortnam" "euro1900" "excolony" "avexpr" "logpgp95" "cons1"

[7] "cons90" "democ00a" "cons00a" "extmort4" "logem4" "loghjypl"

[13] "baseco" # Scatter plot between logpgp95 and avexpr

ggplot(df1, aes(x = avexpr, y = logpgp95)) +

geom_point(color = "steelblue", size = 1.5) +

labs(

x = "Average protection against expropriation risk (avexpr)",

y = "Log of GDP per capita in 1995 (logpgp95)"

)

Given the strong positive relationship in Figure 21.4, we estimate the following OLS regression model: \[ \begin{align*} \text{logpgp95}_i = \beta_0+\beta_1 \text{avexpr}_i + u_i \end{align*} \]

In Figure 21.5, we plot the estimated OLS regression line. The slope coefficient estimate is 0.52, which indicates that a one-unit increase in the average protection against expropriation is associated with a 0.52 increase in log GDP per capita. The coefficient estimate is statistically significant at the 1% level.

# Prepare subset

df1_subset <- df1 %>%

filter(!is.na(logpgp95), !is.na(avexpr), baseco == 1)

# Basic scatter with country labels and OLS line

ggplot(df1_subset, aes(x = avexpr, y = logpgp95, label = shortnam)) +

geom_text(size = 2.5) + # Text labels instead of points

geom_smooth(method = "lm", color = "steelblue", se = FALSE, linewidth = 0.8) +

scale_x_continuous(limits = c(3.3, 11)) +

scale_y_continuous(limits = c(4, 11)) +

labs(

x = "Average expropriation risk over 1985-95",

y = "Log GDP per capita in 1995"

)

Our analysis only considers the impact of avexpr on economic performance. However, numerous other factors influencing income per capita are not included in the model. Omitting these variables that affect logpgp95 can lead to omitted variable bias. Acemoglu et al. (2001) consider the following factors:

- Cultural, historical, and other contextual factors, which are accounted for through the inclusion of continent dummy variables.

- Climate proxied by latitude (

lat_abst).

We estimate some of the extended models considered by Acemoglu et al. (2001) using data in the maketable2.dta file. The results are presented in Table 21.10. The coefficient estimate for the protection against expropriation index is statistically significant at the 1% level across all three models. The relationship remains robust to the inclusion of additional controls, such as geography and continent dummies.

# Load the data

df2 <- read_dta("data/maketable2.dta")

# Model 1: logpgp95 ~ avexpr

reg1 <- lm(logpgp95 ~ avexpr, data = df2)

# Model 2: logpgp95 ~ avexpr + lat_abst

reg2 <- lm(logpgp95 ~ avexpr + lat_abst, data = df2)

# Model 3: logpgp95 ~ avexpr + lat_abst + asia + africa + other

reg3 <- lm(logpgp95 ~ avexpr + lat_abst + asia + africa + other, data = df2)# Display results

modelsummary(

models = list("Model 1" = reg1, "Model 2" = reg2, "Model 3" = reg3),

vcov = "HC1",

stars = TRUE,

fmt = 3,

gof_omit = "AIC|BIC|Log.Lik"

)| Model 1 | Model 2 | Model 3 | |

|---|---|---|---|

| (Intercept) | 4.626*** | 4.873*** | 5.851*** |

| (0.241) | (0.281) | (0.293) | |

| avexpr | 0.532*** | 0.463*** | 0.390*** |

| (0.029) | (0.052) | (0.051) | |

| lat_abst | 0.872+ | 0.333 | |

| (0.499) | (0.442) | ||

| asia | -0.153 | ||

| (0.181) | |||

| africa | -0.916*** | ||

| (0.154) | |||

| other | 0.304+ | ||

| (0.174) | |||

| Num.Obs. | 111 | 111 | 111 |

| R2 | 0.611 | 0.623 | 0.715 |

| R2 Adj. | 0.608 | 0.616 | 0.702 |

| RMSE | 0.71 | 0.70 | 0.61 |

| Std.Errors | HC1 | HC1 | HC1 |

| + p < 0.1, * p < 0.05, ** p < 0.01, *** p < 0.001 | |||

Acemoglu et al. (2001) highlight several critical reasons to exercise caution when interpreting the estimation results given in Table 21.10 as causal:

- Omitted variable bias: There are unobserved determinants of income differences that are naturally correlated with institutions.

- Simultaneous causality bias: Wealthier nations are more likely to invest in and develop better institutional frameworks.

- Error-in-variables bias: The construction of the institutional index may be subject to biases. For instance, analysts might be predisposed to view countries with higher incomes as having superior institutions.

We can solve all of these problems by using a valid instrument for institutions (avexpr). The instrument must be:

- correlated with

avexpr(instrument relevance), - not correlated with the error term \(u\) (instrument exogeneity).

The primary contribution of Acemoglu et al. (2001) lies in their use of “settler mortality rates” (logem4) as an instrument for institutional differences. They propose that settler mortality influenced settlement patterns, which in turn shaped early institutions. These early institutions persisted over time, ultimately forming the foundation of current institutional frameworks.

To check instrument relevance, we generate a scatterplot of avexpr against logem4 (log settler mortality rate). Figure 21.6 reveals a negative correlation between protection against expropriation and settler mortality rates, consistent with the authors’ hypothesis. This negative relationship indicates that higher settler mortality rates are associated with lower levels of protection against expropriation during 1985–95. The first stage F-statistic is 31.5, which is greater than 10, indicating that the instrument is relevant.

# Subset data: drop NA's

df1_subset2 <- df1 %>%

filter(!is.na(logem4), !is.na(avexpr))

# Scatter plot with country labels and OLS line

ggplot(df1_subset2, aes(x = logem4, y = avexpr, label = shortnam)) +

geom_text(size = 2.5) + # text labels instead of points

geom_smooth(method = "lm", color = "steelblue", se = FALSE, linewidth = 0.8) +

scale_x_continuous(limits = c(1.8, 8.4)) +

scale_y_continuous(limits = c(3.3, 10.4)) +

labs(

x = "Log of settler mortality",

y = "Average expropriation risk 1985-95"

)

# First-stage regression

first_stage <- lm(avexpr ~ logem4, data = df1_subset2)

# F-test for first-stage (logem4 = 0)

f_test <- linearHypothesis(first_stage, "logem4 = 0",

vcov = vcovHC,

type = "HC1"

)

f_test

Linear hypothesis test:

logem4 = 0

Model 1: restricted model

Model 2: avexpr ~ logem4

Note: Coefficient covariance matrix supplied.

Res.Df Df F Pr(>F)

1 73

2 72 1 24.449 4.821e-06 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1The instrument exogeneity condition may not be satisfied if settler mortality rates in the 17th to 19th centuries have a direct effect on current GDP (in addition to their indirect effect through institutions). For example, settler mortality rates may be related to the current disease environment in a country, which could affect current economic performance. Acemoglu et al. (2001) argue this is unlikely because:

- The majority of settler deaths were due to malaria and yellow fever and these diseases had a limited effect on local people.

- The disease burden on local people in Africa or India, for example, did not appear to be higher than average, supported by relatively high population densities in these areas before colonization.

Hence, the settler mortality rate variable seem to be a valid instrument and we can proceed with the TSLS estimation. The estimation results are presented in Table 21.11. The estimated coefficient on the protection against expropriation index is 0.94, with a standard error of 0.18. The coefficient is statistically significant at the 5% level. Compared to the OLS estimate (0.53), the TSLS estimate is larger, suggesting that the OLS estimate is biased downwards.

# Display results

modelsummary(

models = list("IV Model" = iv_model),

vcov = "HC1",

stars = TRUE,

fmt = 3,

gof_omit = "AIC|BIC|Log.Lik"

)| IV Model | |

|---|---|

| (Intercept) | 1.910 |

| (1.193) | |

| avexpr | 0.944*** |

| (0.179) | |

| Num.Obs. | 64 |

| R2 | 0.187 |

| R2 Adj. | 0.174 |

| RMSE | 0.93 |

| Std.Errors | HC1 |

| + p < 0.1, * p < 0.05, ** p < 0.01, *** p < 0.001 | |