# Load necessary packages

library(tidyverse)

library(readxl)

library(dynlm)

library(vars)

library(urca)

library(modelsummary)

library(tsDyn)

options("modelsummary_factory_default" = "gt")

library(gridExtra)

library(knitr)

library(haven)

library(fGarch)

library(rugarch)

library(forecast)

library(tseries)26 Additional Topics in Time Series Regression

26.1 Introduction

In this chapter, we consider some selected topics in time series analysis. We cover vector autoregression (VAR), multi-period forecasting, cointegration and error correction models, volatility clustering, and autoregressive conditional heteroskedasticity models.

26.2 Vector Autoregressions

26.2.1 VAR models

VARs are introduced by Sims (1980). A VAR model is a generalization of the univariate ADL model to multiple time series. The VAR model for \(k\) variables is a set of \(k\) ADL models that are estimated simultaneously. If the number of lags is \(p\) in each equation in the VAR model, the model is called a VAR(\(p\)) model. For example, in the case of two variables \(Y_t\) and \(X_t\), the VAR(\(p\)) model is given by \[ \begin{align*} Y_t &= \beta_{10}+\beta_{11}Y_{t-1}+\beta_{12}Y_{t-2}+\cdots+\beta_{1p}Y_{t-p}+\gamma_{11}X_{t-1}+\cdots+\gamma_{1p}X_{t-p}+u_{1t},\\ X_t &= \beta_{20}+\beta_{21}Y_{t-1}+\beta_{22}Y_{t-2}+\cdots+\beta_{2p}Y_{t-p}+\gamma_{21}X_{t-1}+\cdots+\gamma_{2p}X_{t-p}+u_{2t}, \end{align*} \tag{26.1}\] where \(\beta\)’s and \(\gamma\)’s are unknown parameters, and \(u_{1t}\) and \(u_{2t}\) are the error terms.

Using matrix notation, we can express the two-variable VAR(\(p\)) as \[ \begin{align*} & \begin{pmatrix} Y_t\\ X_t \end{pmatrix} = \begin{pmatrix} \beta_{10}\\ \beta_{20} \end{pmatrix} + \begin{pmatrix} \beta_{11}&\gamma_{11}\\ \beta_{21}&\gamma_{21} \end{pmatrix} \times \begin{pmatrix} Y_{t-1}\\ X_{t-1} \end{pmatrix} +\ldots+ \begin{pmatrix} \beta_{1p}&\gamma_{1p}\\ \beta_{2p}&\gamma_{2p} \end{pmatrix} \times \begin{pmatrix} Y_{t-p}\\ X_{t-p} \end{pmatrix} + \begin{pmatrix} u_{1t}\\ u_{2t} \end{pmatrix}. \end{align*} \]

Then, we can express the model with the following compact form: \[ \begin{align} \bs{Y}_t=\bs{b}_0+\bs{B}_1\bs{Y}_{t-1}+\ldots+\bs{B}_{p}\bs{Y}_{t-p}+\bs{u}_t, \end{align} \tag{26.2}\] where \[ \begin{align*} \bs{Y}_t= \begin{pmatrix} Y_t\\ X_t \end{pmatrix},\, \bs{b}_0= \begin{pmatrix} \beta_{10}\\ \beta_{20} \end{pmatrix},\, \bs{B}_j= \begin{pmatrix} \beta_{1j}&\gamma_{1j}\\ \beta_{2j}&\gamma_{2j} \end{pmatrix},\,\text{and}\, \bs{u}_t= \begin{pmatrix} u_{1t}\\ u_{2t} \end{pmatrix}, \end{align*} \] for \(j=1,2,\ldots,p\).

The VAR(\(p\)) in Equation 26.2 is referred to as the reduced-form or standard-form VAR(\(p\)). There is nothing specific to the two-variable case. The model can be generalized to \(k\) variables by replacing the \(2\times1\) vector \(\bs{Y}_t\) with a \(k\times1\) vector \(\bs{Y}_t=(Y_{1t},\ldots,Y_{kt})'\) and adjusting the dimensions of \(\bs{b}_0\), \(\bs{B}_j\), and \(\bs{u}_t\) accordingly.

We can use the OLS estimator to estimate each equation in a VAR model. The assumptions required for estimating the VAR model are the same as those outlined in Section 24.9 for the ADL model. In particular, each variable in the model must be stationary. In large samples, the OLS estimator is consistent and asymptotically normal. Consequently, inference can be conducted as in a multiple regression model.

26.2.2 Granger causality

The structure of the VAR model reveals how a variable or a group of variables can help predict or forecast others. The following intuitive notion of prediction ability is due to Granger (1969) and Sims (1972).

Definition 26.1 (Granger Causality) If \(Y_t\) improves the prediction of \(X_t\), then \(Y_t\) is said to Granger-cause \(X_t\); otherwise, it is said to fail to Granger-cause \(X_t\).

We note that this notion of Granger causality does not correspond to the concept of causality defined in Chapter 22. Instead, it only reflects the predictive ability of variables. In our two-variable VAR model, we can test for whether \(Y_t\) Granger causes \(X_t\) by formulating the following null and alternative hypotheses: \[ \begin{align*} &H_0:\beta_{21}=\beta_{22}=\ldots=\beta_{2p}=0,\\ &H_1:\text{At least one parameter is not zero}. \end{align*} \] We can resort to the \(F\)-statistic to test the null hypothesis.

26.2.3 Model formulation

When formulating a VAR model, we usually face the following issues:

- How many variables should be included in the model?

- What is the appropriate number of lags to include in the model?

- Which variables should be included in the model?

Although the modeling process depends on the specific research question and available data, Stock and Watson (2020) provide a general guideline for formulating a VAR model. For the first and second questions, we need to note that the number of parameters to estimate increases with both the number of VAR variables and the number of lags. For example, in a VAR(\(2\)) model with two variables, there are 10 parameters to estimate, whereas in a VAR(\(2\)) model with three variables, this number increases to 18. If the sample size is small and the number of parameters is large, the OLS estimator may not accurately estimate all parameters. Therefore, when using the OLS estimator, the number of VAR variables should be kept small so that the number of parameters remains relatively low compared to the sample size.

To determine the number of lags, we can use information criteria. Specifically, we consider the Bayesian Information Criterion (BIC) and the Akaike Information Criterion (AIC), which are defined as follows: \[ \begin{align} &\text{BIC}(p)=\ln\left(\text{det}(\hat{\Sigma}_u)\right)+k(kp+1)\ln(T)/T,\\ &\text{AIC}(p)=\ln\left(\text{det}(\hat{\Sigma}_u)\right)+2k(kp+1)/T, \end{align} \] where \(k\) is the number of VAR variables, \(\text{det}(\hat{\Sigma}_u)\) is the determinant of \(\hat{\Sigma}_u\), and \(\hat{\Sigma}_u\) is the estimated covariance matrix of the VAR error terms. The \((i,j)\)th element of \(\hat{\Sigma}_u\) is \(\frac{1}{T}\sum_{t=1}^T\hat{u}_{it}\hat{u}_{jt}\), where \(\hat{u}_{it}\) is the OLS residuals from the \(i\)th equation and \(\hat{u}_{jt}\) is the OLS residuals from the \(j\)th equation. We can then test a set of candidate values for \(p\) and choose the one that minimizes BIC(\(p\)) or AIC(\(p\)).

For the third question, we should use economic theory to select VAR variables that are related to each other so they can effectively predict and forecast one another. We can apply the Granger causality test and include variables that Granger-cause each other. Including variables that do not Granger-cause each other can introduce estimation errors, thereby reducing the model’s forecasting ability.

26.2.4 An empirical application: A VAR model for the GDP growth rate and the term spread

In this section, we consider a VAR(\(2\)) model for the GDP growth rate (GDPGR) and the term spread (TSpread) for the U.S. economy. The model takes the following form: \[

\begin{align*}

&\text{GDPGR}_t=\beta_{10}+\beta_{11}\text{GDPGR}_{t-1}+

\beta_{12}\text{GDPGR}_{t-2}+\gamma_{11}\text{TSpread}_{t-1}+\gamma_{12}\text{TSpread}_{t-2}+u_{1t},\\

&\text{TSpread}_t=\beta_{20}+\beta_{21}\text{GDPGR}_{t-1}+

\beta_{22}\text{GDPGR}_{t-2}+\gamma_{21}\text{TSpread}_{t-1}+\gamma_{22}\text{TSpread}_{t-2}+u_{2t}.

\end{align*}

\] The GDPGR variable is contained in the GrowthRate.csv file, and the TSpread variable is available in the TermSpread.csv file. The GrowthRate.csv file contains data on the following variables:

-

Y: Logarithm of real GDP -

YGROWTH: Annual real GDP growth rate -

RECESSION: Recession indicator (1 if recession, 0 otherwise)

# Load the GrowthRate data

dfGrowth <- read_excel("data/GrowthRate.xlsx")

# Convert to a quarterly time-series object starting in 1960 Q1

dfGrowth <- ts(dfGrowth, start = c(1960, 1), frequency = 4)

# Display column names

colnames(dfGrowth)[1] "Period" "Y" "YGROWTH" "RECESSION"The TermSpread.csv file includes data on the following variables:

-

GS10: Interest rate on 10-year US Treasury bonds -

TB3MS: Interest rate on 3-month Treasury bills -

RSPREAD: Term-spread (GS10-TB3MS) -

RECESSION: Dummy variable indicating recession periods

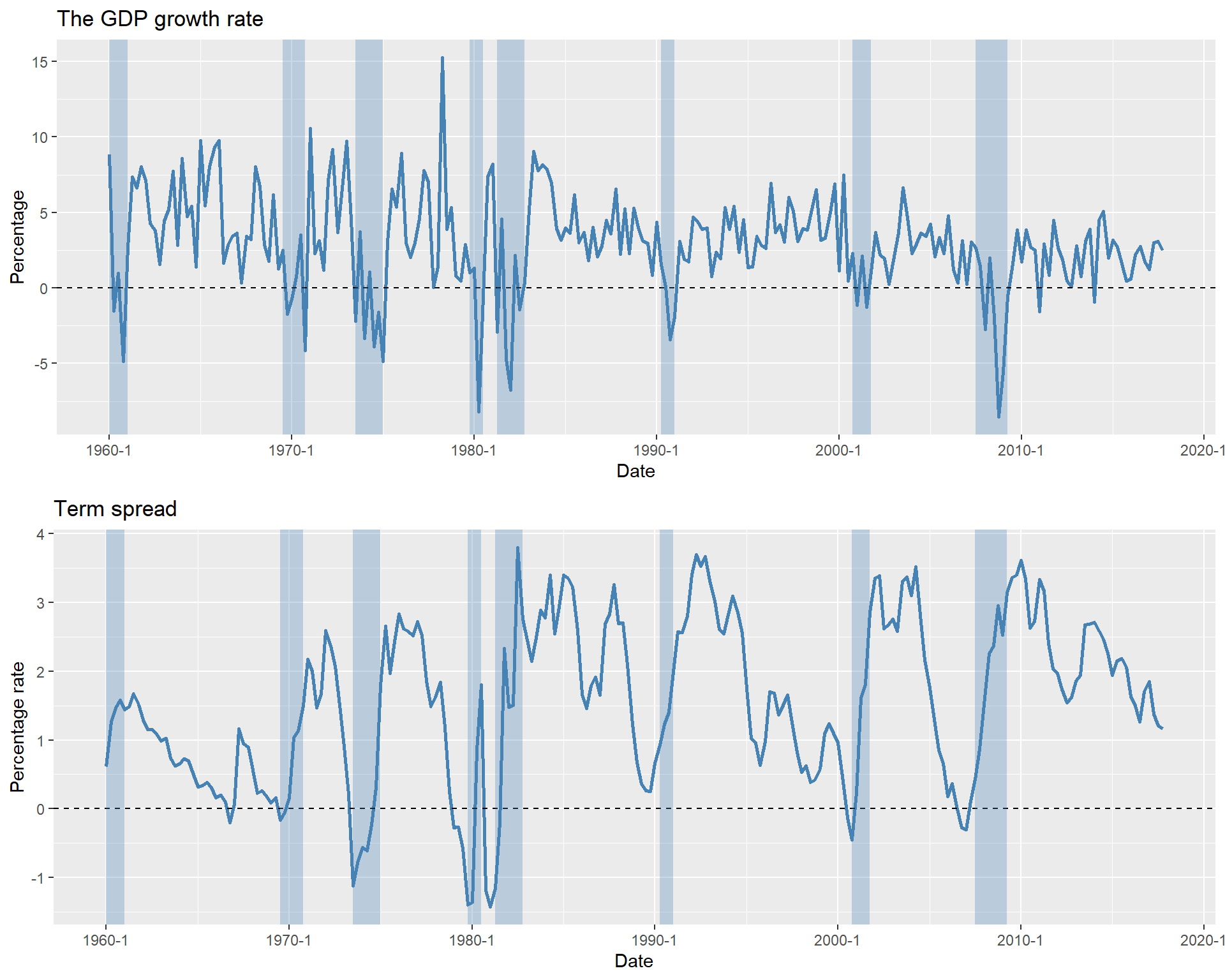

[1] "Period" "GS10" "TB3MS" "RSPREAD" "RECESSION"In the following, we merge the two datasets into a single dataset and plot the GDP growth rate and the term spread. The resulting plots are shown in Figure 26.1, with shaded areas indicating recession periods. The figure illustrates that the GDP growth rate fluctuates over time and is often negative during recessions. Similarly, the term spread varies over time and tends to be negative during recession periods.

# Convert ts object to data frame for ggplot

data_df <- data.frame(

Date = as.yearqtr(time(data)),

YGROWTH = as.numeric(data[, "YGROWTH"]),

RSPREAD = as.numeric(data[, "RSPREAD"]),

RECESSION_x = as.numeric(data[, "RECESSION_x"]),

RECESSION_y = as.numeric(data[, "RECESSION_y"])

)

# Plot GDP growth rate

p1 <- ggplot(data_df, aes(x = Date, y = YGROWTH)) +

geom_line(color = "steelblue", linewidth = 1) +

geom_hline(yintercept = 0, linetype = "dashed", color = "black") +

geom_rect(

data = subset(data_df, RECESSION_x == 1),

aes(xmin = Date - 0.125, xmax = Date + 0.125, ymin = -Inf, ymax = Inf),

fill = "steelblue", alpha = 0.3, inherit.aes = FALSE

) +

labs(title = "The GDP growth rate", x = "Date", y = "Percentage")

# Plot Term Spread

p2 <- ggplot(data_df, aes(x = Date, y = RSPREAD)) +

geom_line(color = "steelblue", linewidth = 1) +

geom_hline(yintercept = 0, linetype = "dashed", color = "black") +

geom_rect(

data = subset(data_df, RECESSION_y == 1),

aes(xmin = Date - 0.125, xmax = Date + 0.125, ymin = -Inf, ymax = Inf),

fill = "steelblue", alpha = 0.3, inherit.aes = FALSE

) +

labs(title = "Term spread", x = "Date", y = "Percentage rate")

# Arrange plots vertically

grid.arrange(p1, p2, ncol = 1)

Although our model is a VAR(\(2\)) model, we can check whether the information criteria return the same number of lags. In the following, we use the VARselect function from the vars package to select the number of lags. The results show that both the BIC (SC) and the AIC suggest two lags, which is consistent with our model specification.

$selection

AIC(n) HQ(n) SC(n) FPE(n)

2 2 2 2

$criteria

1 2 3 4

AIC(n) 0.1576071 0.03941016 0.09016937 0.08419334

HQ(n) 0.2081228 0.12360304 0.20803940 0.23574052

SC(n) 0.2819222 0.24660209 0.38023808 0.45713882

FPE(n) 1.1707205 1.04025637 1.09453104 1.08820171We then use the VAR function from the vars package to estimate the VAR(\(2\)) model. The estimation results are shown in Table 26.1. In the YGROWTH equation, all estimated coefficients are statistically significant at the 5% level, indicating that the GDP growth rate can be forecasted using its own lagged values and the lagged values of the term spread. In the RSPREAD equation, except for the first lag of YGROWTH, all other estimated coefficients are statistically significant at the 5% level.

# Fit the VAR model with lag = 2

var_model <- VAR(varData, p = 2, type = "const")# Display the summary of the VAR model

modelsummary(var_model$varresult,

fmt = 3,

stars = TRUE

)| YGROWTH | RSPREAD | |

|---|---|---|

| YGROWTH.l1 | 0.308*** | 0.010 |

| (0.077) | (0.016) | |

| RSPREAD.l1 | -0.770* | 1.033*** |

| (0.378) | (0.079) | |

| YGROWTH.l2 | 0.236** | -0.055*** |

| (0.075) | (0.016) | |

| RSPREAD.l2 | 1.068** | -0.199* |

| (0.368) | (0.077) | |

| const | 0.657 | 0.453*** |

| (0.438) | (0.092) | |

| Num.Obs. | 145 | 145 |

| R2 | 0.305 | 0.804 |

| R2 Adj. | 0.285 | 0.798 |

| AIC | 654.6 | 202.6 |

| BIC | 672.4 | 220.4 |

| Log.Lik. | -321.294 | -95.293 |

| RMSE | 2.22 | 0.47 |

| + p < 0.1, * p < 0.05, ** p < 0.01, *** p < 0.001 | ||

Although all information criteria suggest two lags, we can still use autocorrelation tests to check whether there is any remaining correlation in the error terms. To that end, we use the Ljung-Box test to check for serial correlation in the residuals. Since the p-values are greater than 0.05, we fail to reject the null hypothesis of no serial correlation in the residuals.

Box-Ljung test

data: res_y

X-squared = 0.74344, df = 4, p-value = 0.9459

Box-Ljung test

data: res_r

X-squared = 3.4924, df = 4, p-value = 0.479In the following, we use the serial.test function, which provides a portmanteau test for testing the overall significance of the residual autocorrelations up to the fourth lag. The results show that there is no serial correlation in the residuals.

# Overall test for residual autocorrelation up to lag 4

serial_test <- serial.test(var_model, lags.pt = 4, type = "PT.asymptotic")

# Display results

serial_test

Portmanteau Test (asymptotic)

data: Residuals of VAR object var_model

Chi-squared = 7.795, df = 8, p-value = 0.4537Thus, both Box.test and serial.test tests indicate that there is no serial correlation in the residuals, suggesting that two lags are sufficient to capture the dynamics of the GDP growth rate and the term spread.

Next, to determine whether TSpread Granger-causes GDPGR, we use the \(F\)-statistic for the following null and alternative hypotheses: \[

\begin{align}

&H_0: \gamma_{11}=\gamma_{12}=0,\\

&H_1:\,\,\text{At least one parameter is different from zero}.

\end{align}

\]

This test is conducted using the causality function from the vars package. Since the p-value is less than 0.05, we reject the null hypothesis and conclude that TSpread Granger-causes GDPGR.

# Granger causality test: Does RSPREAD Granger-cause YGROWTH?

gtest <- causality(var_model, cause = "RSPREAD")

# Display results

gtest$Granger

Granger causality H0: RSPREAD do not Granger-cause YGROWTH

data: VAR object var_model

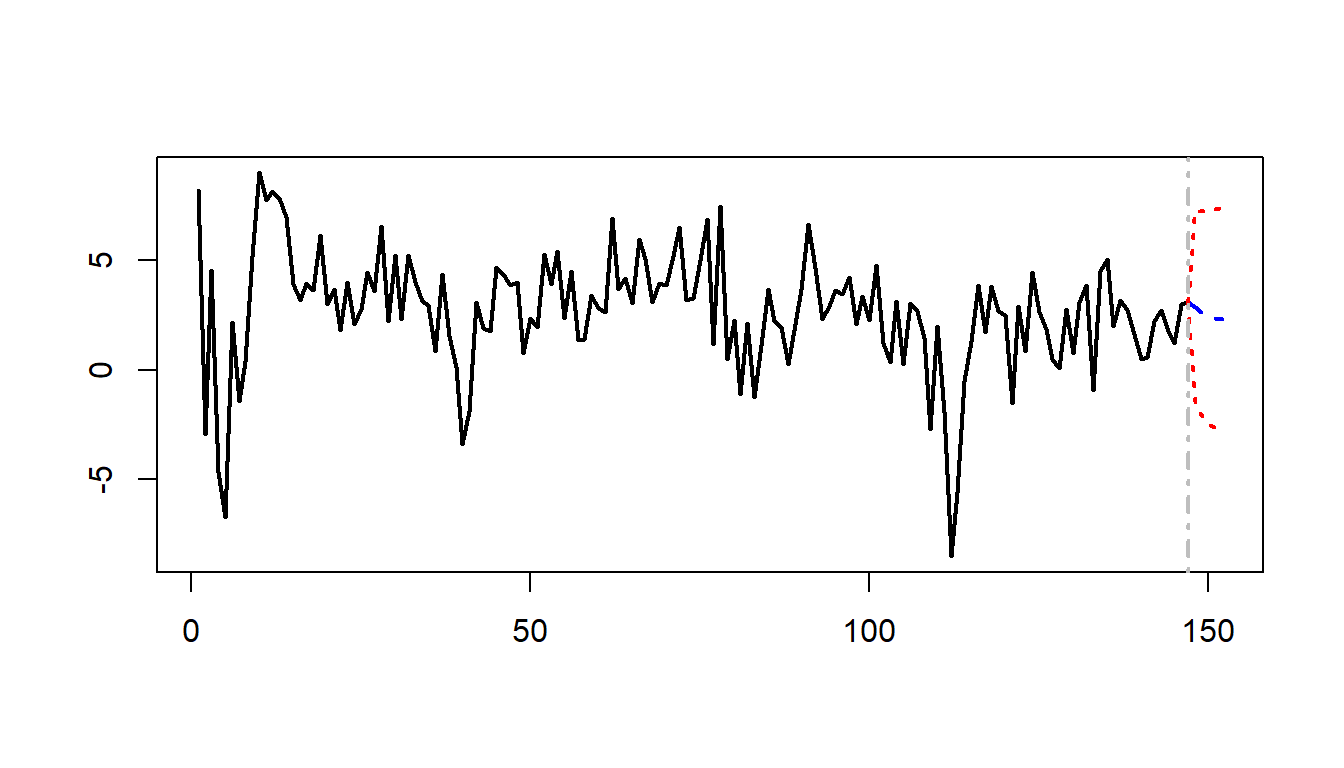

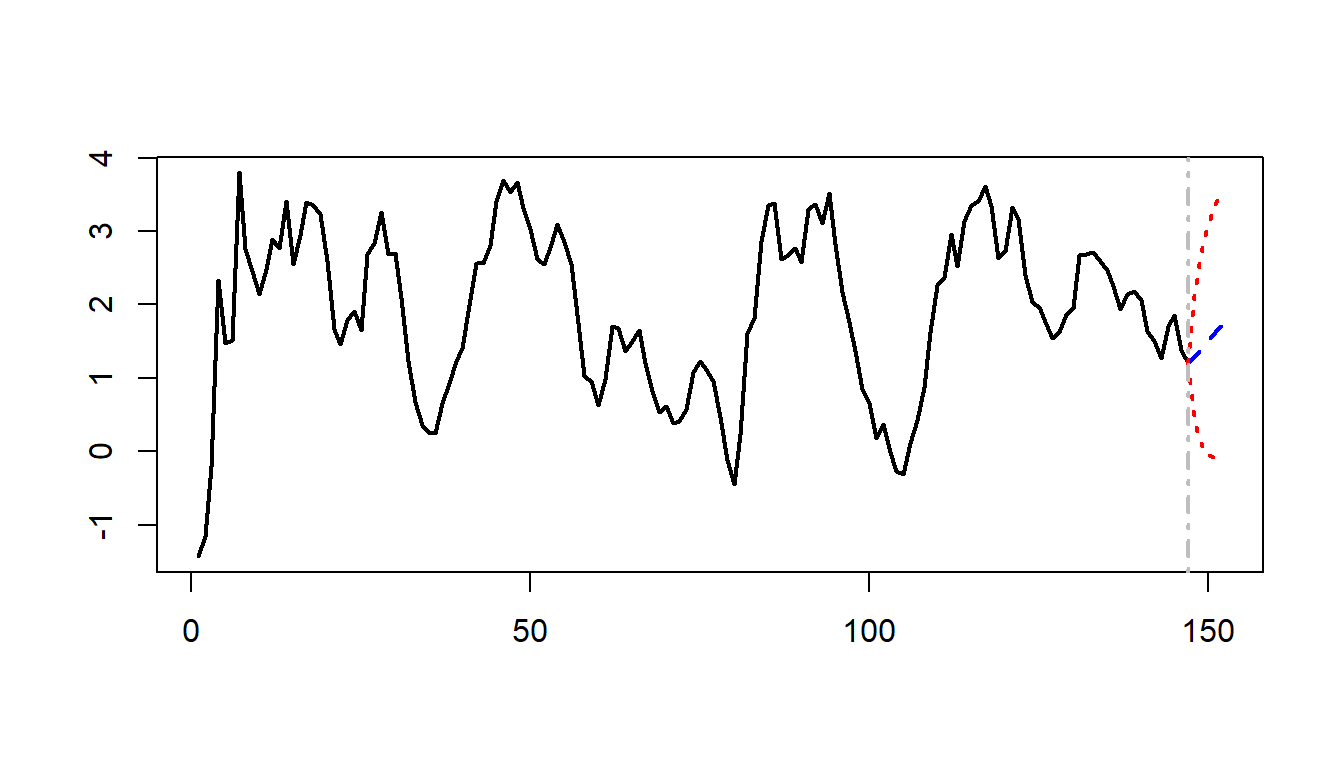

F-Test = 4.8842, df1 = 2, df2 = 280, p-value = 0.008222We can use the predict function with the option n.ahead = 5 to forecast the GDP growth rate and the term spread for the next 5 periods. The forecasted values are plotted in Figure 26.2.

# Forecast for the next 5 periods

# Produce 5-step-ahead forecasts

fc <- predict(var_model, n.ahead = 5)| fcst | lower | upper | CI | |

|---|---|---|---|---|

| 2017 Q4 | 2.865346 | -1.560028 | 7.290720 | 4.425374 |

| 2018 Q1 | 2.568107 | -2.108272 | 7.244487 | 4.676380 |

| 2018 Q2 | 2.423284 | -2.467971 | 7.314540 | 4.891255 |

| 2018 Q3 | 2.345198 | -2.646450 | 7.336846 | 4.991648 |

| 2018 Q4 | 2.323640 | -2.728332 | 7.375612 | 5.051972 |

| fcst | lower | upper | CI | |

|---|---|---|---|---|

| 2017 Q4 | 1.293331 | 0.36212181 | 2.224540 | 0.9312089 |

| 2018 Q1 | 1.408409 | 0.06743861 | 2.749380 | 1.3409705 |

| 2018 Q2 | 1.520251 | -0.04790366 | 3.088406 | 1.5681546 |

| 2018 Q3 | 1.627686 | -0.09431688 | 3.349688 | 1.7220025 |

| 2018 Q4 | 1.723549 | -0.10123707 | 3.548334 | 1.8247857 |

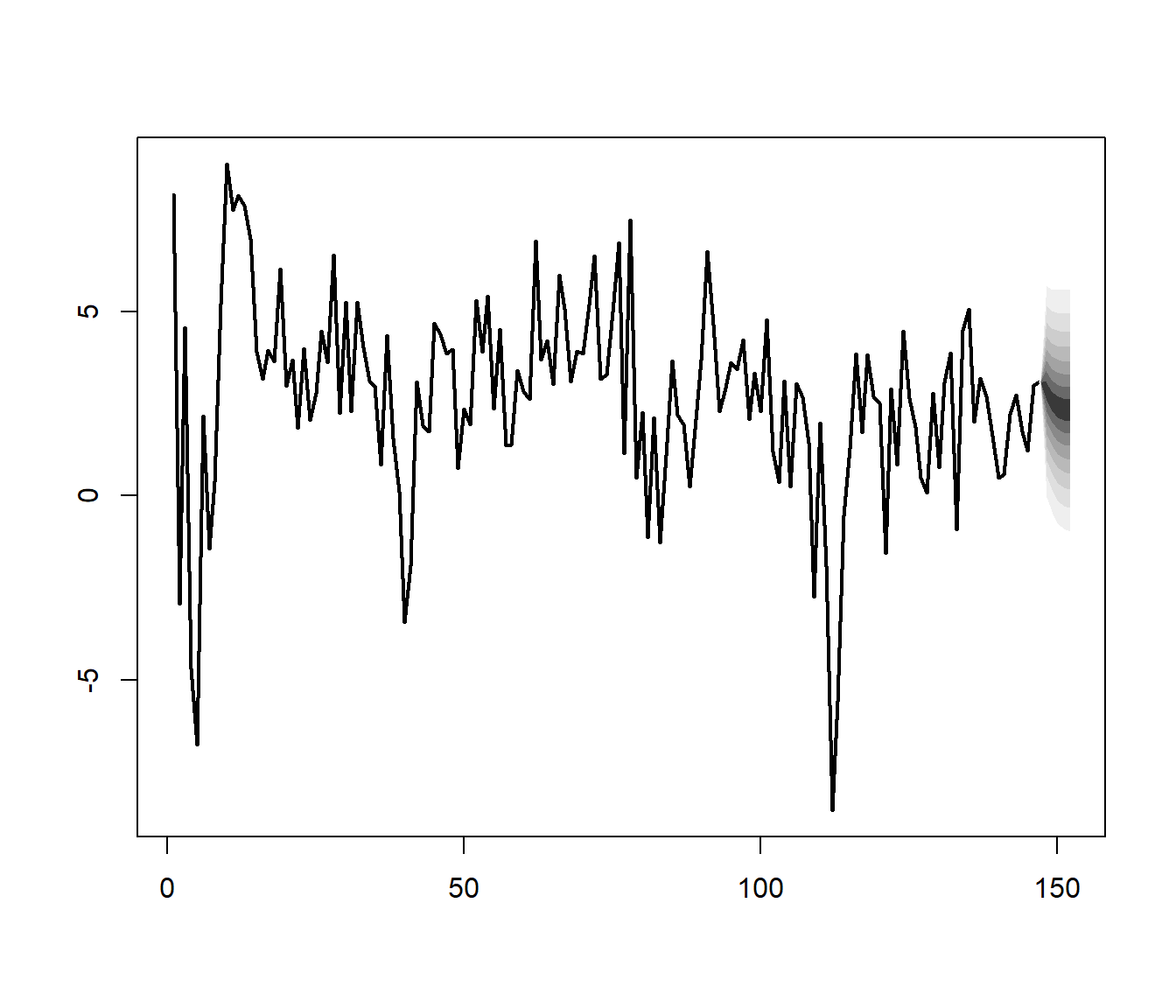

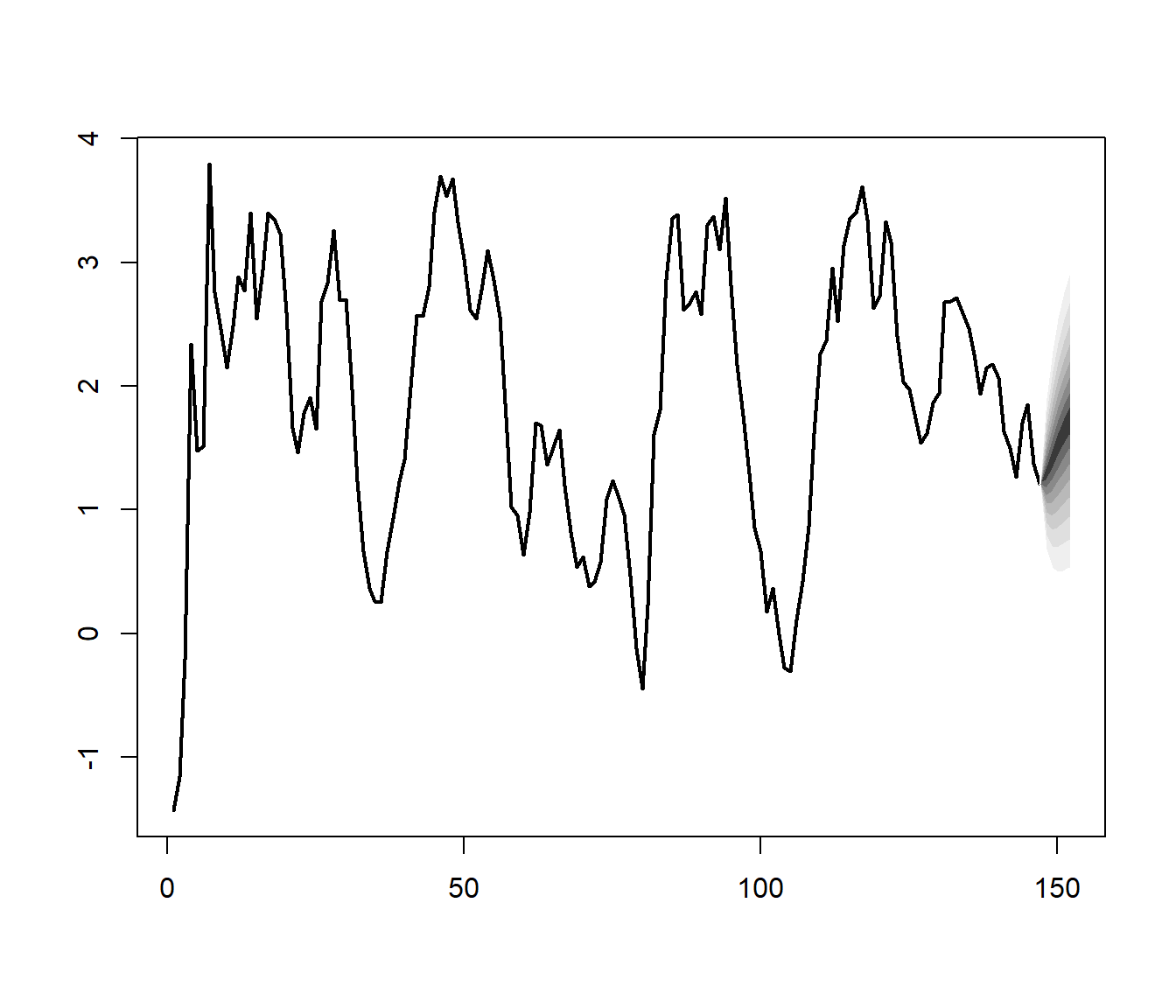

The fanchart function from the vars package can be used to present forecasts with differently shaded confidence regions. Figure 26.3 shows the fancharts.

26.2.5 Impulse Response Analysis

VAR models are often used to analyze the dynamic effects of a shock in one variable on the other variables in the system. This type of analysis is called impulse response analysis. For this analysis, we need to express our VAR(\(p\)) model in its moving average (MA) representation. To that end, we assume that the error term \(\bs{u}_t\) satisfies the following condition: \[ \begin{align*} \E\left(\bs{u}_t|\bs{Y}_{t-1}, \bs{Y}_{t-2}, \ldots\right) &= 0. \end{align*} \]

This assumption implies that (i) \(\E(\bs{u}_t)=0\), (ii) \(\E(\bs{u}_t\bs{u}^{'}_{t-k})=0\) for \(k\geq1\), and (iii) the VAR(\(p\)) model in Equation 26.2 is correctly specified so that the coefficient matrices beyond lag \(p\) are zero. In our analysis, we will further assume that \(\E(\bs{u}_t\bs{u}^{'}_{t})=\bs{\Sigma}\) for some positive definite matrix \(\bs{\Sigma}\).

The multivariate Wold decomposition theorem states that the VAR(\(p\)) model in Equation 26.2 can be expressed in the following MA representation (Lütkepohl (2005) and Hansen (2022)): \[ \begin{align*} \bs{Y}_t=\bs{\mu}+\sum_{j=0}^{\infty}\bs{\Psi}_j\bs{u}_{t-j}, \end{align*} \tag{26.3}\] where \(\bs{\mu}=(\bs{I}-\bs{B}_1-\ldots-\bs{B}_p)^{-1}\bs{b}_0\) is the mean of \(\bs{Y}_t\), and \(\bs{\Psi}_j\) is the \(k\times k\) matrix of coefficents for the \(j\)th lag of the error term \(\bs{u}_{t-j}\) in the MA representation. We can determine \(\bs{\Psi}_j\) recursively using the following formula: \[ \begin{align*} &\bs{\Psi}_0=\bs{I},\\ &\bs{\Psi}_j=\bs{B}_1\bs{\Psi}_{j-1}+\bs{B}_2\bs{\Psi}_{j-2}+\ldots+\bs{B}_p\bs{\Psi}_{j-p},\,\,\text{for}\,\,j\geq1, \end{align*} \tag{26.4}\] where \(\bs{I}\) is the \(k\times k\) identity matrix. Thus, once we estimate the coefficient matrices \(\bs{B}_1,\ldots,\bs{B}_p\), we can compute \(\bs{\Psi}_j\) for any \(j\geq0\).

Note that the MA representation in Equation 26.10 implies that \(\bs{Y}_t\) is a linear function of the current and past error terms. We can also determine \(h\)-period ahead value \(\bs{Y}_{t+h}\) as a linear function of the current and past error terms in the following way: \[ \begin{align*} \bs{Y}_{t+h}=\bs{\mu}+\sum_{j=0}^{h-1}\bs{\Psi}_j\bs{u}_{t+h-j}+\sum_{j=h}^{\infty}\bs{\Psi}_j\bs{u}_{t+h-j}. \end{align*} \] Let \(\mathcal{F}_t\) be the information set at time \(t\) that contains the current and past values of \(\bs{Y}_t\) and \(\bs{u}_t\). Then, we have \[ \begin{align*} \E\left(\bs{Y}_{t+h}|\mathcal{F}_t\right) = \bs{\mu}+\sum_{j=h}^{\infty}\bs{\Psi}_j\bs{u}_{t+h-j}. \end{align*} \]

Definition 26.2 (Impulse response function) The impulse response function (IRF) at horizon \(h\) is defined as the response of \(\E\left(\bs{Y}_{t+h}|\mathcal{F}_t\right)\) to a change in \(\bs{u}_t\): \[ \begin{align*} \text{IRF}(h) = \frac{\partial\E\left(\bs{Y}_{t+h}|\mathcal{F}_t\right)}{\partial \bs{u}^{'}_t} = \bs{\Psi}_h. \end{align*} \tag{26.5}\]

Note that \(\text{IRF}(h)\) is a \(k\times k\) matrix, and the \((i,j)\)th element, denoted by \(\text{IRF}_{ij}(h)\), is the response of the \(i\)th variable \(Y_{i,t+h}\) to a one-unit change in the \(j\)th error term \(u_{jt}\). Thus, we can use \(\text{IRF}_{ij}(h)\) to analyze the dynamic effect of a change in \(u_{jt}\) on the \(i\)th variable \(Y_{it}\) over time.

Using \(\text{IRF}(h)\), we can also define the cumulative impulse response function (CIRF) at horizon \(h\) as follows: \[ \begin{align*} \text{CIRF}(h) = \sum_{j=1}^h \text{IRF}(j) = \sum_{j=1}^h \bs{\Psi}_j, \end{align*} \] which gives the cumulative responses of \(\bs{Y}_{t}\) from time \(t\) to \(t+h\). The limit of \(\text{CIRF}(h)\) as \(h\to\infty\) is called the long-run cumulative impulse response function, which gives the long-run response of \(\bs{Y}_t\) to a change in \(\bs{u}_t\): \[ \begin{align*} \text{CIRF} = \lim_{h\to\infty} \sum_{j=1}^h \text{IRF}(j) = \sum_{j=1}^\infty \bs{\Psi}_j=(\bs{I}-\bs{B}_1-\ldots-\bs{B}_p)^{-1}. \end{align*} \]

The elements of \(\bs{u}_t\) are contemporaneously correlated. Therefore, \(\text{IRF}_{ij}(h)\), which measures the response of \(\E(Y_{i,t+h}|\mathcal{F}_t)\) to a change in \(u_{jt}\) while holding the other error terms fixed, may not be economically meaningful. A natural solution is to define the impulse response function in terms of uncorrelated (orthogonalized) shocks. To this end, we factor \(\bs{\Sigma}\) as \(\bs{\Sigma}=\bs{B}\bs{B}'\) for some nonsingular matrix \(\bs{B}\) and define \(\bs{\varepsilon}_t=\bs{B}^{-1}\bs{u}_t\). Note that \(\E(\bs{\varepsilon}_t)=0\) and \(\E(\bs{\varepsilon}_t\bs{\varepsilon}^{'}_t)=\bs{I}\), so the elements of \(\bs{\varepsilon}_t\) are uncorrelated.

Definition 26.3 (Orthogonalized shocks) We call \(\bs{\varepsilon}_t\) the vector of orthogonalized shocks and refer to its elements simply as shocks.

Unfortunately, the matrix \(\bs{B}\) is not unique. For example, if \(\bs{P}\) is any \(k\times k\) orthogonal matrix (i.e., \(\bs{P}\bs{P}'=\bs{P}'\bs{P}=\bs{I}\)), then \(\bs{\Sigma}=(\bs{B}\bs{P})(\bs{B}\bs{P})'\), showing that there are infinitely many ways to factor \(\bs{\Sigma}\). Sims (1980) suggests using the Cholesky decomposition of \(\bs{\Sigma}\): \(\bs{B}=\text{Cholesky}(\bs{\Sigma})\), which is a lower triangular matrix. When \(k=3\), the Cholesky decomposition of \(\bs{\Sigma}\) is given by \[ \begin{align*} \bs{B}= \begin{pmatrix} b_{11} & 0 & 0\\ b_{21} & b_{22} & 0\\ b_{31} & b_{32} & b_{33} \end{pmatrix}, \end{align*} \] with non-negative diagonal elements. Thus, we can express \(\bs{u}_t\) in terms of \(\bs{\varepsilon}_t\) as follows: \[ \begin{align*} &u_{1t}=b_{11}\varepsilon_{1t},\\ &u_{2t}=b_{21}\varepsilon_{1t}+b_{22}\varepsilon_{2t},\\ &u_{3t}=b_{31}\varepsilon_{1t}+b_{32}\varepsilon_{2t}+b_{33}\varepsilon_{3t}. \end{align*} \]

Therefore, the first shock \(\varepsilon_{1t}\) affects all three error components, the second shock \(\varepsilon_{2t}\) affects only the second and third components, and the third shock \(\varepsilon_{3t}\) affects only the third component. Thus, the Cholesky decomposition imposes a recursive structure on the contemporaneous relationships among the VAR variables. Specifically, the first variable in the system is affected only by its own shock, the second variable is affected by its own shock and the shock to the first variable, and so on. Therefore, the ordering of variables in the system matters when using the Cholesky decomposition to orthogonalize shocks.

Using \(\bs{\varepsilon}_t\), we can express the VAR(\(p\)) model in Equation 26.2 in the following MA representation: \[ \begin{align*} \bs{Y}_t=\bs{\mu}+\sum_{j=0}^{\infty}\bs{\Psi}_j\bs{B}\bs{\varepsilon}_{t-j}. \end{align*} \tag{26.6}\] We can then define the orthogonalized impulse response function (OIRF) at horizon \(h\) as follows: \[ \begin{align*} \text{OIRF}(h) = \frac{\partial\E\left(\bs{Y}_{t+h}|\mathcal{F}_t\right)}{\partial \bs{\varepsilon}^{'}_t} = \bs{\Psi}_h\bs{B}. \end{align*} \]

The discussion in this section suggests that we can formulate the orthogonalized impulse response function using the following steps:

- Estimate the reduced-form VAR(\(p\)) model in Equation 26.2 and obtain the OLS residuals \(\hat{\bs{u}}_t\).

- Compute the estimated covariance matrix of the residuals \(\hat{\bs{\Sigma}}=\frac{1}{T}\sum_{t=1}^T\hat{\bs{u}}_t\hat{\bs{u}}_{t}'\) and its Cholesky decomposition \(\hat{\bs{B}}\).

- Compute \(\hat{\bs{\Psi}}_j\) for \(j=0,\ldots, h\) using the recursive formula in Equation 26.4.

- Compute the estimated OIRF at horizon \(h\) as \(\widehat{\text{OIRF}}(h)=\hat{\bs{\Psi}}_h\hat{\bs{B}}\).

To compute the standard errors of \(\widehat{\text{OIRF}}(h)\), we can resort to the bootstrap method or the delta method. Because of the complexity of the OIRF estimator, the recursive bootstrap method is more commonly used in the literature. The recursive bootstrap method involves resampling the residuals \(\hat{\bs{u}}_t\) to generate new samples of \(\bs{Y}_t\), re-estimating the VAR model for each sample, and computing the OIRF for each sample. The standard errors of \(\widehat{\text{OIRF}}(h)\) can then be computed from the distribution of the OIRF estimates across the bootstrap samples (Hansen (2022)).

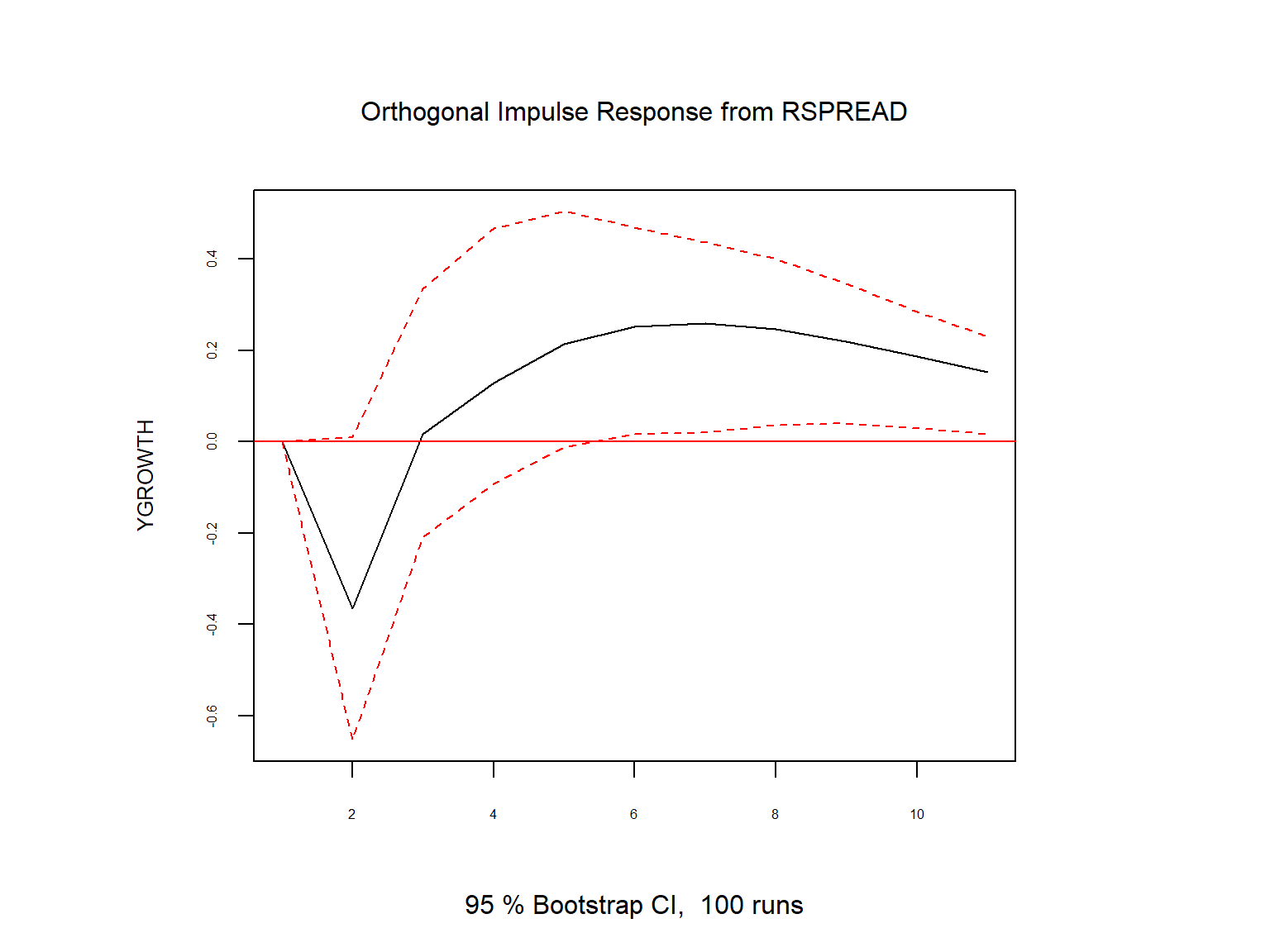

In our VAR(\(2\)) model for the GDP growth rate and the term spread, we use the OIRF to analyze the effect of a shock to the term spread on the GDP growth rate. We assume that a shock to the GDP growth rate contemporaneously affects both the GDP growth rate and the term spread, while a shock to the term spread contemporaneously affects only the term spread. This identification assumption is consistent with the Cholesky decomposition of \(\hat{\bs{\Sigma}}\) when GDPGR is ordered before TSpread in the VAR specification.

We use the irf function from the vars package to compute the OIRF. The resulting estimates are shown in Table 26.6. The table reports the point estimates of the OIRF and the cumulative OIRF, along with their confidence intervals. In Figure 26.4, we plot the estimated OIRF and cumulative OIRF. The OIRF plot shows that a shock to the term spread has a negative effect on GDP growth in the first quarter (a drop of about 0.3 percent). The effect then becomes positive in subsequent quarters, peaking at about 0.26 percent in the sixth quarter. However, all estimates are statistically insignificant at the 5% level, except for the first-quarter point estimate.

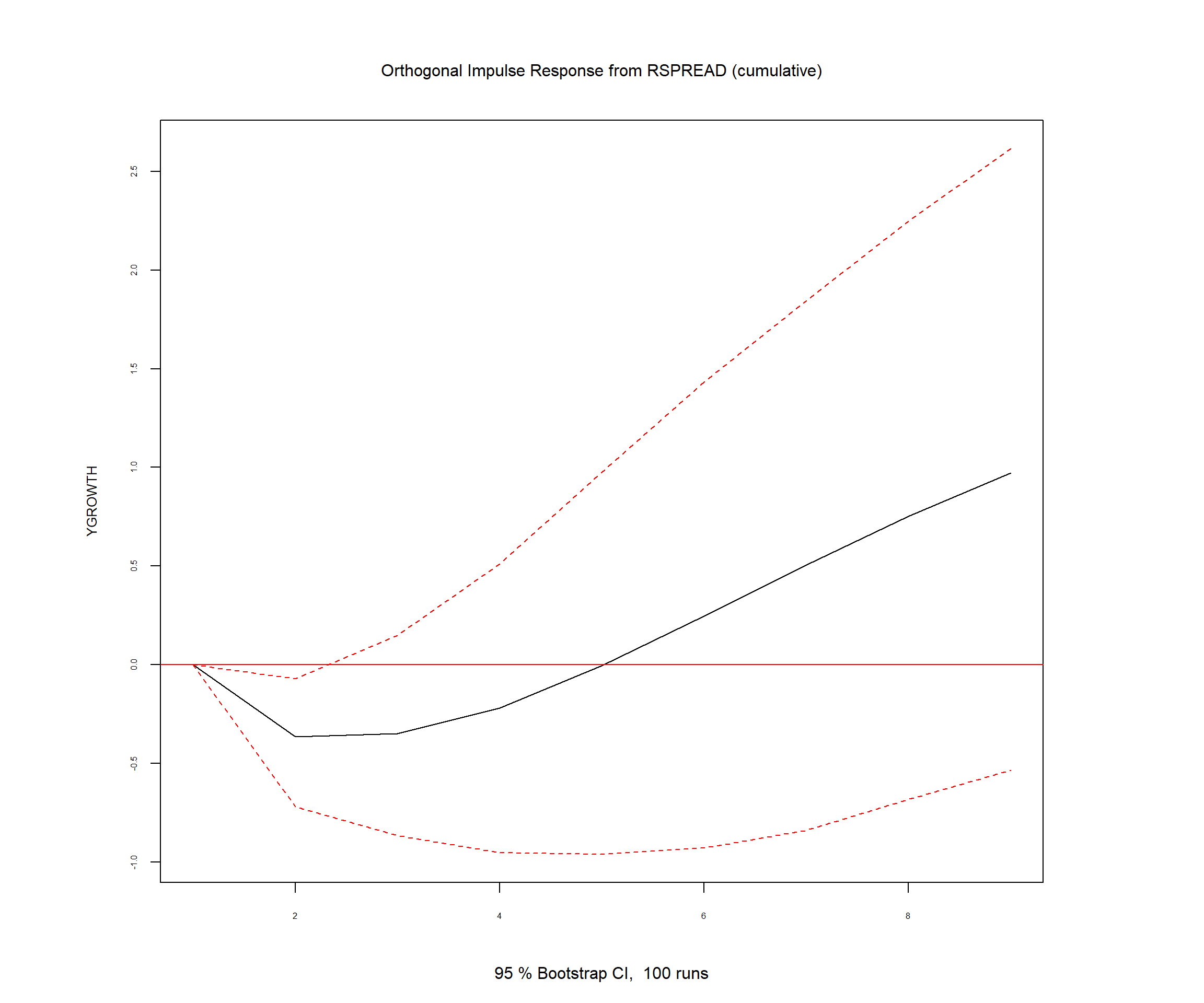

The cumulative OIRF plot shows that the cumulative effect of a shock to the term spread on GDP growth is negative over the first four quarters and then becomes positive and increases over time. However, all estimates of the cumulative OIRF are statistically insignificant at the 5% level, except again for the first-quarter point estimate. Overall, we find that a shock to the term spread has a statistically significant negative effect on GDP growth only in the first quarter, but its effect becomes indistinguishable from zero in subsequent quarters.

# Compute impulse response functions

irf_res <- irf(

var_model,

impulse = "RSPREAD",

response = "YGROWTH",

n.ahead = 8,

ortho = TRUE,

boot = TRUE,

cumulative = FALSE

)

# Compute impulse response functions

irf_res_cum <- irf(

var_model,

impulse = "RSPREAD",

response = "YGROWTH",

n.ahead = 8,

ortho = TRUE,

boot = TRUE,

cumulative = TRUE

)irf_table <- data.frame(

Horizon = 0:8,

Point_Estimate = irf_res$irf$RSPREAD,

Lower_CI = irf_res$Lower$RSPREAD,

Upper_CI = irf_res$Upper$RSPREAD,

Cum_Point_Estimate = irf_res_cum$irf$RSPREAD,

Cum_Lower_CI = irf_res_cum$Lower$RSPREAD,

Cum_Upper_CI = irf_res_cum$Upper$RSPREAD

)

col_names <- c("Horizon", "Point Estimate", "Lower CI", "Upper CI", "Cumulative Point Estimate", "Cumulative Lower CI", "Cumulative Upper CI")

kable(irf_table, digits = 3, col.names = col_names)| Horizon | Point Estimate | Lower CI | Upper CI | Cumulative Point Estimate | Cumulative Lower CI | Cumulative Upper CI |

|---|---|---|---|---|---|---|

| 0 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| 1 | -0.365 | -0.700 | -0.078 | -0.365 | -0.719 | -0.070 |

| 2 | 0.017 | -0.178 | 0.266 | -0.348 | -0.865 | 0.150 |

| 3 | 0.128 | -0.059 | 0.390 | -0.220 | -0.952 | 0.512 |

| 4 | 0.214 | -0.002 | 0.435 | -0.006 | -0.961 | 0.975 |

| 5 | 0.253 | 0.031 | 0.442 | 0.247 | -0.928 | 1.433 |

| 6 | 0.260 | 0.045 | 0.449 | 0.507 | -0.838 | 1.845 |

| 7 | 0.246 | 0.050 | 0.413 | 0.753 | -0.682 | 2.249 |

| 8 | 0.220 | 0.047 | 0.371 | 0.973 | -0.534 | 2.616 |

26.2.6 Forecast error variance decomposition

In addition to impulse response analysis, we can also use the VAR model to analyze the contribution of each shock to the forecast error variance of each variable in the system. This type of analysis is called the forecast error variance decomposition (FEVD).

Definition 26.4 (Forecast error variance decomposition) The forecast error variance decomposition (FEVD) at horizon \(h\) is defined as the proportion of the variance of the forecast error of \(Y_{i,t+h}\) that can be attributed to each shock \(\varepsilon_{jt}\) for \(i,j=1,\ldots, k\).

Consider Equation 26.6 and let \(\bs{Y}_{t+h|t}\) be the \(h\)-period ahead forecast of \(\bs{Y}_t\) based on the information set at time \(t\). We can express the forecast error \(\bs{Y}_{t+h}-\bs{Y}_{t+h|t}\) as follows: \[ \begin{align*} \bs{Y}_{t+h}-\bs{Y}_{t+h|t} = \sum_{j=0}^{h-1}\bs{\Psi}_j\bs{B}\bs{\varepsilon}_{t+h-j}. \end{align*} \]

Given the orthogonality of \(\bs{\varepsilon}_t\), we can compute the variance of the forecast error as follows: \[ \begin{align*} \text{Var}(\bs{Y}_{t+h}-\bs{Y}_{t+h|t}) = \sum_{j=0}^{h-1}\bs{\Psi}_j\bs{B}\bs{B}'\bs{\Psi}_j'. \end{align*} \]

Note that \(\text{Var}(\bs{Y}_{t+h}-\bs{Y}_{t+h|t})\) is a \(k\times k\) matrix. Let \(\sigma_{ij}^2(h)\) be the \((i,j)\)th element of this matrix. The FEVD for the \(i\)th variable at horizon \(h\) due to shock \(\varepsilon_{jt}\) is then given by: \[ \begin{align*} \text{FEVD}_{ij}(h) = \frac{\sigma_{ij}^2(h)}{\sum_{k=1}^k \sigma_{ik}^2(h)}, \end{align*} \] which shows the proportion of the variance of the forecast error of \(Y_{i,t+h}\) that can be attributed to shock \(\varepsilon_{jt}\). Thus, we can use the FEVD to analyze the relative importance of each shock in explaining the variability of each variable in the system over time.

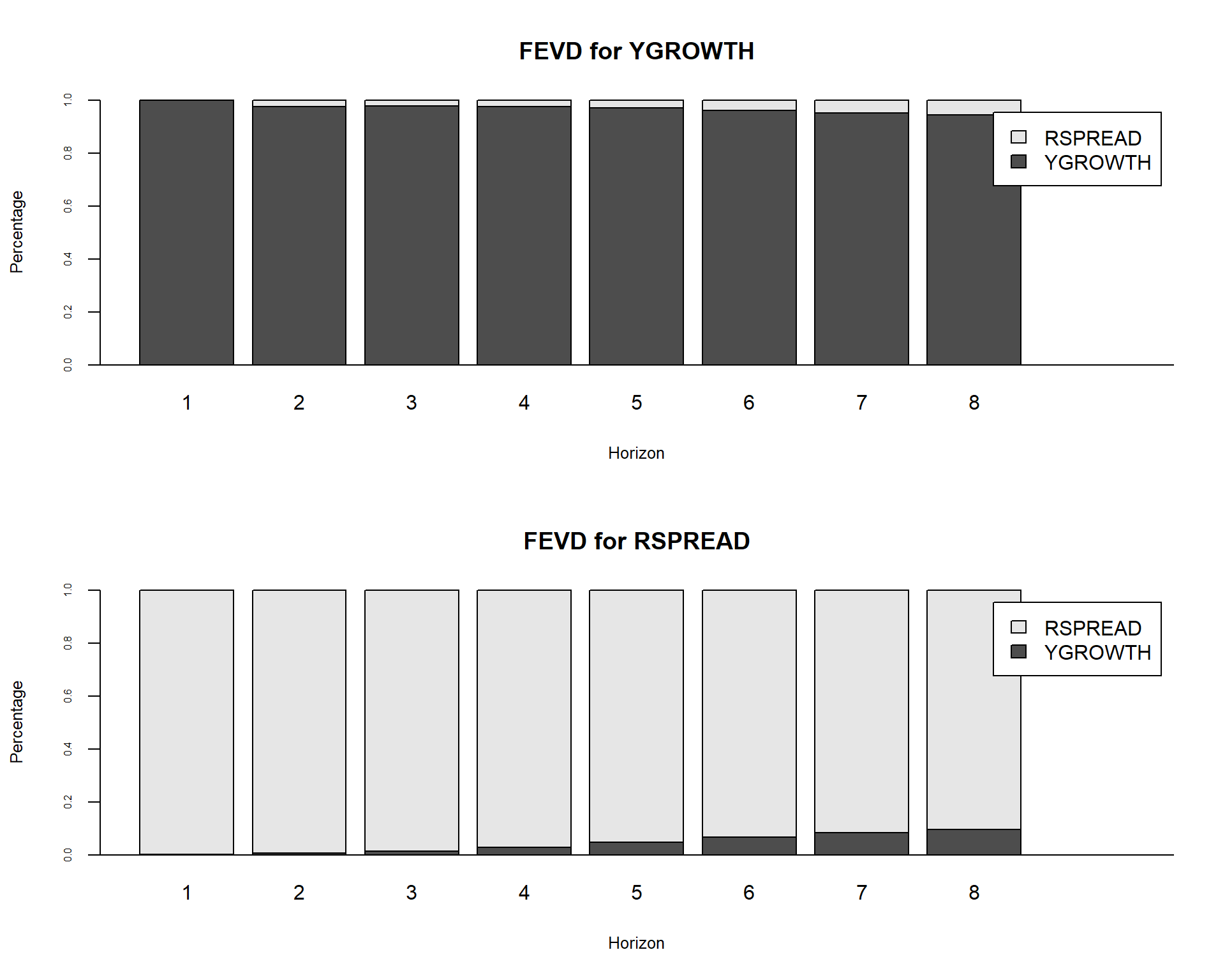

For our VAR(\(2\)) model for the GDP growth rate and the term spread, we use the fevd function from the vars package to compute the FEVD for each variable. The resulting estimates are reported in Table 26.5. The table presents the FEVDs of the GDP growth rate and the term spread at different horizons. The results show that a shock to the term spread explains about 2.3% of the forecast error variance of the GDP growth rate at horizon 1, and its contribution increases to about 6% by horizon 8. Conversely, a shock to the GDP growth rate accounts for most of the forecast error variance of the GDP growth rate, explaining about 97.7% at horizon 1 and about 94% at horizon 8.

For the term spread, a shock to the term spread explains about 99.9% of its forecast error variance at horizon 1, although its contribution declines to about 94% by horizon 8. In contrast, a shock to the GDP growth rate explains only a negligible proportion of the forecast error variance of the term spread at short horizons, but its contribution increases to about 10% by horizon 8. Overall, the results suggest that the term spread has a relatively small but increasing contribution to the forecast error variance of the GDP growth rate over time, while the GDP growth rate has a negligible contribution to the forecast error variance of the term spread at short horizons but an increasing contribution at longer horizons.

# Compute forecast error variance decomposition

fevd_result <- fevd(var_model, n.ahead = 8)# Display the FEVD results in a table format

fevd_table <- data.frame(

Horizon = 1:8,

FEVD_YGROWTH_RSPREAD = fevd_result$YGROWTH[,"RSPREAD"],

FEVD_YGROWTH_YGROWTH = fevd_result$YGROWTH[,"YGROWTH"],

FEVD_RSPREAD_RSPREAD = fevd_result$RSPREAD[,"RSPREAD"],

FEVD_RSPREAD_YGROWTH = fevd_result$RSPREAD[,"YGROWTH"]

)

col_names <- c("Horizon", "FEVD of YGROWTH due to RSPREAD", "FEVD of YGROWTH due to YGROWTH", "FEVD of RSPREAD due to RSPREAD", "FEVD of RSPREAD due to YGROWTH")

kable(fevd_table, digits = 3, col.names = col_names)| Horizon | FEVD of YGROWTH due to RSPREAD | FEVD of YGROWTH due to YGROWTH | FEVD of RSPREAD due to RSPREAD | FEVD of RSPREAD due to YGROWTH |

|---|---|---|---|---|

| 1 | 0.000 | 1.000 | 0.998 | 0.002 |

| 2 | 0.023 | 0.977 | 0.994 | 0.006 |

| 3 | 0.021 | 0.979 | 0.987 | 0.013 |

| 4 | 0.023 | 0.977 | 0.972 | 0.028 |

| 5 | 0.030 | 0.970 | 0.953 | 0.047 |

| 6 | 0.039 | 0.961 | 0.934 | 0.066 |

| 7 | 0.048 | 0.952 | 0.918 | 0.082 |

| 8 | 0.056 | 0.944 | 0.904 | 0.096 |

# Display the FEVD results

plot(fevd_result, cex.axis = 0.5, cex.lab = 0.8)

26.2.7 Structural VAR models

In Sections 26.2.5 and 26.2.6, we used the Cholesky decomposition to orthogonalize shocks and compute the OIRF and FEVD. However, the Cholesky decomposition imposes a recursive structure on the contemporaneous relationships among the VAR variables, which may not be economically meaningful in some cases. To address this issue, we can use structural VAR (SVAR) models, which allow for more flexible contemporaneous relationships among the variables. In an SVAR model, we assume that the error terms \(\bs{u}_t\) in the reduced-form VAR model and the structural shocks \(\bs{\varepsilon}_t\) is formulated in the following way: \[ \begin{align*} \bs{A}\bs{u}_t = \bs{B}\bs{\varepsilon}_t, \end{align*} \tag{26.7}\] where \(\bs{A}\) and \(\bs{B}\) are non-singular matrices of parameters to be estimated. In the literature, the diagonal elements of \(\bs{A}\) are often normalized to 1 to achieve identification. When \(k=3\), the matrices \(\bs{A}\) and \(\bs{B}\) can be expressed as follows: \[ \begin{align*} \bs{A}= \begin{pmatrix} 1 & a_{12} & a_{13}\\ a_{21} & 1 & a_{23}\\ a_{31} & a_{32} & 1 \end{pmatrix},\,\,\, \bs{B}= \begin{pmatrix} b_{11} & b_{12} & b_{13}\\ b_{21} & b_{22} & b_{23}\\ b_{31} & b_{32} & b_{33} \end{pmatrix}. \end{align*} \] These matrices suggest that we can express \(\bs{u}_t\) in terms of \(\bs{\varepsilon}_t\) as follows: \[ \begin{align*} u_{1t} &= b_{11}\varepsilon_{1t}+b_{12}\varepsilon_{2t}+b_{13}\varepsilon_{3t}-a_{12}u_{2t}-a_{13}u_{3t},\\ u_{2t} &= b_{21}\varepsilon_{1t}+b_{22}\varepsilon_{2t}+b_{23}\varepsilon_{3t}-a_{21}u_{1t}-a_{23}u_{3t},\\ u_{3t} &= b_{31}\varepsilon_{1t}+b_{32}\varepsilon_{2t}+b_{33}\varepsilon_{3t}-a_{31}u_{1t}-a_{32}u_{2t}. \end{align*} \]

From Equation 26.7, we can derive the following relationship between the covariance matrix of the reduced-form errors \(\bs{\Sigma}\) and the parameters in \(\bs{A}\) and \(\bs{B}\): \[ \begin{align*} \bs{\Sigma} = \E(\bs{u}_t\bs{u}_t') = \bs{A}^{-1}\bs{B}\E(\bs{\varepsilon}_t\bs{\varepsilon}_t')\bs{B}'(\bs{A}^{-1})' = \bs{A}^{-1}\bs{B}\bs{B}'(\bs{A}^{-1})'. \end{align*} \tag{26.8}\]

The coefficients in \(\bs{A}\) and \(\bs{B}\) are identified if they can be uniquely determined from Equation 26.8. Since \(\bs{\Sigma}\) is symmetric, it has \(k(k+1)/2\) unique elements. Therefore, the total number of free coefficients in \(\bs{A}\) and \(\bs{B}\) cannot exceed \(k(k+1)/2\) for identification to be possible. This requirement is known as the order condition for identification. On the other hand, \(\bs{A}\) and \(\bs{B}\) together contain \(2k^2-k\) parameters (since the diagonal elements of \(\bs{A}\) are normalized to 1). For \(k=3\), \(\bs{A}\) and \(\bs{B}\) contain 15 parameters, whereas \(\bs{\Sigma}\) has only 6 unique elements. Therefore, at least 9 restrictions must be imposed on the parameters in \(\bs{A}\) and \(\bs{B}\) to achieve identification.

In the literature, various types of restrictions have been proposed to achieve identification in SVAR models, including short-run restrictions, long-run restrictions, and sign restrictions. The choice among these approaches depends on the economic setting and the research question of interest. We refer readers to Lütkepohl (2005) and Hansen (2022) for comprehensive discussions of these identification strategies and their implications for the interpretation of SVAR models.

In R, the SVAR function from the vars package can be used to estimate SVAR models. This function allows the user to specify the type of identifying restrictions to impose on the model. In particular, the Amat and Bmat arguments can be used to impose restrictions on the parameters in \(\bs{A}\) and \(\bs{B}\), respectively. After estimating the SVAR model, the OIRF and FEVD can be computed using the estimated \(\bs{A}\) and \(\bs{B}\) matrices, similar to the Cholesky decomposition case. The relatively new svars package provides additional functionality for estimating SVAR models under heteroskedasticity-based identification schemes, as well as for conducting inference on the OIRF and FEVD. For the vars package, see Pfaff (2008), and for the svars package, see Lange et al. (2021).

26.3 Multi-period forecasts

In this section, we discuss two forecasting methods for generating multi-period forecasts: the iterated method and the direct method. In the iterated method, we first forecast the next period’s value and then use this forecast to predict the value for the subsequent period. This process is repeated until the desired forecast horizon is reached. For example, the one-period, two-period, and three-period-ahead iterated forecasts based on an AR(\(p\)) model are computed as follows: \[ \begin{align*} &\hat{Y}_{T+1|T}=\hat{\beta}_0+\hat{\beta}_1Y_{T}+\hat{\beta}_2Y_{T-1}+\hat{\beta}_3Y_{T-2}+\ldots+\hat{\beta}_pY_{T-p+1},\\ &\hat{Y}_{T+2|T}=\hat{\beta}_0+\hat{\beta}_1{\color{steelblue} \hat{Y}_{T+1|T}}+\hat{\beta}_2Y_T+\hat{\beta}_3Y_{T-1}+\ldots+\hat{\beta}_pY_{T-p+2},\\ &\hat{Y}_{T+3|T}=\hat{\beta}_0+\hat{\beta}_1{\color{steelblue}\hat{Y}_{T+2|T}}+\hat{\beta}_2{\color{steelblue}\hat{Y}_{T+1|T}} +\hat{\beta}_3Y_{T}+\ldots+\hat{\beta}_pY_{T-p+3}, \end{align*} \] where the \(\hat{\beta}\)’s are the OLS estimates of the AR(\(p\)) coefficients. Note that we use the forecast \(\hat{Y}_{T+1|T}\) to compute the two-step-ahead forecast and the forecasts \(\hat{Y}_{T+1|T}\) and \(\hat{Y}_{T+2|T}\) to compute the three-step-ahead forecast. We can continue this process (iterating) to produce forecasts further into the future.

Using the same approach, we can also generate multi-period forecasts for VAR models. We need to first compute the one-step ahead forecast for all variables in the VAR model. Then, we use these forecasts to generate the two-step ahead forecast, and so on. For example, in our two-variable VAR(\(p\)) model in Equation 26.1, the two-step ahead forecast for \(Y_t\) is \[ \begin{align*} \hat{Y}_{T+2|T}&= \hat{\beta}_{10}+\hat{\beta}_{11}\hat{Y}_{T+1|T}+\hat{\beta}_{12}Y_{T}+\cdots+\hat{\beta}_{1p}Y_{T+2-p}\\ &+\hat{\gamma}_{11}\hat{X}_{T+1|T}+\hat{\gamma}_{12}X_T+\cdots+\hat{\gamma}_{1p}X_{T+2-p}, \end{align*} \] where \(\hat{Y}_{T+1|T}\) and \(\hat{X}_{T+1|T}\) are the one-step ahead forecasts of \(Y_{T+1}\) and \(X_{T+1}\), respectively.

In the VAR(\(2\)) model that we consider in Section 26.2.5 for the GDP growth rate and the term spread, we use the predict function to generate multi-period forecasts. We report the forecasted values in Table 26.2 and Table 26.3, and the forecast plots in Figure 26.2.

In the direct method, we generate the multi-period forecasts using a single regression with the dependent variable being the variable to be forecasted at the forecast horizon and the regressors are predictors lagged at the forecast horizon. Consider the first equation in the VAR(\(2\)) model in Equation 26.1. Then, we can estimate the following regression model to generate \(h\)-step ahead forecasts for \(Y_t\): \[ \begin{align*} Y_t &= \delta_{0}+\delta_{1}Y_{t-h}+\delta_{2}Y_{t-h-1}+\cdots+\delta_{p}Y_{t-h-p+1}\\ &+\delta_{p+1}X_{t-h}+\cdots+\delta_{2p}X_{t-p-h+1}+u_{t}, \end{align*} \] where \(\delta\)’s are the unknown parameters. This model can be estimated by the OLS estimator. Since the error term in this regression can be autocorrelated, we need to use heteroskedasticity-and autocorrelation-consistent (HAC) standard errors to obtain valid inference. Then, the \(h\)-step ahead forecast for \(Y_t\) is given by \[ \begin{align*} \hat{Y}_{T+h|T} &= \hat{\delta}_{0}+\hat{\delta}_{1}Y_{T}+\hat{\delta}_{2}Y_{T-1}+\cdots+\hat{\delta}_{p+1}Y_{T-p+1}\\ &+\hat{\delta}_{p+1}X_{T}+\cdots+\hat{\delta}_{2p}X_{T-p+1}. \end{align*} \]

In practice, the iterated method is preferred over the direct method for two reasons (Stock and Watson 2020). First, if the postulated model is correct, the iterated method can produce more accurate forecasts than the direct method because the postulated model is estimated more efficiently in the iterated method. Second, the iterated method tends to produce smoother forecasts. In contrast, the direct approach requires estimating a separate regression for each forecast horizon, which can result in greater forecast volatility compared to the iterated method.

26.4 Orders of integration

We introduced the random walk model for the stochastic trend in Chapter 24. The version with a drift is specified as \[ \begin{align} Y_t = \beta_0+Y_{t-1}+u_t, \end{align} \tag{26.9}\] where \(u_t\) is an error term. Although \(Y_t\) is non-stationary, its first difference \(\Delta Y_t\) is stationary. We use the order of integration to characterize the stochastic trend in a time series.

Definition 26.5 (Orders of integration) If a time series is stationary, it is said to be integrated of order zero, denoted as \(I(0)\). A time series that follows a random walk trend is said to be integrated of order one, denoted as \(I(1)\).

According to definition Definition 26.5, if \(Y_t\) is \(I(1)\), then \(\Delta Y_t\) is \(I(0)\), i.e., \(\Delta Y_t\) is stationary. Similarly, if \(Y_t\) is \(I(2)\), then \(\Delta Y_t\) is \(I(1)\), and it second difference \(\Delta^2Y_t=(\Delta Y_t-\Delta Y_{t-1})\) is \(I(0)\) i.e., \(\Delta^2Y_t\) is stationary. In general, if \(Y_t\) is integrated of order \(d\)-that is, if \(Y_t\) is \(I(d)\) -then \(Y_t\) must be differenced \(d\) times to eliminate its stochastic trend; that is, \(\Delta^dY_t\) is stationary.

26.5 Cointegration and error correction models

26.5.1 Cointegration

When two time series share the same stochastic trend, they tend to move together in the long run. The concept of cointegration describes this relationship between time series that exhibit a common stochastic trend.

Definition 26.6 (Cointegration) Suppose that \(Y_{1t}\) and \(Y_{2t}\) are \(I(1)\). If \(Y_{1t} - \theta Y_{2t}\) is \(I(0)\) for a parameter \(\theta\), then \(Y_{1t}\) and \(Y_{2t}\) are said to be cointegrated, with \(\theta\) called the cointegrating parameter.

If \(Y_{1t}\) and \(Y_{2t}\) are cointegrated, then the difference \(Y_{1t} - \theta Y_{2t}\) eliminates the common stochastic trend and therefore is stationary. We call this difference the error correction term.

26.5.2 Vector error correction models

A VAR model for the first difference of cointegrated variables can be augmented by including the error correction term as an additional regressor. Such an augmented VAR model is called a vector error correction model (VECM). The VECM for \(Y_{1t}\) and \(Y_{2t}\) is given by \[ \begin{align} &\Delta Y_{1t}=a_{1}+\delta_{11}\Delta Y_{1,t-1}+\ldots+\delta_{1p}\Delta Y_{1,t-p}+\gamma_{11}\Delta Y_{2,t-1}+\ldots+\gamma_{1p}\Delta Y_{2,t-p}\nonumber\\ &\quad\quad\quad+\alpha_1(Y_{1,t - 1} - \theta Y_{2,t-1})+u_{1t},\\ &\Delta Y_{2t}=a_{2}+\delta_{21}\Delta Y_{1,t-1}+\ldots+\delta_{2p}\Delta Y_{1,t-p}+\gamma_{21}\Delta Y_{2,t-1}+\ldots+\gamma_{2p}\Delta Y_{2,t-p}\nonumber\\ &\quad\quad\quad+\alpha_2(Y_{1,t - 1} - \theta Y_{2,t-1})+u_{2t}, \end{align} \] where \(a_{i}\), \(\delta_{ij}\), \(\gamma_{ij}\), and \(\alpha_i\) for \(i,j\in\{1,2\}\) are unknown parameters, and \(u_{1t}\) and \(u_{2t}\) are the error terms. Note that the error correction term \((Y_{1,t - 1} - \theta Y_{2,t-1})\) is included in both equations of the VECM. The parameters \(\alpha_1\) and \(\alpha_2\) are called the adjustment parameters. If \(\alpha_i\) is negative, then \(Y_{it}\) tends to adjust towards the long-run equilibrium relationship defined by the error correction term.

To express the VECM in matrix form, we define the following matrices: \[ \begin{align*} &\bs{Y}_t= \begin{pmatrix} Y_{1t}\\ Y_{2t} \end{pmatrix},\, \bs{\Delta Y}_t= \begin{pmatrix} \Delta Y_{1t}\\ \Delta Y_{2t} \end{pmatrix},\, \bs{a}= \begin{pmatrix} a_{1}\\ a_{2} \end{pmatrix},\, \bs{B}_j= \begin{pmatrix} \delta_{1j}&\gamma_{1j}\\ \delta_{2j}&\gamma_{2j} \end{pmatrix},\\ & \bs{\alpha}= \begin{pmatrix} \alpha_1\\ \alpha_2 \end{pmatrix},\, \bs{\beta}= \begin{pmatrix} 1\\ -\theta \end{pmatrix},\,\text{and}\, \bs{u}_t= \begin{pmatrix} u_{1t}\\ u_{2t} \end{pmatrix}, \end{align*} \] for \(j=1,2,\ldots,p\). Then, the VECM in matrix form is given by \[ \begin{align} \bs{\Delta Y}_t=\bs{a}+\bs{B}_1\bs{\Delta Y}_{t-1}+\ldots+\bs{B}_{p}\bs{\Delta Y}_{t-p}+\bs{\alpha}\bs{\beta}^{'}\bs{Y}_{t-1}+\bs{u}_t. \end{align} \tag{26.10}\]

In the VECM model, our goal is to use the past value of the error correction term to predict the future values of \(\bs{\Delta Y}_t\).

The augmentation of the VAR with the error correction term is not arbitrary. To see this, consider a VAR(2) model for \(k\) variables: \[ \begin{align*} \bs{Y}_t &= \bs{a} + \bs{A}_1\bs{Y}_{t-1}+\bs{A}_2\bs{Y}_{t-2}+\bs{u}_t. \end{align*} \]

Subtracting \(\bs{Y}_{t-1}\) from both sides and re-arranging, we obtain \[ \begin{align*} \bs{Y}_t - \bs{Y}_{t-1}&= \bs{a} + \bs{A}_1\bs{Y}_{t-1} - \bs{Y}_{t-1}+\bs{A}_2\bs{Y}_{t-2}+\bs{u}_t\\ &= \bs{a} - (\bs{I}_k - \bs{A}_1)\bs{Y}_{t-1}+\bs{A}_2\bs{Y}_{t-2}+\bs{u}_t\\ &= \bs{a} - (\bs{I}_k - \bs{A}_1 - \bs{A}_2)\bs{Y}_{t-1}-\bs{A}_2\bs{Y}_{t-1}+\bs{A}_2\bs{Y}_{t-2}+\bs{u}_t. \end{align*} \]

Let \(\bs{\Pi} = - (\bs{I}_k - \bs{A}_1 - \bs{A}_2)\) and \(\bs{B}_1 = -\bs{A}_2\). Then, we can express the above equation as

\[ \begin{align*} \bs{\Delta Y}_t &= \bs{a} + \bs{\Pi} \bs{Y}_{t-1} + \bs{B}_1 \bs{\Delta Y}_{t-1}+\bs{u}_t. \end{align*} \]

This last equation resembles the VECM representation in Equation 26.10 with one lag, i.e., \(p=1\). If \(\bs{Y}_t\) has a stochastic trend, then one or more of the roots of \(\operatorname{det}(\bs{\Pi})\) must be unity (Lütkepohl 2005, chap. 2). In that case, \(\bs{\Pi}\) is singular and its rank \(r\) must be less than \(k\). Hence, \(\bs{\Pi}\) can be decomposed as \(\bs{\Pi}=\bs{\alpha}\bs{\beta}^{'}\), where \(\bs{\alpha}\) and \(\bs{\beta}\) are \(k\times r\) matrices.

This decomposition of \(\bs{\Pi}\) is not unique. For any positive definite \(r\times r\) matrix \(\bs{Q}\), we can write \(\bs{\Pi}=\bs{\alpha}^\star\bs{\beta}^{\star'}\), where \(\bs{\alpha}^\star = \bs{\alpha}\bs{Q}\) and \(\bs{\beta}^{\star}=\bs{\beta}\bs{Q}^{-1}\). Therefore, cointegration relations are not unique. To avoid this problem, restrictions on \(\bs{\beta}\) and/or \(\bs{\alpha}\) can be imposed. Normalizing the first component of \(\bs{\beta}\) to unity in the definition above serves to avoid the identification problem.

26.5.3 Estimating the cointegrating parameter

In order to form a VECM, we first need to check whether the variables are cointegrated. We can use the following two-step approach to decide whether \(Y_{1t}\) and \(Y_{2t}\) are cointegrated:

Step 1: Estimate the cointegrating coefficient \(\theta\) by the OLS estimator from the regression \[ \begin{align} Y_{1t} = \mu_0 + \theta Y_{2t} + v_t, \end{align} \tag{26.11}\] where \(\mu_0\) is the intercept term, and \(v_t\) is the error term.

Step 2: Compute the residual \(\hat{v}_t\). Then, use the ADF test (with an intercept but no time trend) to test whether \(\hat{v}_t\) is stationary. In Table 26.6, we provide the critical values for the ADF statistic.

If \(\hat{v}_t\) is \(I(0)\), then we conclude that \(Y_{1t}\) and \(Y_{2t}\) are cointegrated. This two-step procedure is called the Engle-Granger Augmented Dickey-Fuller test (EG-ADF test) for cointegration.

| Number of X’s in Equation 26.12 | 10% | 5% | 1% |

|---|---|---|---|

| 1 | -3.12 | -3.41 | -3.96 |

| 2 | -3.52 | -3.80 | -4.36 |

| 3 | -3.84 | -4.16 | -4.73 |

| 4 | -4.20 | -4.49 | -5.07 |

We estimate the cointegrating parameter \(\theta\) in the two-step procedure by the OLS estimator. If the variables are cointegrated, the OLS estimator is consistent but has a non-standard distribution (see Theorem 16.19 in Hansen (2022)). There is also an alternative estimator called the dynamic OLS (DOLS) estimator, which is more efficient than the OLS estimator. The DOLS estimator is based on the following extended version of Equation 26.12: \[ \begin{align} Y_{1t}=\mu_0+\theta Y_{2t}+\sum_{j=-p}^p\delta_j\Delta Y_{2,t-j}+u_t, \end{align} \tag{26.12}\] where the regressors are \(Y_{2t}, \Delta Y_{2,t+p},\ldots,\Delta Y_{2,t-p}\). If the variables are cointegrated, the DOLS estimator is consistent and asymptotically normal. For inference, we need to use the HAC standard errors.

So far we assume only two variables for the cointegration analysis. However, the cointegration analysis can be extended to multiple variables. If there are three \(I(1)\) variables \(Y_{1t}\), \(Y_{2t}\) and \(Y_{3t}\), then they are cointegrated if the following linear combination is stationary: \(Y_{1t}-\theta_1Y_{2t}-\theta_2Y_{3t}\) for some parameters \(\theta_1\) and \(\theta_2\). Note that when there are multiple variables, there can be multiple cointegrating relationships among the variables. For example, in the case of three \(I(1)\) variables \(Y_{1t}\), \(Y_{2t}\) and \(Y_{3t}\), one cointegrating relationship can be \(Y_{1t}-\theta_1Y_{2t}\), and another cointegrating relationship can be \(Y_{2t}-\theta_2Y_{3t}\) for some parameters \(\theta_1\) and \(\theta_2\).

We can extend the EG-ADF test to test for cointegration among multiple variables. For example, in the case of the three \(I(1)\) variables, we need to estimate the following regression model with the OLS estimator: \[ \begin{align} Y_{1t}=\mu_0+\theta_1Y_{2t}+\theta_2Y_{3t}+v_t. \end{align} \tag{26.13}\]

In the second step, we need to check whether \(\hat{v}_t\) is stationary using the EG-ADF test with the critical values from Table 26.6. Instead of using the OLS estimator, we can also use the DOLS estimator to estimate the cointegrating parameters in Equation 26.13. In this case, the DOLS estimator is based on the following regression model: \[ \begin{align} Y_{1t}=\mu_0+\theta_1Y_{1t}+\theta_2Y_{2t}+\sum_{j=-p}^p\delta_j\Delta Y_{1,t-j}+\sum_{j=-p}^p\gamma_j\Delta Y_{3,t-j}+u_t. \end{align} \tag{26.14}\]

26.5.4 Alternative VECM specifications

In Equation 26.10, we consider a VECM model that includes an intercept but no linear time trend. Alternative VECM specifications exist depending on whether an intercept and a linear time trend are included in the VECM and the error correction term. Lütkepohl (2005) and Hansen (2022) provide a detailed discussion on these alternative VECM models. Below, we list some major options.

Model 1: Both the VECM and the error correction term do not include an intercept: \[ \begin{align} \bs{\Delta Y}_t=\bs{B}_1\bs{\Delta Y}_{t-1}+\ldots+\bs{B}_{p}\bs{\Delta Y}_{t-p}+\bs{\alpha}\bs{\beta}^{'}\bs{Y}_{t-1}+\bs{u}_t. \end{align} \tag{26.15}\] According to Hansen (2022), this model is not suitable for empirical applications.

Model 2: The error correction term includes an intercept but the VECM does not include an intercept: \[ \begin{align} \bs{\Delta Y}_t=\bs{B}_1\bs{\Delta Y}_{t-1}+\ldots+\bs{B}_{p}\bs{\Delta Y}_{t-p}+\bs{\alpha}\bs{\beta}^{'}(\bs{Y}_{t-1}+\bs{\mu})+\bs{u}_t. \end{align} \tag{26.16}\] where \(\bs{\mu}\) is the intercept in the error correction term. This model should be used for non-trended series such as interest rates.

Model 3: The VECM includes an intercept term but the error correction term does not include an intercept: \[ \begin{align} \bs{\Delta Y}_t=\bs{a}+\bs{B}_1\bs{\Delta Y}_{t-1}+\ldots+\bs{B}_{p}\bs{\Delta Y}_{t-p}+\bs{\alpha}\bs{\beta}^{'}\bs{Y}_{t-1}+\bs{u}_t. \end{align} \tag{26.17}\] The intercept term provides a drift component for \(\bs{\Delta Y}_t\) and a linear trend for \(\bs{Y}_t\). Therefore, this model should be used for series that have a linear time trend.

Model 4: The VECM includes an intercept and the error correction term includes a linear time trend: \[ \begin{align} \bs{\Delta Y}_t=\bs{a}+\bs{B}_1\bs{\Delta Y}_{t-1}+\ldots+\bs{B}_{p}\bs{\Delta Y}_{t-p}+\bs{\alpha}\bs{\beta}^{'}(\bs{Y}_{t-1}+\bs{\mu}t)+\bs{u}_t. \end{align} \tag{26.18}\] This model should be used for series that have a linear time trend. In this model, the vector error correction term contains a linear time trend and a stationary process.

Model 5: The VECM includes an intercept and a linear trend, and the error correction term includes none of them: \[ \begin{align} \bs{\Delta Y}_t=\bs{a}+\bs{b}t+\bs{B}_1\bs{\Delta Y}_{t-1}+\ldots+\bs{B}_{p}\bs{\Delta Y}_{t-p}+\bs{\alpha}\bs{\beta}^{'}\bs{Y}_{t-1}+\bs{u}_t. \end{align} \tag{26.19}\] This model suggests that the level series have a quadratic linear time trend. According to Hansen (2022), this model is not a typical model for empirical applications.

26.5.5 Johansen cointegration test

According to Granger representation theorem (Engle and Granger 1987), there are \(r\) cointegrating relationships if the rank of the matrix \(\bs{\Pi}=\bs{\alpha}\bs{\beta}^{'}\) is \(r\). This suggests that we can test the presence of \(r\) cointegrating relationships by testing \(H_0:\text{rank}(\bs{\Pi})=r\). The alternative hypothesis takes two forms: (i) \(H_1:r<\text{rank}(\bs{\Pi})\leq m\), where \(m\) is the number of variable in the VECM, and (ii) \(H_1:\text{rank}(\bs{\Pi})=r+1\). As a result, the null and alternative hypotheses take the following forms: \[ \begin{align} &\text{Case 1}:\,H_0:\text{rank}(\bs{\Pi})=r\,\text{versus}\, H_1:r<\text{rank}(\bs{\Pi})\leq m,\\ &\text{Case 2}:\, H_0:\text{rank}(\bs{\Pi})=r\,\text{versus}\, H_1:\text{rank}(\bs{\Pi})=r+1. \end{align} \]

In both cases, the likelihood ratio statistic is used to test the null hypothesis, which is known as the Johansen cointegration test. The test statistic for the first case is referred to as the trace statistic, while the test statistic for the second case is called the maximum eigenvalue statistic. Under the null hypothesis, both statistics follow a nonstandard distribution; therefore, the critical values must be determined through simulations.

In practice, we use a sequence of null hypotheses to determine the number of cointegrating relationships: \[ \begin{align} &H_0:\text{rank}(\bs{\Pi})=0,\,H_0:\text{rank}(\bs{\Pi})=1,\, \ldots\,, H_0:\text{rank}(\bs{\Pi})=m-1. \end{align} \]

We test each null hypothesis sequentially and stop when we fail to reject the null hypothesis. The number of cointegrating relationships is then given by the last null hypothesis that we fail to reject.

26.5.6 An empirical application

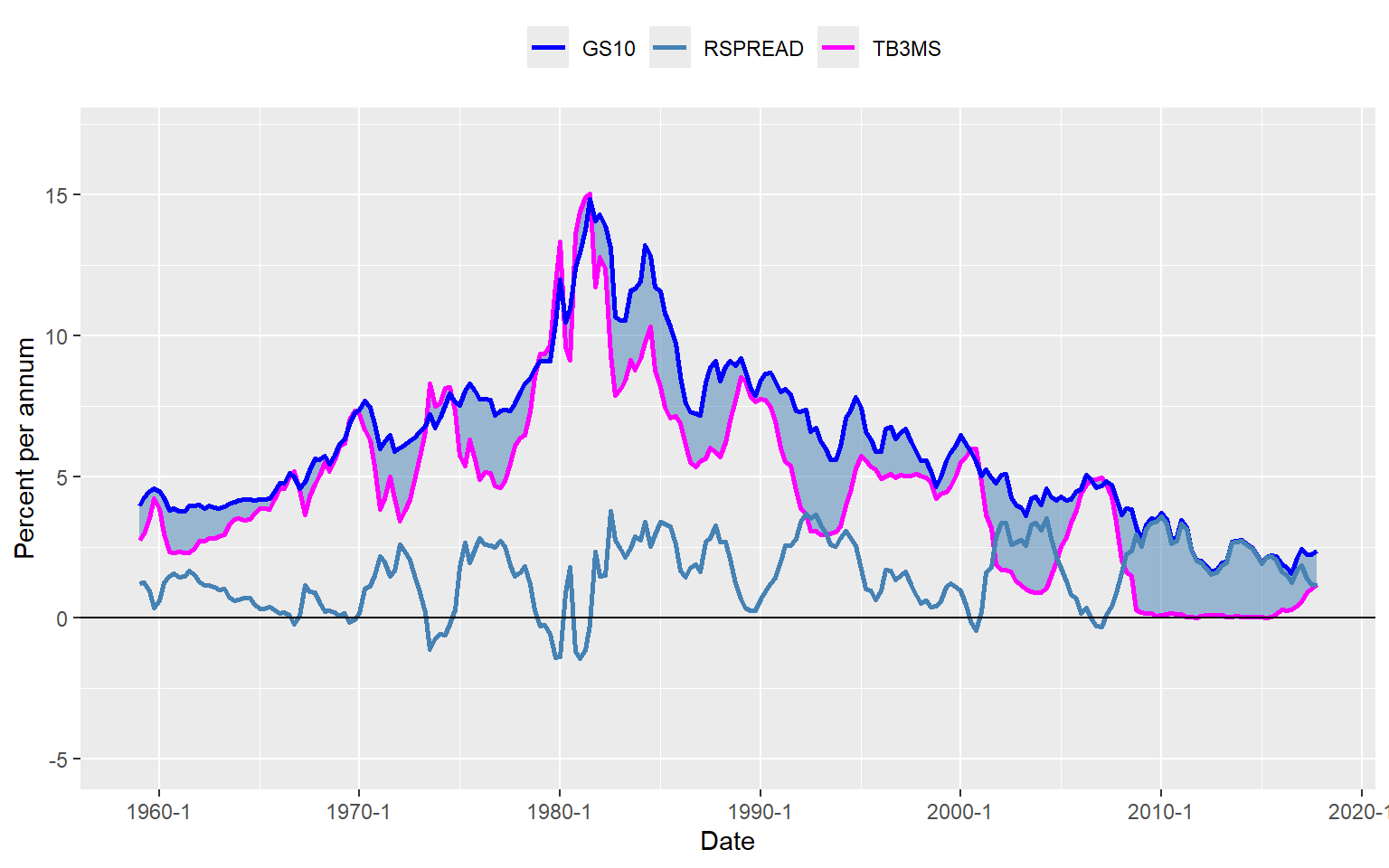

As an example, we examine the relationship between short- and long-term interest rates: (i) the interest rate on 3-month Treasury bills (TB3MS) and (ii) the interest rate on 10-year Treasury bonds (GS10). Figure 26.6 displays the time series plots. Both interest rates were low during the 1960s, rose throughout the 1970s to peak in the early 1980s, and declined thereafter. However, the difference between long-term and short-term interest rates, known as the term spread (also shown in Figure 26.6), does not appear to exhibit a trend. These patterns suggest that long-term and short-term interest rates are cointegrated, as both series share a common stochastic trend and exhibit similar long-run behavior.

# Import growth data

mydata <- read_dta("data/FRED-QD.dta")

# Create a ts object

tsMydata <- ts(mydata, start = c(1959, 1), frequency = 4)

# 3-month interest rate (short-term rate)

TB3MS <- tsMydata[, "tb3ms"]

# 10-year interest rate (long-term rate)

GS10 <- tsMydata[, "gs10"]

# Term spread

RSPREAD <- GS10 - TB3MS# Plots of the interest rates and the term spread

# Prepare data frame from ts object

df <- data.frame(

Date = as.yearqtr(time(tsMydata)),

TB3MS = as.numeric(tsMydata[, "tb3ms"]),

GS10 = as.numeric(tsMydata[, "gs10"])

)

df$RSPREAD <- df$GS10 - df$TB3MS

# Shaded area between GS10 and TB3MS

df$ymin <- pmin(df$TB3MS, df$GS10)

df$ymax <- pmax(df$TB3MS, df$GS10)

# Plot directly without long format

ggplot(df) +

# Shaded area

geom_ribbon(aes(x = Date, ymin = ymin, ymax = ymax),

fill = "steelblue", alpha = 0.5

) +

# Lines

geom_line(aes(x = Date, y = TB3MS, color = "TB3MS"), linewidth = 1) +

geom_line(aes(x = Date, y = GS10, color = "GS10"), linewidth = 1) +

geom_line(aes(x = Date, y = RSPREAD, color = "RSPREAD"), linewidth = 1) +

# Horizontal line at 0

geom_hline(yintercept = 0, linetype = "solid") +

# Axis labels

labs(x = "Date", y = "Percent per annum", color = "") +

# Y-axis limits

ylim(-5, 17) +

# Colors

scale_color_manual(values = c(

"TB3MS" = "magenta",

"GS10" = "blue",

"RSPREAD" = "steelblue"

)) +

theme(legend.position = "top")

We can use the two-step Engle-Granger test to check whether these interest rates are cointegrated. In the first step, we estimate the cointegrating parameter \(\theta\) by the OLS estimator from the following regression: \[ \begin{align} \text{tb3ms}_t = \mu + \theta \text{gs10}_t + v_t. \end{align} \tag{26.20}\]

# Estimate cointegrating relationship: TB3MS ~ GS10

results <- lm(TB3MS ~ GS10, data = df)The estimation results are presented in Table Table 26.7. The estimated model is \[ \begin{align} \widehat{\text{tb3ms}}_{t}=-1.71+1.03\times\text{gs10}_t. \end{align} \]

Thus, the estimated cointegrating parameter is \(\hat{\theta}=1.03\).

# Estimation results from Step 1

# Display OLS results

modelsummary(results,

fmt = 3, stars = TRUE,

gof_omit = "AIC|BIC|Log"

)| (1) | |

|---|---|

| (Intercept) | -1.712*** |

| (0.184) | |

| GS10 | 1.028*** |

| (0.027) | |

| Num.Obs. | 236 |

| R2 | 0.860 |

| R2 Adj. | 0.859 |

| F | 1433.488 |

| RMSE | 1.17 |

| + p < 0.1, * p < 0.05, ** p < 0.01, *** p < 0.001 | |

In the second step, we use the EG-ADF test to test whether \(\hat{v}_t\) is stationary. The ADF test statistic given below is -4.52, which is less than the 5% critical value -3.41 given in Table 26.6. Thus, we can reject the null hypothesis of unit root. As a result, this two-step approach suggests that gs10 and tb3ms are cointegrated.

###############################################

# Augmented Dickey-Fuller Test Unit Root Test #

###############################################

Test regression drift

Call:

lm(formula = z.diff ~ z.lag.1 + 1 + z.diff.lag)

Residuals:

Min 1Q Median 3Q Max

-2.2886 -0.2311 0.0484 0.2895 3.1167

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 6.826e-05 3.435e-02 0.002 0.998416

z.lag.1 -1.355e-01 3.002e-02 -4.515 1.01e-05 ***

z.diff.lag 2.334e-01 6.399e-02 3.648 0.000327 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.5255 on 231 degrees of freedom

Multiple R-squared: 0.1063, Adjusted R-squared: 0.09857

F-statistic: 13.74 on 2 and 231 DF, p-value: 2.303e-06

Value of test-statistic is: -4.5154 10.1945

Critical values for test statistics:

1pct 5pct 10pct

tau2 -3.46 -2.88 -2.57

phi1 6.52 4.63 3.81Alternatively, we can resort to the dynamic OLS (DOLS) estimator to estimate the cointegrating coefficient. The estimation results are presented in Table 26.8. The estimated cointegrating parameter is \(\hat{\theta}\approx1\), which is close to the value obtained from the two-step approach.

modelsummary(

models = list("Model" = m2),

stars = T,

vcov = m2Se

)| Model | |

|---|---|

| (Intercept) | -1.574*** |

| (0.309) | |

| GS10 | 1.009*** |

| (0.041) | |

| L(diff(GS10), k = -5 × 5)-5 | 0.235 |

| (0.172) | |

| L(diff(GS10), k = -5 × 5)-4 | 0.357* |

| (0.125) | |

| L(diff(GS10), k = -5 × 5)-3 | 0.447** |

| (0.110) | |

| L(diff(GS10), k = -5 × 5)-2 | 0.456** |

| (0.122) | |

| L(diff(GS10), k = -5 × 5)-1 | 0.437** |

| (0.134) | |

| L(diff(GS10), k = -5 × 5)0 | 0.402* |

| (0.179) | |

| L(diff(GS10), k = -5 × 5)1 | 0.413* |

| (0.129) | |

| L(diff(GS10), k = -5 × 5)2 | 0.188 |

| (0.151) | |

| L(diff(GS10), k = -5 × 5)3 | 0.436** |

| (0.144) | |

| L(diff(GS10), k = -5 × 5)4 | 0.382* |

| (0.130) | |

| L(diff(GS10), k = -5 × 5)5 | 0.650*** |

| (0.146) | |

| Num.Obs. | 225 |

| R2 | 0.903 |

| R2 Adj. | 0.897 |

| AIC | 657.7 |

| BIC | 705.5 |

| Log.Lik. | -314.833 |

| RMSE | 0.98 |

| Std.Errors | Custom |

| + p < 0.1, * p < 0.05, ** p < 0.01, *** p < 0.001 | |

Since both gs10 and tb3ms are cointegrated, we can estimate the VECM model for these two variables. Since these series are non-trended series, we consider the following VECM specification: \[

\begin{align}

\Delta\text{tb3ms}_t&=\delta_{11}\Delta\text{tb3ms}_{t-1}+\delta_{12}\Delta\text{tb3ms}_{t-2}+\delta_{13}\Delta\text{tb3ms}_{t-3}\\

&+\gamma_{11}\Delta\text{gs10}_{t-1}+\gamma_{12}\Delta\text{gs10}_{t-2}+\gamma_{13}\Delta\text{gs10}_{t-3}\\

&+\alpha_1(\text{tb3ms}_{t-1}-\theta\text{gs10}_{t-1}-\mu)+u_{1t},

\end{align}

\] \[

\begin{align}

\Delta\text{gs10}_t&=\delta_{21}\Delta\text{tb3ms}_{t-1}+\delta_{22}\Delta\text{tb3ms}_{t-2}+\delta_{23}\Delta\text{tb3ms}_{t-3}\\

&+\gamma_{21}\Delta\text{gs10}_{t-1}+\gamma_{22}\Delta\text{gs10}_{t-2}+\gamma_{23}\Delta\text{gs10}_{t-3}\\

&+\alpha_2(\text{tb3ms}_{t-1}-\theta\text{gs10}_{t-1}-\mu)+u_{2t}.

\end{align}

\]

We can use the VECM function from the vars package to estimate the VECM model for tb3ms and gs10 as shown below. The lag argument specifies the number of lags in the VECM, the r argument specifies the number of cointegrating relationships, and the include argument specifies whether to include an intercept or a linear time trend in the VECM. The beta argument allows us to specify the cointegrating vector. Since we have already estimated the cointegrating parameter \(\theta\) in the two-step approach, we can use this estimate to specify the cointegrating vector as \(\bs{\beta} = (1, -\hat{\theta})^{'}\). The estim argument specifies the estimation method, and the LRinclude argument specifies whether to include an intercept or a linear time trend in the error correction term.

summary(model)#############

###Model VECM

#############

Full sample size: 236 End sample size: 232

Number of variables: 2 Number of estimated slope parameters 14

AIC -682.5401 BIC -630.839 SSR 139.7794

Cointegrating vector (estimated by ML):

tb3ms gs10 const

r1 1 -1.007232 1.576377

ECT tb3ms -1 gs10 -1

Equation tb3ms -0.0945(0.0423)* 0.3727(0.0838)*** 0.0564(0.1207)

Equation gs10 0.0688(0.0289)* 0.0397(0.0574) 0.2099(0.0826)*

tb3ms -2 gs10 -2 tb3ms -3

Equation tb3ms -0.1999(0.0825)* -0.1886(0.1224) 0.2788(0.0827)***

Equation gs10 -0.0801(0.0565) -0.0895(0.0837) 0.0732(0.0566)

gs10 -3

Equation tb3ms 0.1048(0.1206)

Equation gs10 0.0566(0.0825) The first block of the estimation output presents the estimated cointegrating vector: \(\boldsymbol{\beta} = (\beta_1, \beta_2)^{'} = (1, -\theta)^{'}\). The estimated cointegrating parameter is \(\hat{\theta} = -\hat{\beta}_2 = 1.007\), which is close to the value obtained from the two-step approach.

The estimated coefficients for the lag terms appear in the second block of the estimation output. For \(\Delta\text{tb3ms}\), only its own lag terms are statistically significant at the 5% level. For \(\Delta\text{gs10}\), only the first lag of its own term is statistically significant at the 5% level.

The estimated coefficients for the error correction terms are provided under the ECT column. These coefficients are \(\hat{\alpha}_1 = -0.0945\) and \(\hat{\alpha}_2 = 0.0688\), both of which are statistically significant at the 5% level. The estimate \(\hat{\alpha}_1 = -0.0945\) suggests that the error correction term \((\text{tb3ms}_{t-1} - \theta\times \text{gs10}_{t-1} - \mu)\) negatively affects \(\Delta\text{tb3ms}_t\), while \(\hat{\alpha}_2 = 0.0688\) indicates a positive effect on \(\Delta\text{gs10}_t\). These estimates imply that if the short-term interest rate exceeds the long-term interest rate by more than 1.6, the short-term interest rate will decrease while the long-term interest rate will increase, and vice versa.

We can use the ca.jo function from the urca package to perform the Johansen cointegration test. The ca.jo function requires the data to be in a ts object. The type argument specifies the type of test to be performed: trace for the trace statistic and eigen for the maximum eigenvalue statistic. The K argument specifies the number of lags in the VAR model, and the ecdet argument specifies the deterministic component to be included in the vector error correction term.

# Trace statistic and critical values

summary(trace_stat)

######################

# Johansen-Procedure #

######################

Test type: trace statistic , without linear trend and constant in cointegration

Eigenvalues (lambda):

[1] 9.424203e-02 9.556330e-03 8.765943e-18

Values of teststatistic and critical values of test:

test 10pct 5pct 1pct

r <= 1 | 2.24 7.52 9.24 12.97

r = 0 | 25.30 17.85 19.96 24.60

Eigenvectors, normalised to first column:

(These are the cointegration relations)

tb3ms.l1 gs10.l1 constant

tb3ms.l1 1.000000 1.000000 1.000000

gs10.l1 -1.042671 8.075155 -3.891947

constant 1.769976 -50.520741 68.811930

Weights W:

(This is the loading matrix)

tb3ms.l1 gs10.l1 constant

tb3ms.d -0.02828046 -0.002548758 -1.766993e-18

gs10.d 0.08968674 -0.001255779 -2.534307e-19The trace statistics for \(H_0:\text{rank}(\bs{\Pi})=0\) and \(H_0:\text{rank}(\bs{\Pi})=1\) are 25.30 and 2.24, respectively. The corresponding critical values at the 5% significance level are 19.96 and 9.24. Thus, we can reject \(H_0:\text{rank}(\bs{\Pi})=0\) but fail to reject \(H_0:\text{rank}(\bs{\Pi})=1\). As a result, we conclude that there is one cointegrating relationship according to the trace statistic.

The maximum eigenvalue statistics for \(H_0:\text{rank}(\bs{\Pi})=0\) and \(H_0:\text{rank}(\bs{\Pi})=1\) are 23.06 and 2.24, respectively. The corresponding critical values at the 5% significance level are 15.67 and 9.24. Again, we can reject \(H_0:\text{rank}(\bs{\Pi})=0\) but fail to reject \(H_0:\text{rank}(\bs{\Pi})=1\). As a result, the maximum eigenvalue statistic also suggests one cointegrating relationship.

# Maximum eigenvalue statistic and critical values

summary(trace_eigen)

######################

# Johansen-Procedure #

######################

Test type: maximal eigenvalue statistic (lambda max) , without linear trend and constant in cointegration

Eigenvalues (lambda):

[1] 9.424203e-02 9.556330e-03 8.765943e-18

Values of teststatistic and critical values of test:

test 10pct 5pct 1pct

r <= 1 | 2.24 7.52 9.24 12.97

r = 0 | 23.06 13.75 15.67 20.20

Eigenvectors, normalised to first column:

(These are the cointegration relations)

tb3ms.l1 gs10.l1 constant

tb3ms.l1 1.000000 1.000000 1.000000

gs10.l1 -1.042671 8.075155 -3.891947

constant 1.769976 -50.520741 68.811930

Weights W:

(This is the loading matrix)

tb3ms.l1 gs10.l1 constant

tb3ms.d -0.02828046 -0.002548758 -1.766993e-18

gs10.d 0.08968674 -0.001255779 -2.534307e-1926.6 Volatility clustering and autoregressive conditional heteroskedasticity

The conditional variance of financial asset returns is called volatility. The volatility increases during financial crises and decreases during periods of economic stability.

Definition 26.7 (Volatility clustering) A series exhibits volatility clustering if periods of high volatility are followed by high volatility, and periods of low volatility are followed by low volatility.

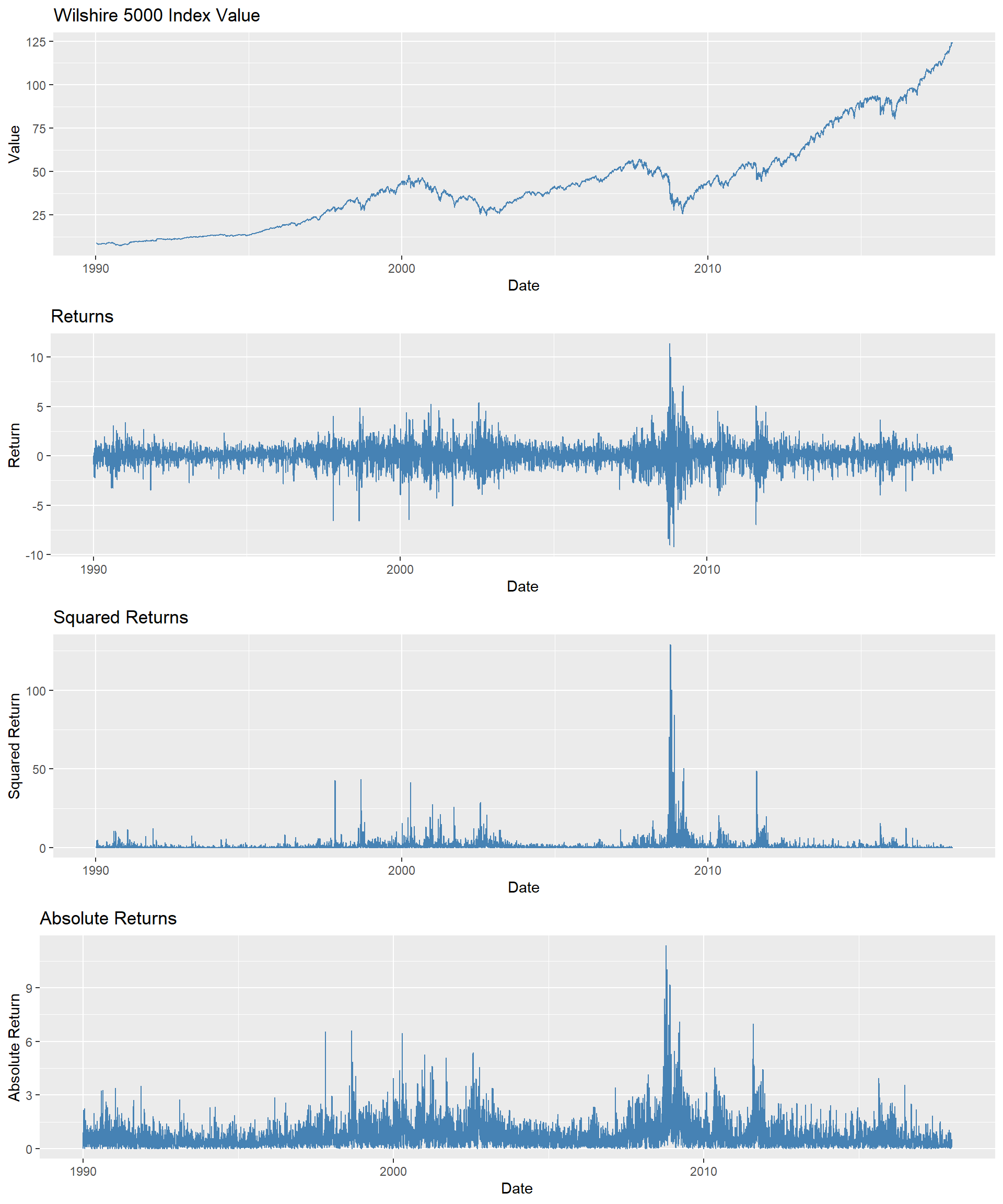

As an example, we consider the daily Wilshire 5000 index, a broad stock market index that includes all actively traded U.S. stocks. Figure 26.7 displays the time series plots of the index value, returns, squared returns, and absolute returns. The returns are calculated as the percentage change in the index value; squared returns are the square of the returns, and absolute returns are the absolute value of the returns. Although the index value shows an upward trend, there are periods where the value decreases. The returns exhibit volatility clustering, with periods of high volatility followed by high volatility and periods of low volatility followed by low volatility. This pattern is also observed in the squared and absolute returns.

# Load the data

df <- read.csv("data/WILL500IND.csv")

# Convert the date column to Date format

df$date <- as.Date(df$date)

# Compute returns

df$return <- 100 * (df$value - dplyr::lag(df$value)) / dplyr::lag(df$value)

# Compute squared returns

df$squared_return <- df$return^2

# Compute absolute returns

df$abs_return <- abs(df$return)

# Set the date as the index (convert to a time-series object if desired)

df <- df[order(df$date), ]

rownames(df) <- df$date# Plot 1: Index value

p1 <- ggplot(df, aes(x = date, y = value)) +

geom_line(color = "steelblue") +

labs(

title = "Wilshire 5000 Index Value",

x = "Date",

y = "Value"

)

# Plot 2: Returns

p2 <- ggplot(df, aes(x = date, y = return)) +

geom_line(color = "steelblue") +

labs(

title = "Returns",

x = "Date",

y = "Return"

)

# Plot 3: Squared returns

p3 <- ggplot(df, aes(x = date, y = squared_return)) +

geom_line(color = "steelblue") +

labs(

title = "Squared Returns",

x = "Date",

y = "Squared Return"

)

# Plot 4: Absolute returns

p4 <- ggplot(df, aes(x = date, y = abs_return)) +

geom_line(color = "steelblue") +

labs(

title = "Absolute Returns",

x = "Date",

y = "Absolute Return"

)

# Arrange plots in a single column

grid.arrange(p1, p2, p3, p4, ncol = 1)

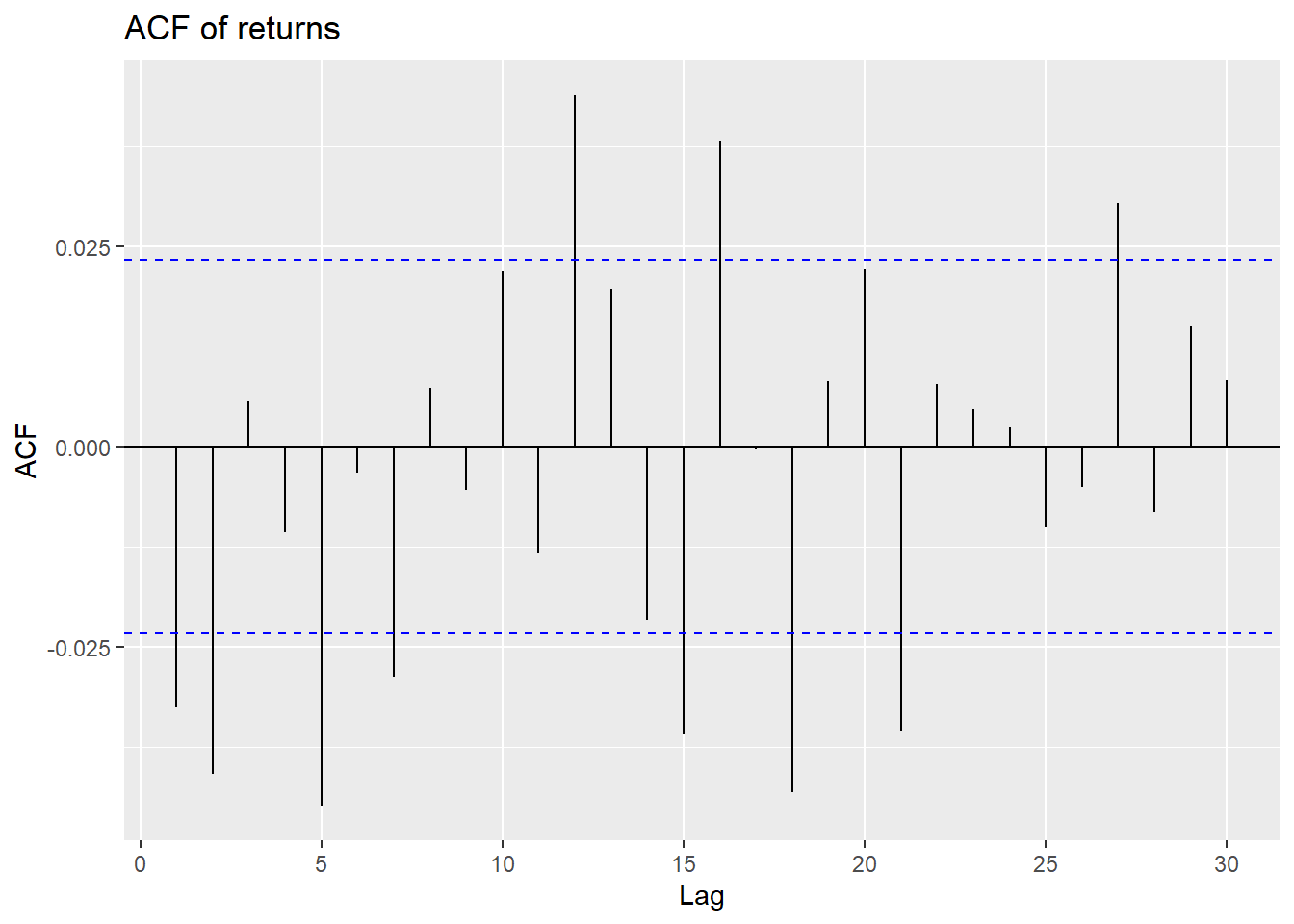

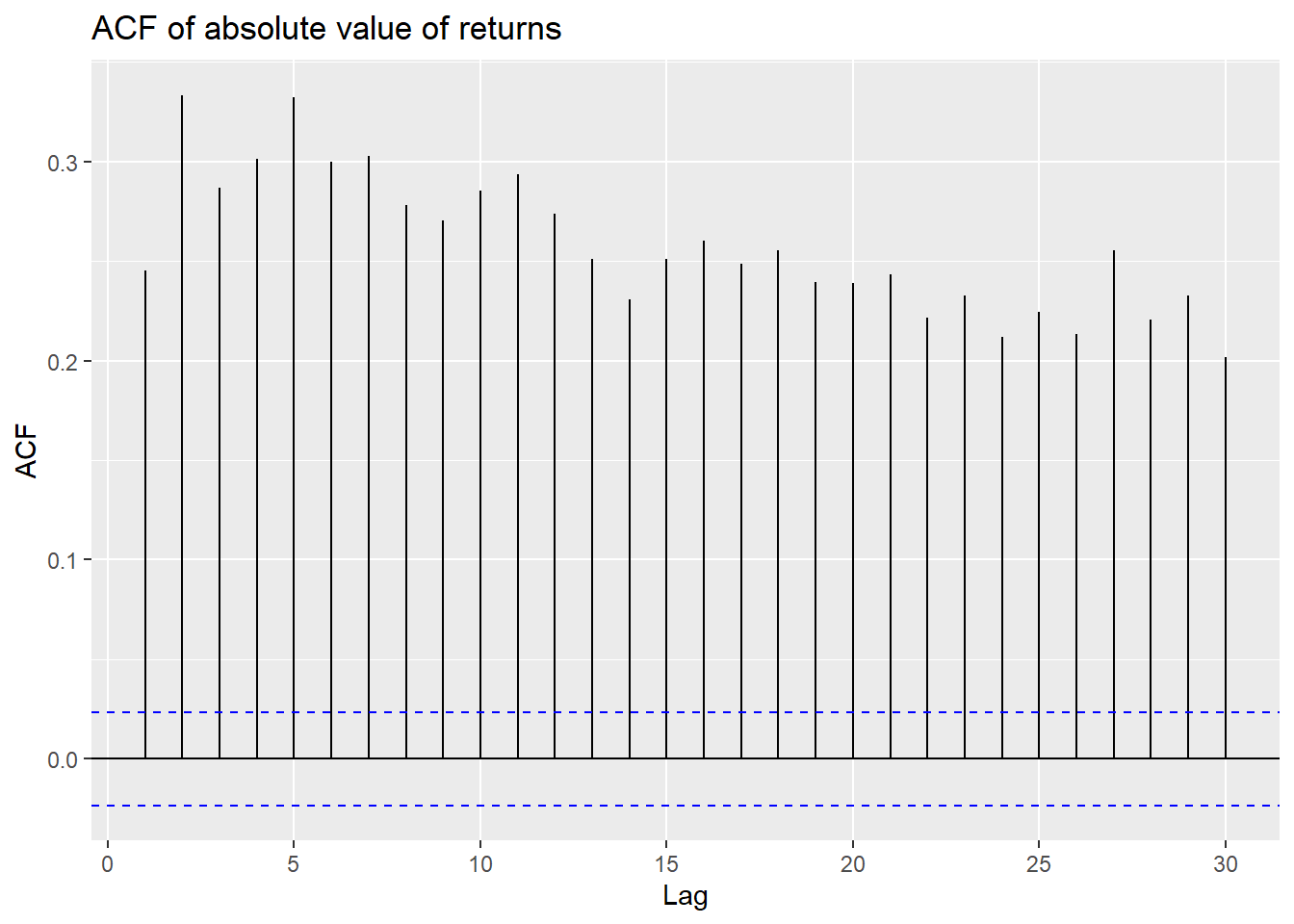

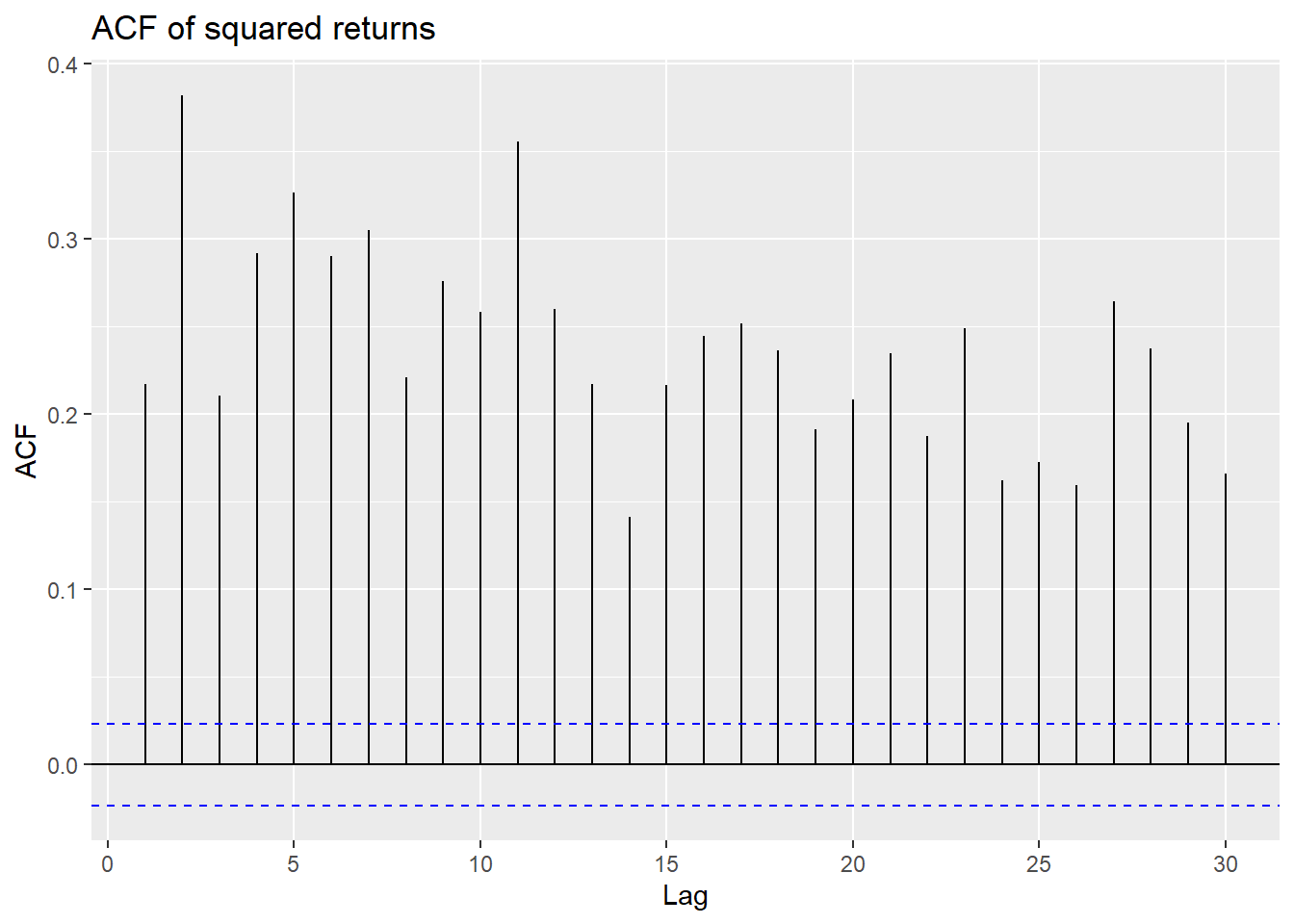

The volatility clustering observed in the returns leads to autocorrelation in the squared returns. The correlograms of the returns and squared returns are shown in Figure 26.8. While the autocorrelation of the returns is relatively small at all lags, the autocorrelation of the squared returns is significant at all lags and decays slowly.

# Autocorrelation of returns, absolute value of returns, and squared returns

ggAcf(df$return[-1], lag.max = 30) +

labs(title = "ACF of returns")

ggAcf(df$abs_return[-1], lag.max = 30) +

labs(title = "ACF of absolute value of returns")

ggAcf(df$squared_return[-1], lag.max = 30) +

labs(title = "ACF of squared returns")

In Figure 26.8, we observe that autocorrelations of returns are rather weak, making it difficult to predict future outcomes using, for example, an AR model. However, we observe strong and persistent autocorrelation in the absolute value of returns and the squared returns.

In this section, we review two methods for estimating volatility: (i) the realized volatility approach and (ii) the model-based approach. Estimating volatility is important for several reasons. First, the volatility of an asset serves as a measure of its risk. A risk-averse investor will require a higher return for holding an asset with higher volatility. Second, volatility is used in the pricing of financial derivatives. For example, the Black-Scholes option pricing model uses the volatility of the underlying asset as an input. Third, volatility can be used to improve the accuracy of forecast intervals.

26.6.1 The realized volatility approach

The realized volatility approach uses high-frequency data to estimate the volatility of an asset. Since the mean return of the high-frequency data is close to zero, volatility is typically estimated not by the sample variance, but by the sample root mean square of the returns. The \(h\)-period realized volatility estimate of a variable \(Y_t\) is the sample root mean square of \(Y\) computed over \(h\) consecutive periods: \[ \begin{align} \text{RV}^h_t=\sqrt{\frac{1}{h}\sum_{s=t-h+1}^tY^2_s}. \end{align} \]

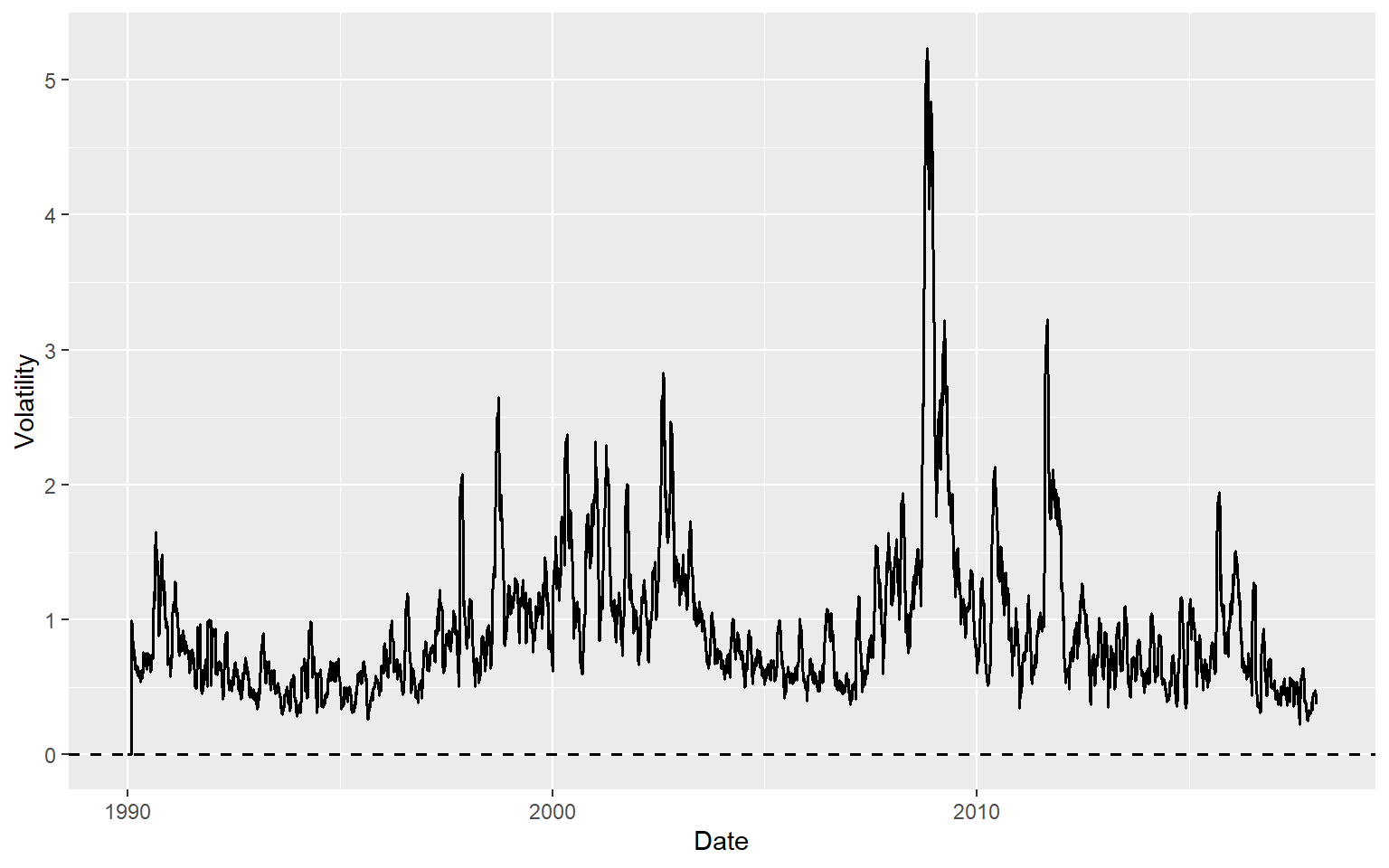

For the Wilshire 5000 index returns, we set \(h=20\) and compute the 20-day realized volatility. In the following, we compute the realized volatility using the return column in the df DataFrame.

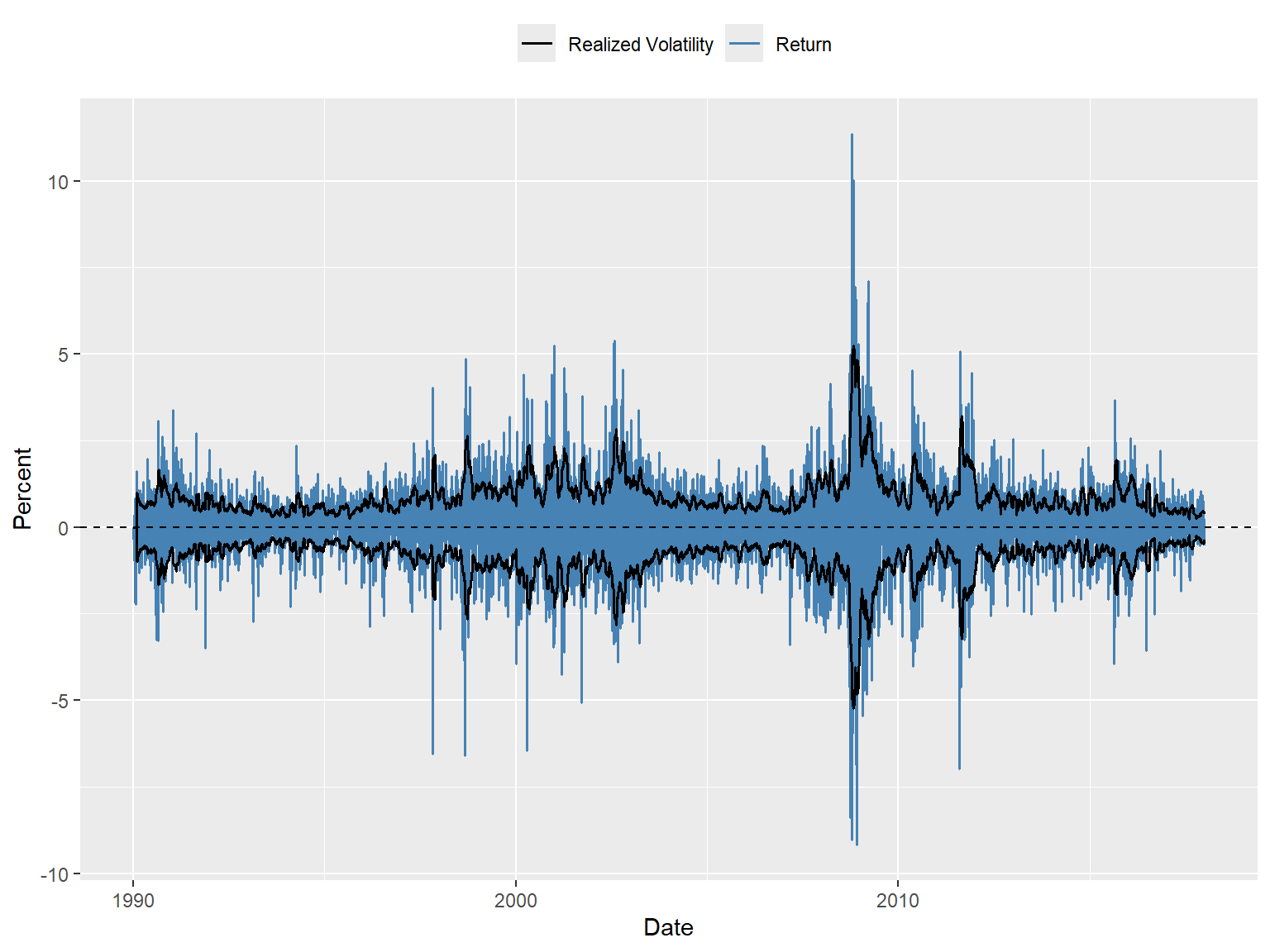

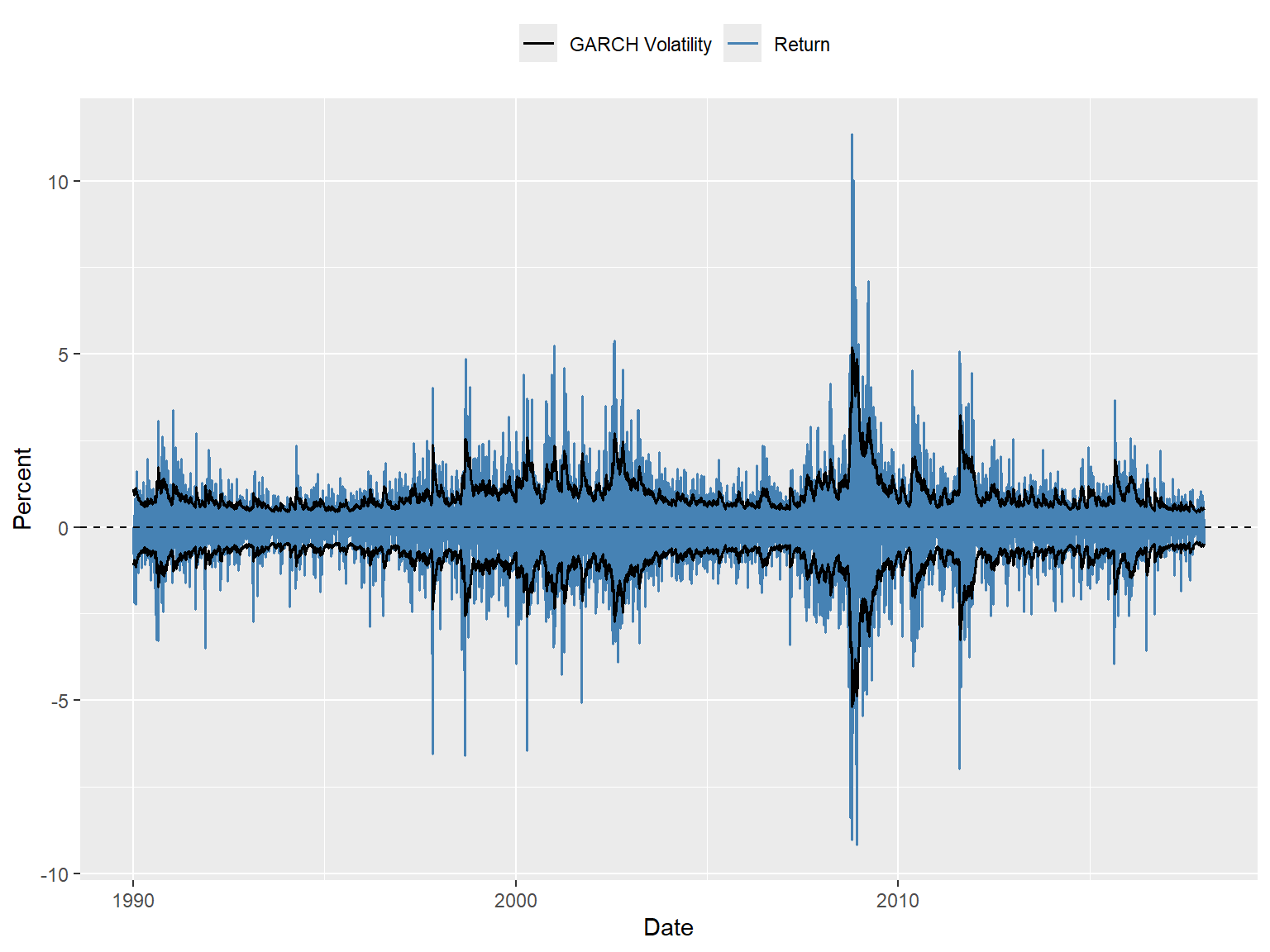

The time-series plot of the 20-day realized volatility estimates is shown in Figure 26.9. In Figure 26.10, we plot the returns along with the realized volatility bands (\(\pm\text{RV}\)). The figure shows that when returns are large, realized volatility is also high, and vice versa, suggesting that realized volatility effectively captures the volatility clustering observed in the returns. The width of the band can be used to identify periods of high volatility. For example, the realized volatility bands are wide during the 2008 financial crisis, indicating high volatility in the returns.

# Time-series plot of the 20-day realized volatility estimates

ggplot(df, aes(x = date, y = RV)) +

geom_line(color = "black", linewidth = 0.7) +

geom_hline(yintercept = 0, linetype = "dashed", color = "black", linewidth = 0.6) +

labs(

x = "Date",

y = "Volatility"

)

# Time-series plot of returns along with the realized volatility bands

ggplot(df, aes(x = date)) +

geom_line(aes(y = return, color = "Return"), linewidth = 0.6) +

geom_line(aes(y = RV, color = "Realized Volatility"), linewidth = 0.7) +

geom_line(aes(y = -RV), color = "black", linewidth = 0.7) +

geom_hline(yintercept = 0, linetype = "dashed", color = "black") +

labs(

x = "Date",

y = "Percent",

color = ""

) +

scale_color_manual(values = c(

"Return" = "steelblue",

"Realized Volatility" = "black"

)) +

theme(legend.position = "top")

26.6.2 The model-based approach

The model-based approach is used when the data are not available at high frequency. The most popular model for estimating volatility is the autoregressive conditional heteroskedasticity (ARCH) model proposed by Engle (1982) and its extension, the generalized autoregressive conditional heteroskedasticity (GARCH) model proposed by Bollerslev (1986). In the ARCH model, we assume that the conditional variance of the returns is a function of the past squared returns. The ARCH(\(p\)) model is given by \[ \begin{align} &Y_t=\beta_0+\beta_1Y_{t-1}+\gamma_1X_{t-1}+u_t,\\ &\sigma^2_t=\omega+\alpha_1u^2_{t-1}+\alpha_2u^2_{t-2}+\ldots+\alpha_pu^2_{t-p}, \end{align} \tag{26.21}\] where \(Y_t\) is the return, \(X_t\) is a regressor, \(u_t\) is the error term, which is independent over \(t\) with mean zero and variance \(\sigma^2_t\). The parameters \(\beta_0,\beta_1,\gamma_1,\omega, \alpha_1,\ldots,\alpha_p\) are unknown coefficients. The first equation is the mean equation, where we assume an ADL(1,1) model for the returns. The second equation is the variance equation, where the conditional variance \(\sigma^2_t\) is a function of the past squared error terms.

The GARCH(p,q) model extends the ARCH model by including past conditional variances in the variance equation: \[ \begin{align} \sigma^2_t=\omega+\sum_{i=1}^p\alpha_iu^2_{t-i}+\sum_{j=1}^q\beta_j\sigma^2_{t-j}, \end{align} \tag{26.22}\] where \(\omega,\alpha_1,\ldots,\alpha_p,\beta_1,\ldots,\beta_q\) are unknown parameters.

For both models, the mean equation can alternatively be specified as \[ \begin{align} &Y_t=\beta_0+\beta_1Y_{t-1}+\gamma_1X_{t-1}+\sigma_tv_t, \end{align} \tag{26.23}\] where \(v_t\) is i.i.d over \(t\) with mean zero and variance one. The error term \(u_t\) in Equation 26.21 is then given by \(u_t=\sigma_tv_t\).

Consider the GARCH(1,1) model and let \(\mathcal{F}_{t-1}\) be the information set available at time \(t-1\). Then, the conditional mean and variance of \(Y_t\) are \[ \begin{align} \E(Y_t|\mathcal{F}_{t-1})&=\E(\beta_0+\beta_1Y_{t-1}+\gamma_1X_{t-1}+\sigma_tv_t|\mathcal{F}_{t-1})\\ &=\beta_0+\beta_1Y_{t-1}+\gamma_1X_{t-1}+\sigma_t\E\left(v_t|\mathcal{F}_{t-1}\right)\\ &=\beta_0+\beta_1Y_{t-1}+\gamma_1X_{t-1}, \end{align} \tag{26.24}\] and \[ \begin{align} \text{Var}(Y_t|\mathcal{F}_{t-1})&=\E((Y_t-(\beta_0+\beta_1Y_{t-1}+\gamma_1X_{t-1}))^2|\mathcal{F}_{t-1})\\ &=\E(\sigma^2_tv^2_t|\mathcal{F}_{t-1})\\ &=\sigma^2_t\E\left(v^2_t|\mathcal{F}_{t-1}\right)\\ &=\sigma^2_t. \end{align} \tag{26.25}\]

Thus, the conditional standard deviation is \(\sqrt{\text{Var}(Y_t|\mathcal{F}_{t-1})}=\sigma_t\).

Definition 26.8 (Volatility) In ARCH and GARCH models, the conditional standard deviation \(\sigma_t\) is called volatility.

26.6.3 Estimation of ARCH and GARCH models

The ARCH and GARCH models can be estimated using the maximum likelihood method. Under the assumption that \(v_t\sim N(0,1)\), we have \(Y_t|\mathcal{F}_{t-1}\sim N(\beta_0+\beta_1Y_{t-1}+\gamma_1X_{t-1},\sigma^2_t)\). Thus, we can express the likelihood function of GARCH\((\)p,q\()\) as \[ \begin{align} L(\theta)=\prod_{t=1}^T\frac{1}{\sqrt{2\pi\sigma^2_t}}\exp\left(-\frac{1}{2\sigma^2_t}(Y_t-\beta_0-\beta_1Y_{t-1}-\gamma_1X_{t-1})^2\right), \end{align} \tag{26.26}\] where \(\theta=(\beta_0,\beta_1,\gamma_1,\omega,\alpha_1,\ldots,\alpha_p,\phi_1,\ldots,\phi_q)^{'}\) is the vector of unknown parameters. The log-likelihood function is then given by \[ \begin{align} \ln L(\theta)=-\frac{T}{2}\ln(2\pi)-\frac{1}{2}\sum_{t=1}^T\ln(\sigma^2_t)-\frac{1}{2}\sum_{t=1}^T\frac{1}{\sigma^2_t}(Y_t-\beta_0-\beta_1Y_{t-1}-\gamma_1X_{t-1})^2. \end{align} \tag{26.27}\]

Then, the maximum likelihood estimator (MLE) is defined by \[ \begin{align} \hat{\theta}=\text{argmax}_{\theta} L(\theta). \end{align} \tag{26.28}\]

Under some standard assumptions, the MLE is a consistent estimator and has an asymptotic normal distribution. For further details on the estimation of ARCH and GARCH models, see Hamilton (1994) and Francq and Zakoian (2019).

26.6.4 Volatility forecasting

We assume the following GARCH(1,1) model for the returns: \[ \begin{align} &Y_t=\beta_0+\sigma_tv_t,\\ &\sigma^2_t=\omega+\alpha_1u^2_{t-1}+\phi_1\sigma^2_{t-1}, \end{align} \] for \(t=1,\ldots,T\). Then, from \(Y_{T+1}=\beta_0+u_{T+1}\), we obtain one-step ahead forecast as \[ \begin{align} Y_{T+1|T}=\E(Y_{T+1}|\mathcal{F}_T)=\E(\beta_0+u_{T+1}|\mathcal{F}_T)=\beta_0. \end{align} \] In general, the \(h\)-step forecast is \(Y_{T+h|T}=\beta_0\). Let \(e_h\) be the \(h\)-step ahead forecast error. Then, we have \[ \begin{align} e_h=Y_{T+h}-Y_{T+h|T}=\beta_0+u_{T+h}-\beta_0=u_{T+h}. \end{align} \] The conditional variance of \(e_h\) is \[ \begin{align} \var(e_h|\mathcal{F}_T)&=\var(u_{T+h}|\mathcal{F}_T)=\E(u^2_{T+h}|\mathcal{F}_T)\\ &=\E(\sigma^2_{T+h}v^2_{T+h}|\mathcal{F}_T)=\E(\sigma^2_{T+h}|\mathcal{F}_T). \end{align} \]