14 Regression with a Single Regressor: Hypothesis Tests and Confidence Intervals

14.1 Testing hypotheses about one of the regression parameters

A hypothesis is a claim about the true value of a parameter. We are interested in formulating hypotheses about the slope parameter \(\beta_1\) in the simple linear regression model. The null hypothesis states our claim about \(\beta_1\) and is denoted by \(H_0\). For example, the null hypothesis: \(H_0: \beta_{1} = c\) states that \(\beta_1\) is equal to the hypothesized value \(c\). The alternative hypothesis states the scenario in which the null hypothesis does not hold. There are three types of alternative hypotheses:

- Two-sided alternative hypothesis: \(H_1: \beta_{1} \ne c\),

- Left-sided alternative hypothesis: \(H_1: \beta_{1} < c\), and

- Right-sided alternative hypothesis: \(H_1: \beta_{1} > c\).

We use the \(t\)-statistic to test \(H_0\): \[ \begin{align} t=\frac{\text{estimator-hypothesized value}}{\text{standard error of the estimator}}. \end{align} \] Thus, the \(t\)-statistic for testing \(H_0:\beta_1=c\) takes the following form: \[ \begin{align} t = \frac{\hat{\beta}_{1} - c}{\SE(\hat{\beta}_1)}, \end{align} \tag{14.1}\]

where \(\SE(\hat{\beta}_1)\) is the square root of the variance of \(\hat{\beta}_1\). Note that the test statistic \(t\) is formulated under the assumption that \(H_0\) holds.

To compute the \(t\)-statistic in Equation 14.1, we need to determine \(\SE(\hat{\beta}_1)\). In Chapter 13, we show that \[ \begin{align*} &\hat{\beta}_1 \stackrel{A}{\sim} N\left(\beta_1, \sigma^2_{\hat{\beta}_1}\right),\,\text{where}\quad\sigma^2_{\hat{\beta}_1} = \frac{1}{n}\frac{\var\left((X_i - \mu_X)u_i\right)}{\left(\sigma^2_X\right)^2},\\ &\hat{\beta}_0 \stackrel{A}{\sim} N\left(\beta_0, \sigma^2_{\hat{\beta}_0}\right),\, \text{where}\quad\sigma^2_{\hat{\beta}_0} = \frac{1}{n}\frac{\var\left(H_i u_i\right)}{\left(\E(H_i^2)\right)^2}\,\,\text{and}\,\, H_i = 1 - \frac{\mu_X}{\E(X_i^2)}X_i. \end{align*} \]

We can estimate the variance terms by replacing the unknown terms in \(\sigma^2_{\hat{\beta}_1}\) and \(\sigma^2_{\hat{\beta}_0}\) by their sample counterparts: \[ \begin{align} &\hat{\sigma}^2_{\hat{\beta}_1} = \frac{1}{n}\frac{\frac{1}{n-2}\sum_{i=1}^n(X_i - \bar{X})^2\hat{u}_i^2}{\left(\frac{1}{n}\sum_{i=1}^n(X_i - \bar{X})^2\right)^2},\\ &\hat{\sigma}^2_{\hat{\beta}_0} = \frac{1}{n}\frac{\frac{1}{n-2}\sum_{i=1}^n\hat{H}^2\hat{u}_i^2}{\left(\frac{1}{n}\sum_{i=1}^n\hat{H}_i^2\right)^2}\quad\text{and}\quad \hat{H}_i = 1 - \frac{\bar{X}}{\frac{1}{n}\sum_{i=1}^nX_i^2}X_i. \end{align} \]

Then, \(\SE(\hat{\beta}_{1})\) in Equation 14.1 can be computed by \(\SE(\hat{\beta}_{1})=\sqrt{\hat{\sigma}^2_{\hat{\beta}_1}}\). Also, when the sample size is large, the central limit theorem ensures that \[ \begin{align} \hat{\beta}_1 \stackrel{A}{\sim} N\left(\beta_1, \sigma^2_{\hat{\beta}_1}\right) \implies \frac{\hat{\beta}_1 - \beta_1}{\sigma_{\hat{\beta}_1}}\stackrel{A}{\sim} N(0,1). \end{align} \]

Thus, if \(H_0\) is true, then the sampling distribution of the \(t\)-statistic in Equation 14.1 can be approximated by \(N(0,1)\) in large samples, i.e., \[ t\stackrel{A}{\sim} N(0,1). \]

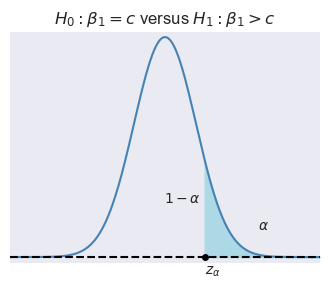

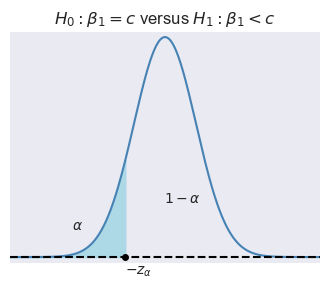

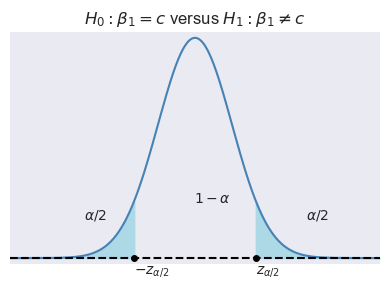

Let \(\alpha\) be the significance level, i.e., the probability of Type-I error. We can use the asymptotic distribution of \(t\), \(\alpha\) and the type of the alternative hypothesis to determine the critical values. In Figure 14.1, depending on the type of alternative hypothesis, we determine the critical values as \(z_{\alpha}\), \(-z_{\alpha}\), \(z_{\alpha/2}\), and \(-z_{\alpha/2}\). These values suggest the following rejection regions:

- \(\{z:z>z_{\alpha}\}\) when \(H_1:\beta_1>c\),

- \(\{z:z<-z_{\alpha}\}\) when \(H_1:\beta_1<c\), and

- \(\{z:|z|>z_{\alpha/2}\}\) when \(H_1:\beta_1\ne c\).

If the realized value of \(t\) falls within a rejection region, then we reject the null hypothesis at the \(\alpha\%\) significance level; otherwise, we fail to reject the null hypothesis.

Example 14.1 Assume that \(\alpha=5\%\) and \(H_1:\beta_1\ne c\). Then, the critical value on the left tail is the \(2.5\)th percentile of \(N(0,1)\), which is \(-z_{\alpha/2}=-1.96\), and the critical value on the right tail is the \(97.5\)th percentile of \(N(0,1)\), which is \(z_{\alpha/2}=1.96\). In R, we can compute these critical values as follows:

Alternatively, we can compute the \(p\)-value to decide between \(H_0\) and \(H_1\). The \(p\)-value is the probability of obtaining a test statistic value that is more extreme than the actual one when \(H_0\) is correct. Let \(t_{\text{calc}}\) be the realized value of the \(t\)-statistic from Equation 14.1. Then, depending on the type of alternative hypothesis, we can determine the \(p\)-value as \[ \begin{align} \text{$p$-value}= \begin{cases} P_{H_0}\left(t > |t_{\text{calc}}|\right)=1-\Phi(|t_{\text{calc}}|)\,\,\text{for}\,\,H_1:\beta_1>c,\\ P_{H_0}\left(t <-|t_{\text{calc}}|\right)=\Phi(-|t_{\text{calc}}|)\,\,\text{for}\,\,H_1:\beta_1<c,\\ P_{H_0}\left(|t| > |t_{\text{calc}}|\right)=2\times\Phi(-|t_{\text{calc}}|)\,\,\text{for}\,H_1:\beta_1\ne c. \end{cases} \end{align} \]

We reject \(H_0\) at the \(\alpha\%\) significance level if the \(p\)-value is less than \(\alpha\); otherwise, we fail to reject \(H_0\).

Example 14.2 Assume that \(\alpha=0.05\) and the realized value of the \(t\)-statistic is \(t_{\text{calc}}=-2.5\). Then, the \(p\)-value for the two-sided alternative hypothesis is \[ \begin{align} \text{$p$-value} = 2\times\Phi(-|-2.5|) = 2\times\Phi(-2.5). \end{align} \]

We can compute the \(p\)-value in R as follows:

p-value: 0.0124Since \(p\text{-value} < 0.05\), we reject \(H_0\) at the \(5\%\) significance level.

14.2 Application to the test score example

We use the data set contained in the caschool.xlsx file to estimate the following model: \[

\begin{align}

\text{TestScore}_i = \beta_0 + \beta_1 \text{STR}_i + u_i,

\end{align}

\]

In the data set, the test scores are denoted by testscr and the student-teacher ratio by str.

# Import data

CAschool = read_excel("data/caschool.xlsx")

# Column names

colnames(CAschool) [1] "Observation Number" "dist_cod" "county"

[4] "district" "gr_span" "enrl_tot"

[7] "teachers" "calw_pct" "meal_pct"

[10] "computer" "testscr" "comp_stu"

[13] "expn_stu" "str" "avginc"

[16] "el_pct" "read_scr" "math_scr" Consider \(H_0: \beta_1 = 0\) against \(H_1: \beta_1 \neq 0\). We use the lm function to estimate the model.

Call:

lm(formula = testscr ~ str, data = CAschool)

Residuals:

Min 1Q Median 3Q Max

-47.727 -14.251 0.483 12.822 48.540

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 698.9330 9.4675 73.825 < 2e-16 ***

str -2.2798 0.4798 -4.751 2.78e-06 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 18.58 on 418 degrees of freedom

Multiple R-squared: 0.05124, Adjusted R-squared: 0.04897

F-statistic: 22.58 on 1 and 418 DF, p-value: 2.783e-06Using the estimation results, we can compute \(t\)-statistic as \[ \begin{align} t = \frac{\hat{\beta}_1-0}{SE(\hat{\beta}_1)} \approx \frac{-2.28}{0.48} \approx -4.75 \end{align} \]

Note that the summary function also returns the \(t\)-statistics. The column named t value in the output includes the \(t\)-statistics. Also note that we can return \(t\)-statistics through result1$coefficients:

# t-statistics

result1$coefficients[, "t value"](Intercept) str

73.824514 -4.751327 Assume that the significance level is \(\alpha = 0.05\). Then, the corresponding critical value can be determined in the following way.

[1] 1.96Since \(|t| = |-4.75| = 4.75 > 1.96\), we reject \(H_0\) at the \(5\%\) significance level. Thus, the estimated effect of class size on test scores is statistically significant at the \(5\%\) significance level.

The \(p\)-value for the two-sided alternative hypothesis is \[ \begin{align} \text{p-value} = \text{Pr}_{H_0}\left(|t| > |t_{\text{calc}}|\right) = 2 \times \Phi(-|t_{\text{calc}}|), \end{align} \]

where \(t_{\text{calc}}\) is the actual \(t\)-statistic computed, which is \(t\approx -4.75\). Then, we can compute the \(p\)-value in the following way:

[1] 2.020858e-06Alternatively, we can extract \(p\)-values from result1$coefficients:

# p-values

result1$coefficients[, "Pr(>|t|)"] (Intercept) str

6.569925e-242 2.783307e-06 Note that this value is slightly different from the one that we computed above by 2 * pnorm(-abs(t), mean = 0, sd = 1). By default, the lm function uses the \(t\) distribution for the computation. Thus, we need to use the t distribution to get the same result:

[1] 2.783307e-06Again, since \(p\text{-value} < 0.05\), we reject \(H_0\) at the \(5\%\) significance level.

14.3 Confidence intervals for a regression parameter

Recall that the \(95\%\) two-sided confidence interval can be equivalently defined in the following ways:

- It is the set of points that cannot be rejected in a two-sided hypothesis testing problem with the \(5\%\) significance level.

- It is a set-valued function of the data (an interval that is a function of the data) that contains the true parameter value \(95\%\) of the time in repeated samples.

Then, the \(95\%\) two-sided confidence interval for \(\beta_1\) refers to the set of values for \(\beta_1\) such that \(P\left(\left\{\beta_1:\left|\frac{\hat{\beta}_1-\beta_1}{SE(\hat{\beta}_1)}\right|\le 1.96\right\}\right) = 0.95\). We can express the set \(\left\{\beta_1:\left|\frac{\hat{\beta}_1-\beta_1}{SE(\hat{\beta}_1)}\right|\le 1.96\right\}\) in a more convenient way: \[ \begin{align*} &\left\{\beta_1:\left|\frac{\hat{\beta}_1-\beta_1}{\SE(\hat{\beta}_1)}\right|\le 1.96\right\}=\left\{\beta_1:-1.96\le \frac{\hat{\beta}_1-\beta_1}{\SE(\hat{\beta}_1)}\le 1.96\right\}\\ &=\left\{\beta_1:-\hat{\beta}_1-1.96\, \SE(\hat{\beta}_1)\le -\beta_1\le -\hat{\beta}_1+1.96\, \SE(\hat{\beta}_1)\right\}\\ &=\left\{\beta_1:\hat{\beta}_1 + 1.96 \, \SE(\hat{\beta}_1)\ge \beta_1\ge \hat{\beta}_1 -1.96\, \SE(\hat{\beta}_1)\right\}\\ &=\left\{\beta_1:\hat{\beta}_1 - 1.96 \, \SE(\hat{\beta}_1)\le \beta_1\le \hat{\beta}_1 +1.96\, \SE(\hat{\beta}_1)\right\}. \end{align*} \]

In our test score example, the \(95\%\) confidence interval is computed in the following way:

[1] -3.220249 -1.339367Alternatively, we can use the confint function to compute the confidence interval:

# Confidence interval

confint(model1, level = 0.95) 2.5 % 97.5 %

(Intercept) 680.32313 717.542779

str -3.22298 -1.336637Again note that these values are slightly different from the ones that we computed above by lower_bound and upper_bound. By default, the lm function uses the critical value from the \(t\) distribution for the computation. Finally, note that the \(95\%\) two-sided confidence interval does not include the hypothesized value in \(H_0:\beta_1=0\), and therefore, we reject \(H_0\) at the \(5\%\) significance level.

14.4 Regression when \(X\) is a binary variable

In this section, we consider the following regression model: \[ \begin{align} Y_i &= \beta_0 + \beta_1 D_i + u_i, \quad i = 1,2,\dots,n, \end{align} \]

where \(D_i\) is a dummy variable defined as \[ \begin{align*} D_i &= \left\{\begin{array}{ll} 1, &\text{STR}_i < 20,\\ 0, &\text{STR}_i \geq 20. \end{array}\right. \end{align*} \]

Under the least squares assumptions, if the student-teacher ratio is high, i.e., \(D_i = 0\), then \(\E(Y_i|D_i = 0) = \beta_0\). However, if the student-teacher ratio is low, i.e., \(D_i = 1\), then \(\E(Y_i|D_i = 1) = \beta_0 + \beta_1\). Hence, \[ \begin{align*} \E(Y_i|D_i = 1) - \E(Y_i|D_i = 0) &= \beta_0 + \beta_1 - \beta_0 = \beta_1. \end{align*} \]

That is, \(\beta_1\) gives the difference between the mean test score in districts with low student-teacher ratios and the mean test score in districts with high student-teacher ratios.

The dummy variable can be created by using a logical operator. The command mydata$str < 20 will return \(1\) if \(STR < 20\), otherwise \(0\).

# A tibble: 6 × 3

testscr str D

<dbl> <dbl> <lgl>

1 691. 17.9 TRUE

2 661. 21.5 FALSE

3 644. 18.7 TRUE

4 648. 17.4 TRUE

5 641. 18.7 TRUE

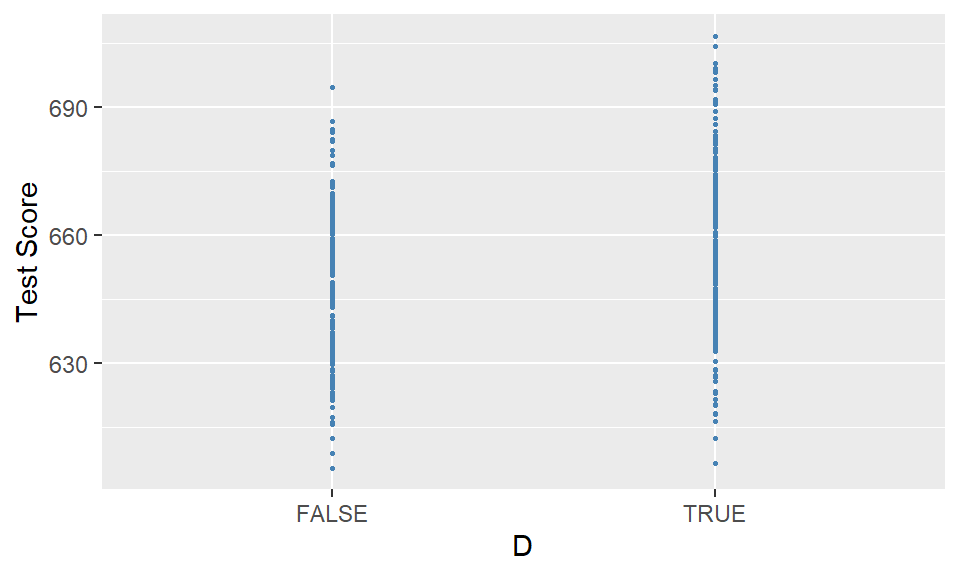

6 606. 21.4 FALSEFigure 14.2 shows the scatter plot of TestScore and D. Since D takes only two values, namely \(0\) and \(1\), we observe that the data points are clustered at x=0 and x=1.

# Scatterplot without jitter

ggplot(CAschool, aes(x = D, y = testscr)) +

geom_point(color = "steelblue", size = 0.5) +

labs(x = "D", y = "Test Score")

In Figure 14.3, we create a jittered version of D by adding some random noise: jittered_D = CAschool['D'] + np.random.normal(0, 0.02, size=len(CAschool['D'])), and construct a scatter plot between TestScore and jittered_D.

# Scatterplot with jitter

ggplot(CAschool, aes(x = D, y = testscr)) +

geom_jitter(

width = 0.02, # jitter scale (matches np.random.normal(0, 0.02))

size = 1,

color = "steelblue"

) +

labs(x = "D", y = "Test Score")

As in the case of a continuous regressor, we can use the lm function to estimate a dummy variable regression model.

Call:

lm(formula = testscr ~ D, data = CAschool)

Residuals:

Min 1Q Median 3Q Max

-50.601 -14.047 -0.451 12.841 49.399

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 649.979 1.388 468.380 < 2e-16 ***

DTRUE 7.372 1.843 3.999 7.52e-05 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 18.72 on 418 degrees of freedom

Multiple R-squared: 0.03685, Adjusted R-squared: 0.03455

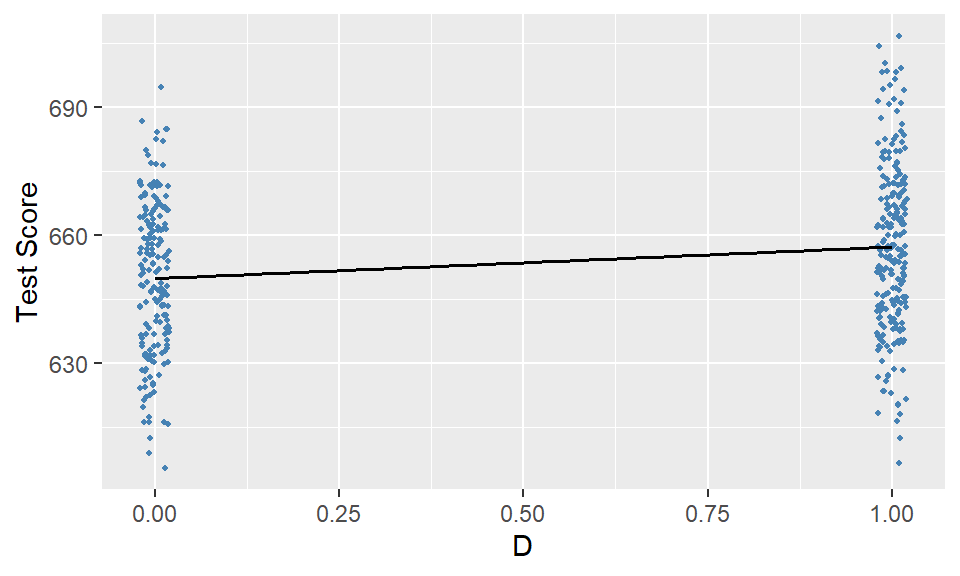

F-statistic: 15.99 on 1 and 418 DF, p-value: 7.515e-05The estimated regression function is \[ \begin{align} \widehat{\text{TestScore}}_i = 649.98 + 7.38 D_i. \end{align} \]

The estimate of \(\beta_1\) is \(7.38\), which indicates that students in the districts with STR < 20 have on average \(7.38\) more points than students in other districts.

Figure 14.4 shows the scatter plot along with the estimated regression function. Since \(\beta_1=7.38\), the estimated regression line is upward sloping, which indicates that the test scores are higher in districts with low student-teacher ratios.

# Dummy variable regression plot

ggplot(CAschool, aes(x = as.numeric(D), y = testscr)) +

geom_jitter(width = 0.02, size = 0.8, color = "steelblue") +

geom_smooth(method = "lm", se = FALSE, color = "black", linewidth = 0.6) +

labs(

x = "D",

y = "Test Score"

)

14.5 Heteroskedasticity versus Homoskedasticity

In the least squares assumptions introduced in Chapter 13, we only assume the zero-conditional mean assumption about the error terms. Other than this assumption, we do not impose any structure on the error term \(u_i\). In this section, we introduce two concepts about the conditional variance of the error term \(u_i\) given \(X_i\): homoskedasticity and heteroskedasticity. We say that the error term \(u_i\) is homoskedastic if the variance of \(u_i\) given \(X_i\) is constant for all \(i = 1,2,\dots,n\). In particular, this means that the variance does not depend on \(X_i\). On the other hand, if the variance does depend on \(X_i\), we say that the error term \(u_i\) is heteroskedastic.

Homoskedasticity and heteroskedasticity do not affect the unbiasedness and consistency of the OLS estimators of \(\beta_0\) and \(\beta_1\). However, they do affect the variance formulas of the OLS estimators as shown in Chapter 13. Under homoskedasticity, let \(\var(u_i|X_i)=\sigma^2_u\), where \(\sigma^2_u\) is an unknown scalar parameter. Then, the variance formulas of \(\hat{\beta}_1\) and \(\hat{\beta}_0\) simplify to \[ \begin{align*} &\sigma^2_{\widehat{\beta}_1} = \frac{1}{n}\frac{\var\left((X_i - \mu_X)u_i\right)}{\left(\var(X_i)\right)^2} = \frac{\sigma^2_u}{n\var(X_i)},\\ &\sigma^2_{\hat{\beta}_0} = \frac{1}{n}\frac{\var\left(H_i u_i\right)}{\left(\E(H_i^2)\right)^2} = \frac{\E(X^2_i)\sigma^2_u}{n\sigma^2_X}. \end{align*} \]

These variances are called the homoskedasticity-only variances. They can be estimated as \[ \begin{align*} &\hat{\sigma}^2_{\hat{\beta}_1} = \frac{\frac{1}{n-2}\sum_{i=1}^n \hat{u}_i^2}{\sum_{i=1}^n(X_i - \bar{X})^2},\\ &\hat{\sigma}^2_{\hat{\beta}_0}=\frac{\left(\frac{1}{n}\sum_{i=1}^nX^2_i\right)\left(\frac{1}{n-2}\sum_{i=1}^n \hat{u}_i^2\right)}{\frac{1}{n}\sum_{i=1}^n(X_i - \bar{X})^2}. \end{align*} \]

The lm function uses these formulas to compute the standard errors, i.e., it only reports the homoskedasticity-only standard errors. To get heteroskedasticity-robust standard errors, we use the vcovHC function from the sandwich package.

In the following, we use the modelsummary function to present results side by side. Note that we use the vcov = list(NULL, robust_se) option to specify the standard errors for each model. Alternatively, we can also use vcov=c("classical", "HC1") to obtain the same result. Note that in this alternative approach, we do not need to compute the robust standard errors manually through the vcovHC function. The estimation results are presented in Table 14.1. The estimation results in this table indicate that the heteroskedasticity-robust standard errors are relatively large.

modelsummary(

list(

"Homoskedastic" = result3,

"Heteroskedastic" = result3

),

vcov = list(NULL, robust_se),

stars = TRUE

)| Homoskedastic | Heteroskedastic | |

|---|---|---|

| (Intercept) | 698.933*** | 698.933*** |

| (9.467) | (10.364) | |

| str | -2.280*** | -2.280*** |

| (0.480) | (0.519) | |

| Num.Obs. | 420 | 420 |

| R2 | 0.051 | 0.051 |

| R2 Adj. | 0.049 | 0.049 |

| AIC | 3650.5 | 3650.5 |

| BIC | 3662.6 | 3662.6 |

| Log.Lik. | -1822.250 | -1822.250 |

| F | 22.575 | |

| RMSE | 18.54 | 18.54 |

| Std.Errors | Custom | |

| + p < 0.1, * p < 0.05, ** p < 0.01, *** p < 0.001 | ||

In practice, which standard errors should we use? Stock and Watson (2020) write that “At a general level, economic theory rarely gives any reason to believe that the errors are homoskedastic. It therefore is prudent to assume that the errors might be heteroskedastic unless you have compelling reasons to believe otherwise.” Therefore, we recommend using heteroskedasticity-robust standard errors in practice.

14.6 The theoretical foundation of the ordinary least squares method

In this section, we consider the OLS estimator of \(\beta_1\) under the following assumptions.

Under these extended assumptions, the following theorem justifies the use of the OLS method.

Theorem 14.1 (The Gauss-Markov Theorem for \(\hat{\beta}_1\)) Under Gauss–Markov Assumption, the OLS estimator of \(\beta_1\) is the best (most efficient) linear conditionally unbiased estimator (BLUE).

The proof of this theorem is given in Stock and Watson (2020). The Gauss-Markov theorem states that the OLS estimator \(\hat{\beta}_1\) has the smallest conditional variance among all conditionally unbiased estimators that are linear functions of \(Y_1,\dots,Y_n\). There are two limitations to this theorem. First, it requires the strong assumption that error terms are homoskedastic, which mostly does not hold in empirical applications. Second, there exist conditionally biased and non-linear estimators that are more efficient than the OLS estimator. We discuss such estimators in Chapter 23.

In the next chapter, we introduce the multiple linear regression model. In Chapter 28, we extend the Gauss-Markov theorem to the multiple linear regression model.